An 80% Discount to NAV, Four Weeks to Close

Stray Narratives, Issue 11 - A $398m market cap. $986m of Shanghai-listed Insta360 stock, $230m of net cash, plus an operating business that already clears the market cap on its own.

Stray Narratives is published when the market demands a closer look. Nothing in this publication constitutes investment advice. All views are those of the author. Please read our full disclaimer.

If you have no time to read and prefer to sit back, relax, and listen to this article in a podcast format by Notebook LLM (only 5 minutes long!):

The trade

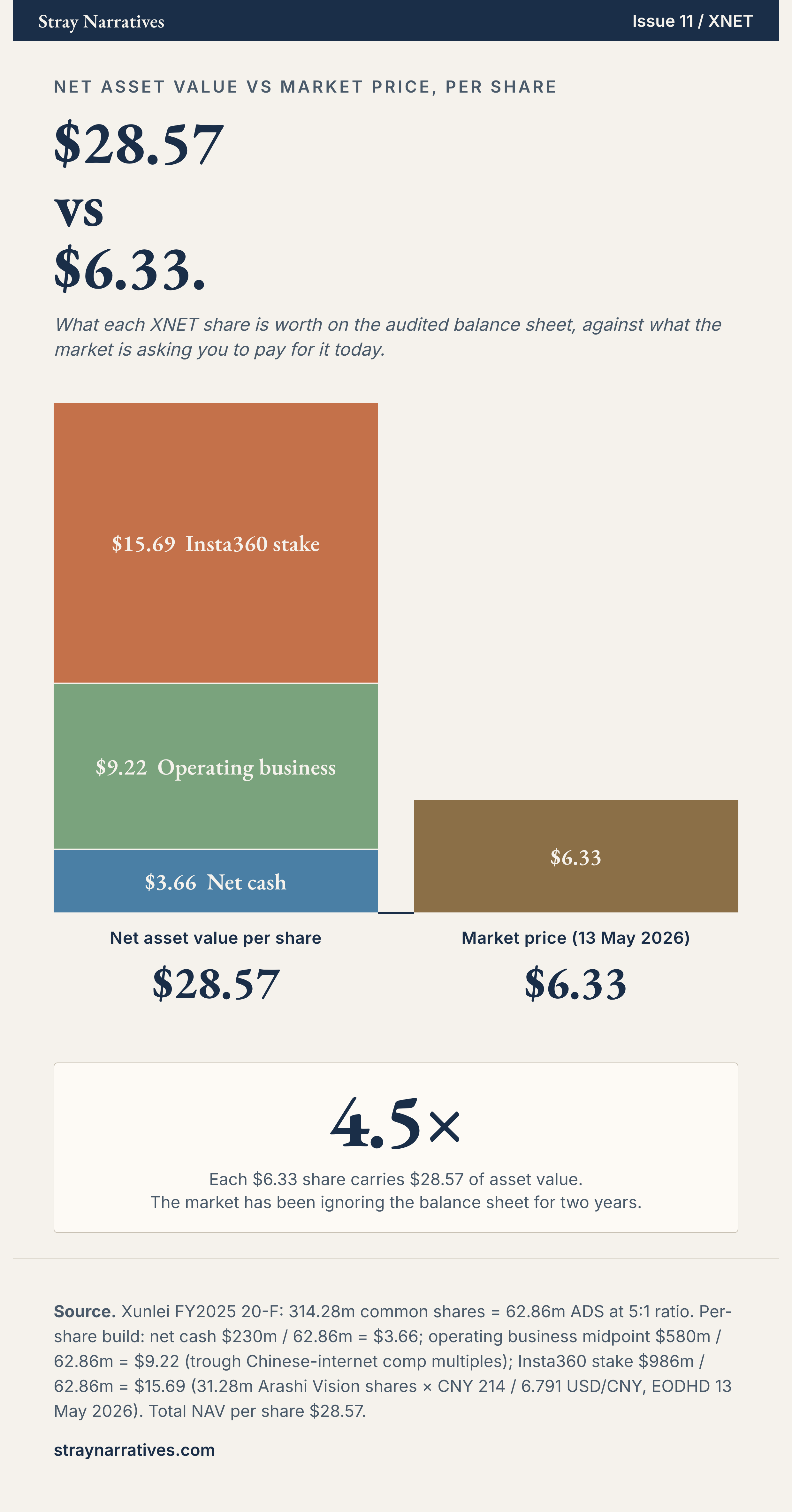

Buy Xunlei (NASDAQ: XNET) for 6 US dollars before the 11 June 2026 lock-up unlocks on its Insta360 stake [1]. You are paying $398m for a Chinese internet operator whose Shanghai-listed equity stake is worth $986m at the 13 May close [2], whose net cash is $230m after netting bank debt [1], and whose operating business is worth another $410m–$745m on current Chinese-internet trough multiples.

That is a 78% discount to net asset value with a hard catalyst date and a published lock-up schedule.

Twenty-two years in the attic

Xunlei was a download manager in 2003, the first to make peer-to-peer file transfer fast enough to matter in China. It IPO’d on Nasdaq in 2014, lost the founder in 2017, pivoted into cloud, then live streaming, then short-form video, then accelerator subscriptions. Each pivot left a residual asset on the balance sheet.

One residual was a strategic equity position in Insta360, taken in the early 2010s when Xunlei was still a venture-portfolio business. It compounded silently while management chased four other things. Insta360 IPO’d on Shanghai’s STAR Market on 11 June 2025. Xunlei held 8.73% pre-offering, 7.84% after dilution, and approximately 7.8% at year-end 2025 per the audited filing [1].

This is what fifteen years of Chinese-internet pivoting looks like. It looks like an attic full of strategic equity stakes nobody is paying attention to. Most of them are worth nothing. One, by accident, is worth more than two and a half times the entire company holding it.

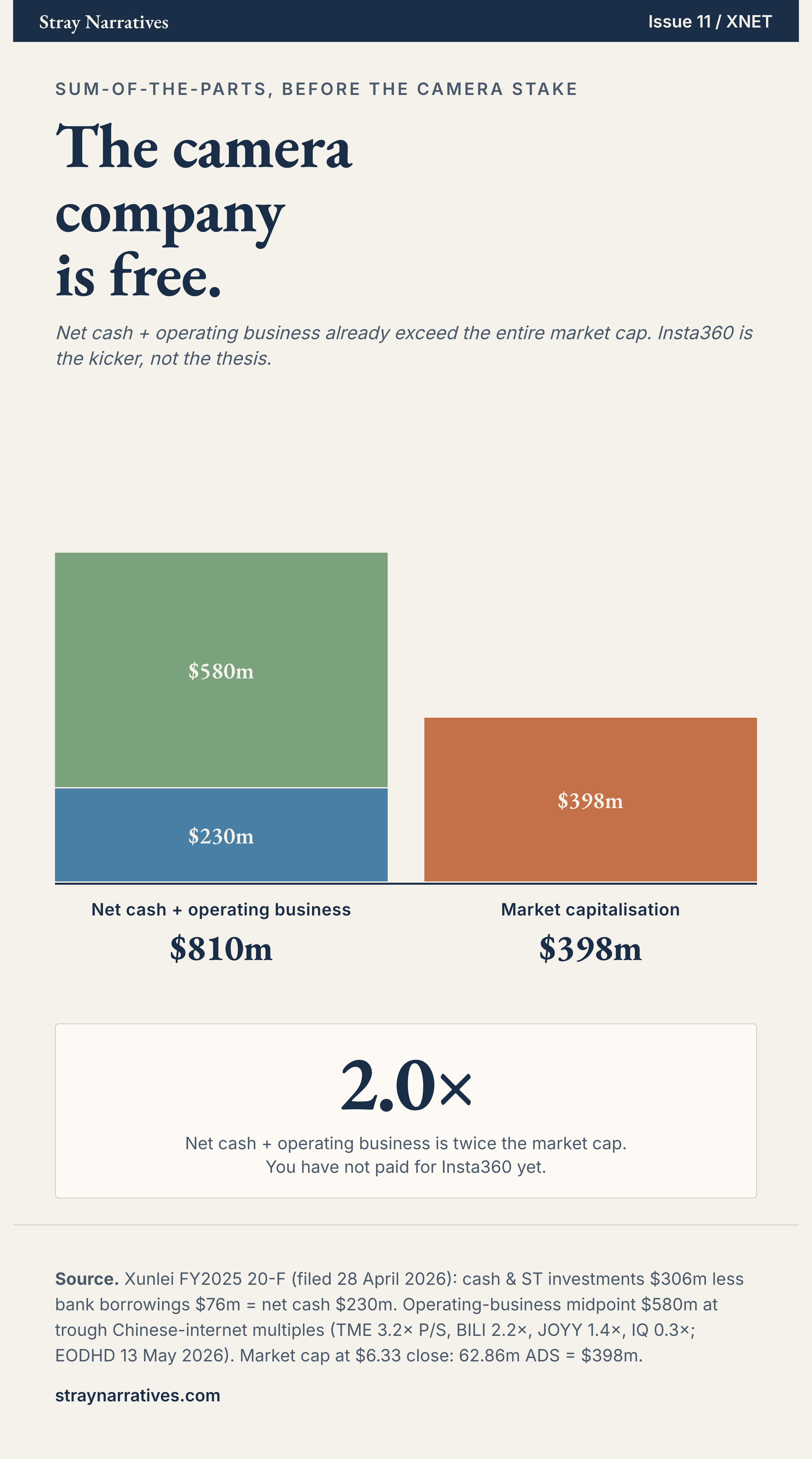

What you are buying, before the camera stake

Skip the camera stake for a moment. Pretend it does not exist.

For $398m you get a Chinese internet operator with $462m of revenue growing 42.5% in 2025 [1], $230m of net cash on the balance sheet, and a real operating business in three pieces.

Subscriptions. Xunlei Accelerator. $155m revenue, +16% growth, mid-twenties operating margins. Closest comps in the current trough are Tencent Music at 3.2× P/S, Bilibili at 2.2× P/S, iQIYI at 0.3× P/S [3]. At 1.5–2.5× revenue today, the subscription cash cow is worth $230m–$390m. Through-cycle (when the comps re-rate to 2020–2022 levels) the same business is worth $385m–$545m. Either way, it alone clears more than half the market cap.

Live streaming and IVAS. $170m revenue, +97.5% growth, including the inorganic Hupu contribution from Q2 2025. Hupu is the leading Chinese sports media platform, acquired May 2025 for RMB 500m, which sets a $69m floor under that piece. Closest comp: JOYY at 1.4× P/S [3]. At 1.0–2.0× revenue today this segment is worth $170m–$340m. Through-cycle, $425m–$680m.

Cloud. Twenty per cent residual in Onething, after Xunlei sold the controlling 50% to Kingsoft Cloud for RMB 125m in March 2026 [1]. Pro-rata value: $10m–$15m. The cleanest piece of capital allocation management has done in years was deciding they were not the right operator. They walked.

Operating business at current trough multiples: $410m–$745m, midpoint $580m. Through-cycle: $820m–$1,240m. We anchor the headline visual to the trough-midpoint because we want a number a sceptical reader cannot dismantle on a Bloomberg comp screen. The honest disclosure is that the trade improves substantially if Chinese-internet multiples re-rate.

The operating business and net cash exceed the market cap before Insta360 contributes a dollar. Even at the trough-low end ($410m of ops biz), net cash plus operating business clears $640m, against a $398m market cap. The camera company is technically free. It is also actually worth most of the value.

The Insta360 stake, the kicker

Insta360 holds 67% of consumer 360-degree cameras and is now joint leader in action cameras alongside DJI [4]. GoPro, the once-dominant incumbent, is the third name and falling. Q2 2025 revenue grew 41% to $190m. Trailing-twelve-month growth: 77%. The stock closed at 214 yuan on 13 May 2026, down 43% from its September peak of 378 yuan, well above the IPO offer price of 47 [5]. The chart is messy but the business is fine. Check out this video if, like me, you are too old to know what Insta360 is.

Xunlei’s stake: approximately 7.8% per the FY2025 20-F, equivalent to 31.28m Arashi Vision shares [1][2]. Audited carrying value at 31 December 2025: $1,051m. Mark at 13 May 2026: $986m.

The lock-up bucket is the standard 12 months under STAR Market rules. The 36-month rule applies only to controlling shareholders (Shenzhen Yiwei at 29.94%); the 24-month rule applies only to the underwriter’s investment arm. Xunlei sits in the 12-month bucket per the prospectus shareholder-commitment table [6]. The lock-up unlocks on 11 June 2026, less than a month away.

After the lock-up, Xunlei can sell. PRC corporate income tax (25%) plus Cayman repatriation withholding (10%) plus capital-control timing means roughly fifty cents of every gross dollar reaches ADR holders in the central case [7]. Insta360 is the kicker on a position the operating business already underwrites. You get the cake and the icing.

The risks honestly

Five concerns. They are also, mostly, the discount decomposition.

The lock-up could be voluntarily extended. It is not, per primary text. Xunlei is in the standard 12-month bucket. Management’s Q3 2025 commentary, “no plans to sell Arashi Vision shares due to regulatory requirements,” is consistent with the active 12-month restriction. Q4 commentary shifted to “determine the pace based on capital market conditions,”which is the right vocabulary for a board preparing to sell.

Insta360’s share price could correct further. It could. The doomsday case stress-tests against an IPO-band retracement to 70 yuan. There the trade loses money. I am not pretending otherwise.

Management never returns the cash. This is the structural risk. Twenty-two years without a dividend. Cumulative buyback through end-2025: $6.5m on a $20m authorisation [8]. At that pace, the authorisation will be exhausted some time in 2031. The market is pricing this management like the founder is still in the chair. He has not been since 2017. Current CEO Jinbo Li, in role since April 2020, launched the first two buyback programmes in company history (2023 and 2024). The pace is glacial. The direction is right. The Sohu/Changyou going-private at an 82% premium in April 2020 [9] is the comparable success precedent for a Chinese-ADR-holdco-to-portfolio monetisation. It is one data point, not a frequency.

Capital controls bite. They do. I model them in each scenario. The bear case (20% reach-through) is already heavy.

HFCAA delisting. Currently dormant. The PCAOB removed mainland China and Hong Kong from its inspection blacklist in December 2022 [10]; Xunlei does not expect to be identified as a Commission-Identified Issuer. The base case does not require this to remain dormant. Reactivation is the high-asymmetry tail.

The discount sits at 78% of net asset value because three reasons unwind mechanically (lock-up inertia, dormant HFCAA cohort drag, small-cap liquidity friction) and two are structurally priced (capital controls, management-distribution discipline). The market may be right that current management will inherit founder-era inertia. It may also be looking at the wrong twenty-two years.

How to express the trade

Stock: Linear, lower-leverage, suitable for a multi-month hold through the monetization window.

Call options: Higher leverage, time-bounded, binary downside. June, July, October, and January 2027 expiries each capture a different stretch of the catalyst window. Out-of-the-money calls magnify the stock returns 3–5×, with proportional risk of going to zero. Calls magnify everything, including being wrong. Reader picks the variance.

Expected return

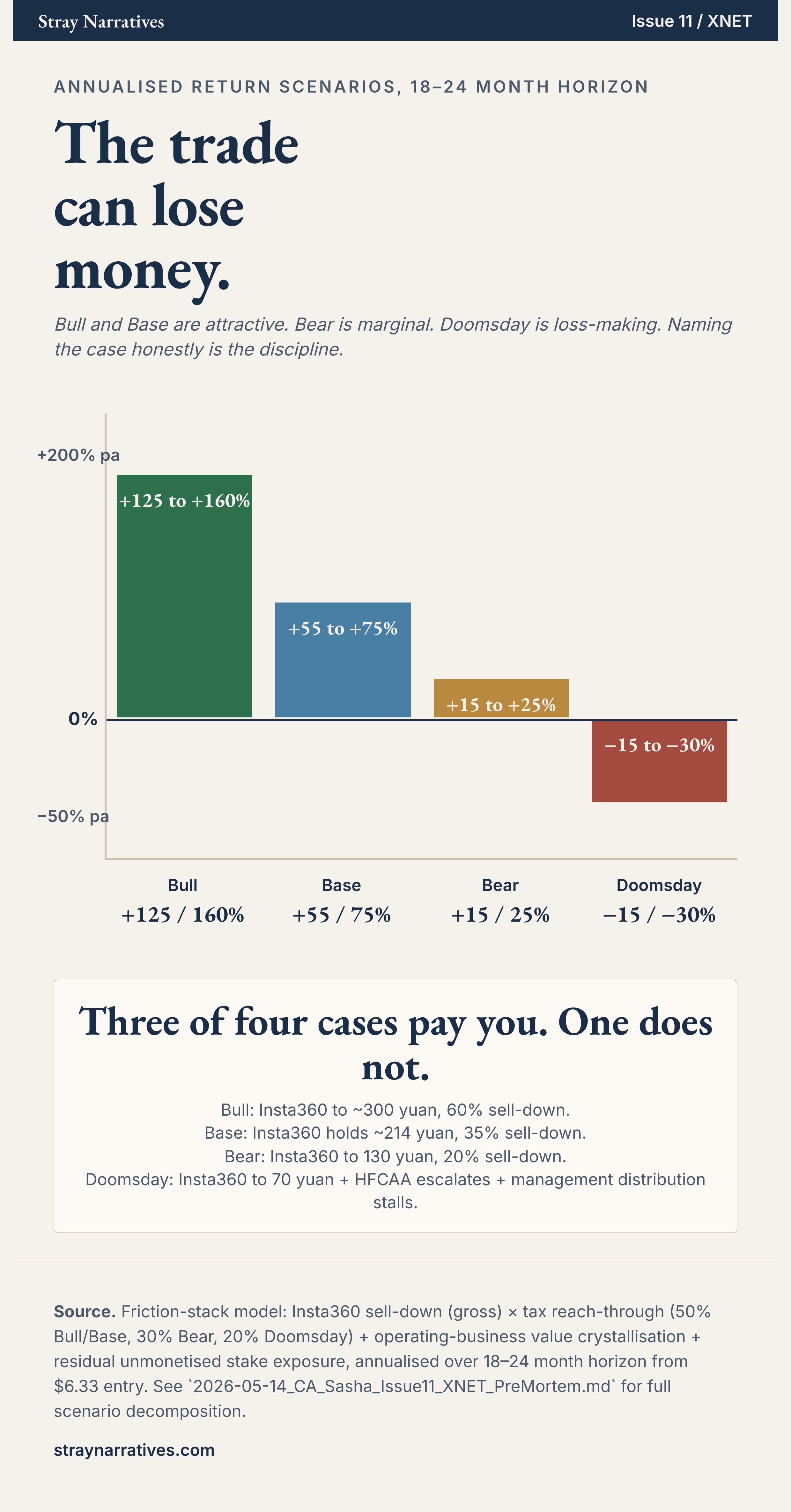

Today’s $6.33 close is the entry. Hold through the 18–24 month monetisation window after 11 June 2026.

The visual headline of 4.5× is the gap between current price and net asset value. The realised return is the gap times the friction stack: tax leakage (25% PRC CIT + 10% Cayman withholding ≈ 50% reach-through), partial monetisation (30–40% of the stake sold over 18 months in our central case), and the residual unmonetised stake remaining exposed to whatever Insta360 trades at after the window closes. The visual depicts NAV. The IRR depicts what survives the friction stack.

Bull (Insta360 to ~300 yuan, 60% of stake monetised in 18 months, 50% reach-through, ops biz re-rates toward through-cycle): 125–160% per annum. Calls magnify 3–5×.

Base (Insta360 holds ~214 yuan, 35% monetised over 18 months, 50% reach-through, ops biz partially re-rates): 55–75% per annum.

Bear (Insta360 to 130 yuan, 20% monetised, 30% reach-through, no ops re-rating): even the bear case has a positive 15–25% per annum.

Doomsday (Insta360 to 70 yuan plus HFCAA escalates plus management distribution stalls plus operating margin compression): −15% to −30% per annum. This trade can lose money.

The path is staged: the first four weeks carry a discount-narrowing flow as the market reads the catalyst date; the next twelve carry the actual monetization; the eighteen to twenty-four months carry the operating-business compounding alongside.

Re-read points: Arashi Vision below 130 yuan or above 250 yuan changes the math; the first disclosed Insta360 sale by Xunlei confirms management willingness; Q1 and Q2 2026 earnings.

Bottom Line

A Chinese-domiciled internet operator trading at less than a third of audited net asset value. A Shanghai-listed equity asset on the balance sheet worth almost two and a half times the entire market cap. A subscription cash cow alone worth more than half the company is selling for. A four-week catalyst published in a prospectus.

Not a free lunch, there are none, but worth a closer look don’t you think?

Position disclosure

At time of publication, I hold a long position in XNET expressed via stock and call options.

References

[1] Xunlei Limited, Form 20-F for FY ending 31 December 2025, filed with the SEC on 28 April 2026. Consolidated Balance Sheets (cash $157.0m + short-term investments $148.2m + restricted cash $0.8m = $306.0m liquid; bank borrowings current $37.2m + non-current $38.4m = $75.6m). Note 6 (long-term investment in Arashi Vision: $1,050.6m fair value at 31 December 2025; approximately 7.8% equity interest). Note 12 and segment-revenue disclosure for Subscriptions, Cloud Computing, Live Streaming.

[2] Mark-to-market 13 May 2026: 31.28m Arashi Vision shares (= 401m total shares × 7.8% per Stock Analysis / Yahoo Finance public records) × CNY 214 closing price ÷ USD/CNY 6.791 (EODHD) = US$985.5m.

[3] EODHD fundamentals pull, 2026-05-13 close. Tencent Music P/S 3.24×, Bilibili P/S 2.21×, iQIYI P/S 0.30×, JOYY P/S 1.38×, NetEase P/S 4.83×.

[4] Mordor Intelligence, 360-Degree Camera Market; Grand View Research, Action Camera Market. Market-share commentary on Insta360 / DJI / GoPro.

[5] Stock Analysis (stockanalysis.com), Arashi Vision Inc. (SHA: 688775); Xunlei Limited (NASDAQ: XNET). Share price history and trading metrics.

[6] Lexology, In review: governing rules for IPOs in China. Hankun Law and KPMG STAR Market lock-up framework summaries; Arashi Vision STAR Market listing announcement (上市公告书), 11 June 2025; 36氪, “影石创新科创板上市”, 11 June 2025.

[7] PwC, China Tax Summaries: Corporate Income Tax, capital-gains treatment of listed-equity sales by PRC corporate sellers; Cayman / Hong Kong dividend-withholding treatment.

[8] Investing.com, Xunlei sets new $20 million share repurchase program, 4 June 2024; subsequent quarterly buyback disclosures in 20-F.

[9] Sohu.com Limited, Sohu.com Announces Completion of Changyou Going-Private Transaction, PR Newswire, 17 April 2020. Comparable Chinese-ADR-holdco-to-portfolio monetisation precedent.

[10] U.S. Public Company Accounting Oversight Board, Statement on PCAOB inspection access in mainland China and Hong Kong, 15 December 2022.

Research, not investment advice. Stray Narratives is the publishing arm of an investment-research operation; positions are disclosed alongside the analysis where they exist. Past performance does not guarantee future returns. Full disclaimer at straynarratives.com/p/disclaimer.

whatever happened with this? the shares have trended lower and lower...