Blood in the Orchards

Stray Narratives, Issue 16 - Ad-Hoc: Select Harvests (ASX:SHV) - Almond supply is being bulldozed, and the lowest-cost grower trades below its asset value.

Stray Narratives is published when the market demands a closer look. Nothing in this publication constitutes investment advice. All views are those of the author. Please read our full disclaimer.

Another free article, so please like & share if you enjoy it!

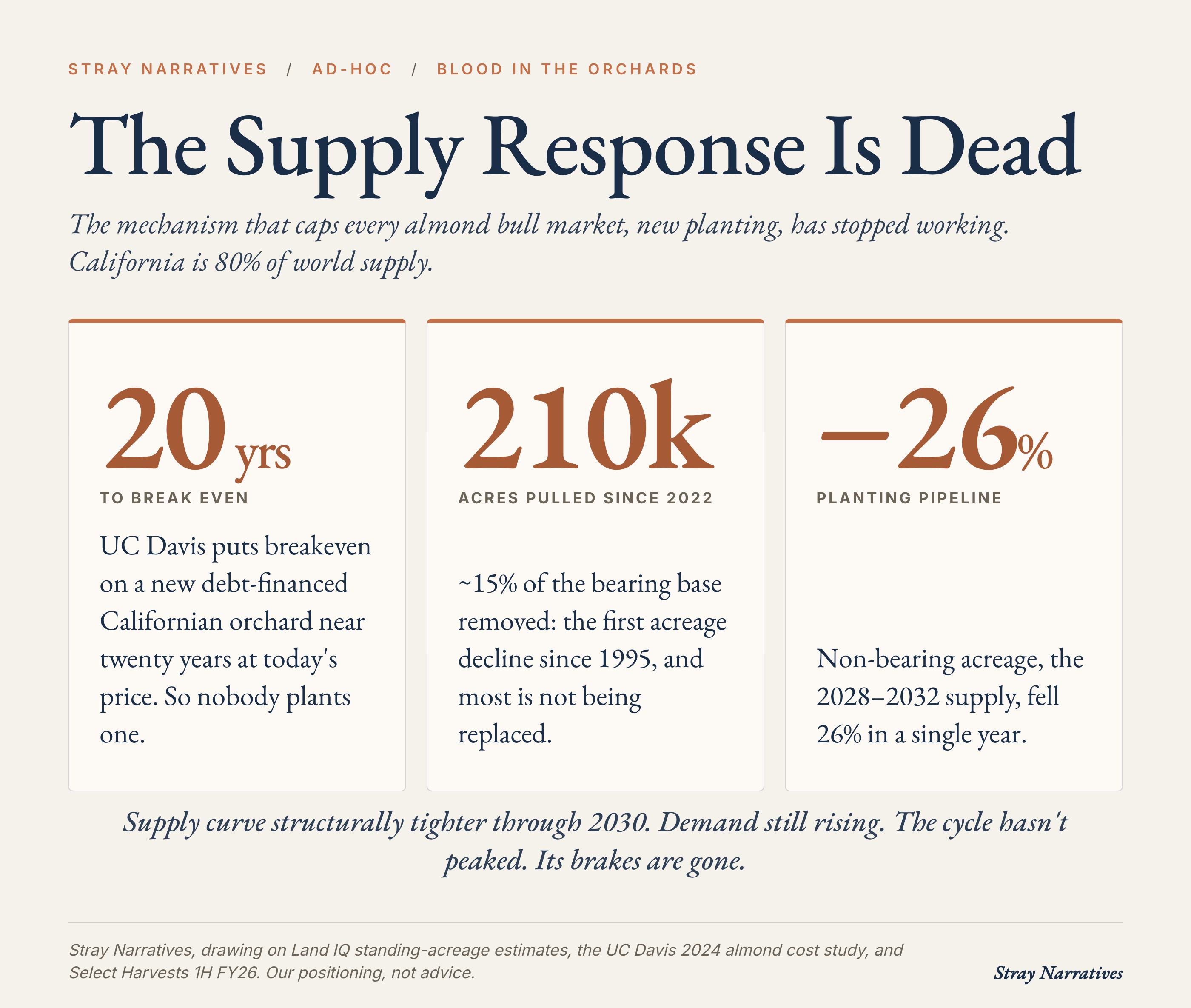

In the Central Valley of California, farmers are ripping more than 210,000 acres of almond trees out of the dirt.

They aren’t doing this to rotate crops. They are doing it because the maths of the last decade has completely broken. The University of California, Davis recently ran the numbers on planting a new almond orchard: factoring in land, trees, water, ten years of capex, and debt service, a debt-financed grower now needs roughly twenty years to break even at today’s price deck near US$2.70 a pound, and about twelve years even with no land debt to service [1].

Nobody invests with a twenty-year breakeven. Twenty years is not an investment horizon; it is a sentence. The margin of safety is gone, marginal growers are walking away, and the supply response that historically kills almond bull markets is dead.

An almond tree bears its first crop in year three, reaches full yield around year seven, and produces for roughly twenty-five years before the orchard is replaced. Supply is set the better part of a decade in advance, and it cuts both ways: the planting that should feed 2030 is not going into the ground, and the trees being pulled now will not come back at these economics.

But while California capitulates, the cycle break has opened an asymmetric mispricing 12,000 kilometres away.

I am adding Select Harvests (ASX:SHV) as a trade at the open, at roughly A$3.93. The trade is the global almond cycle break, expressed through the lowest-cost producer outside California, with a revenue tailwind from US-China tariff arbitrage and a share price trading at a steep discount to its hard assets.

Here is why the cycle is broken — and why the downside on this trade is bound by physics rather than by market sentiment.

The Ultimate Capitulation Signal

When an industry quietly stops publishing the data that historically hurt its prices, that is not a methodology change, it is a confession. It is the agricultural equivalent of a struggling tech company quietly retiring quarterly guidance.

In December 2025, the Almond Board of California voted to stop funding the USDA Objective Measurement Report — the rigorous July estimate, built on physical orchard sampling, that historically corrected the looser May grower survey [1]. The timing gives away the motive. The vote came months after the July 2025 estimate landed high and triggered the single largest one-day almond price drop in modern memory [1]. Confronted with the one number that reliably delivered downside surprises, the industry chose to stop publishing it rather than argue with it. Officially, the reason was accuracy. Read it however you like — but an industry quietly euthanising the data that keeps embarrassing its prices is not the behaviour of people who think supply is about to flood.

The data backs the tell. California controls 80% of global almond production, so what happens in the Central Valley dictates the cycle [2]. Three things are happening at once:

Removals are unprecedented. Land IQ data show more than 210,000 acres — roughly 15% of bearing acreage — pulled since 2022, including about 67,000 in 2024 alone. In 2026, California’s bearing almond acreage fell for the first time since 1995 [2].

The pipeline has collapsed. Non-bearing acreage, the leading indicator for production three-to-seven years out, fell 26% year-on-year. The supply that should feed the 2028–2032 window simply will not exist [2].

The marginal acre is uneconomic. Westlands Water District, historically the largest destination for new plantings, planted essentially zero new acres in 2023 and 2024, as water costs sat structurally elevated under California’s Sustainable Groundwater Management Act (SGMA) [2].

Combine that with Australian output running broadly flat toward 2030 as growers replant rather than expand, and structural drought across Spain’s growing regions, and the global supply curve is locked. Meanwhile demand keeps climbing — on tariff-driven Chinese buying, Indian consumption, and the developed world’s determination to put almonds in everything that once contained milk.

Capital Allocation: Utility Over Signalling

The market is pricing SHV on cyclical fear, assuming we are near a top. Management is quietly arbitraging that behavioural error with a textbook capital-return playbook [3].

After a strong 1H FY2026 result, the board announced a 10% on-market buyback — around 14.2 million shares, 10% of the issued capital — and resumed the interim dividend. It also secured a new A$60 million debt facility on favourable terms, not for distressed working capital, but to shrink the float at a depressed valuation [3].

This is the unglamorous version of smart capital allocation: financial utility over market signalling. Buying a dollar of productive almond orchard for eighty cents is not a sophisticated manoeuvre — it is just an unfashionable one. And the mechanics are cycle-proof: a 10% reduction in the share count lifts earnings per share by roughly 11% on a flat earnings base, entirely independent of where almond prices go next.

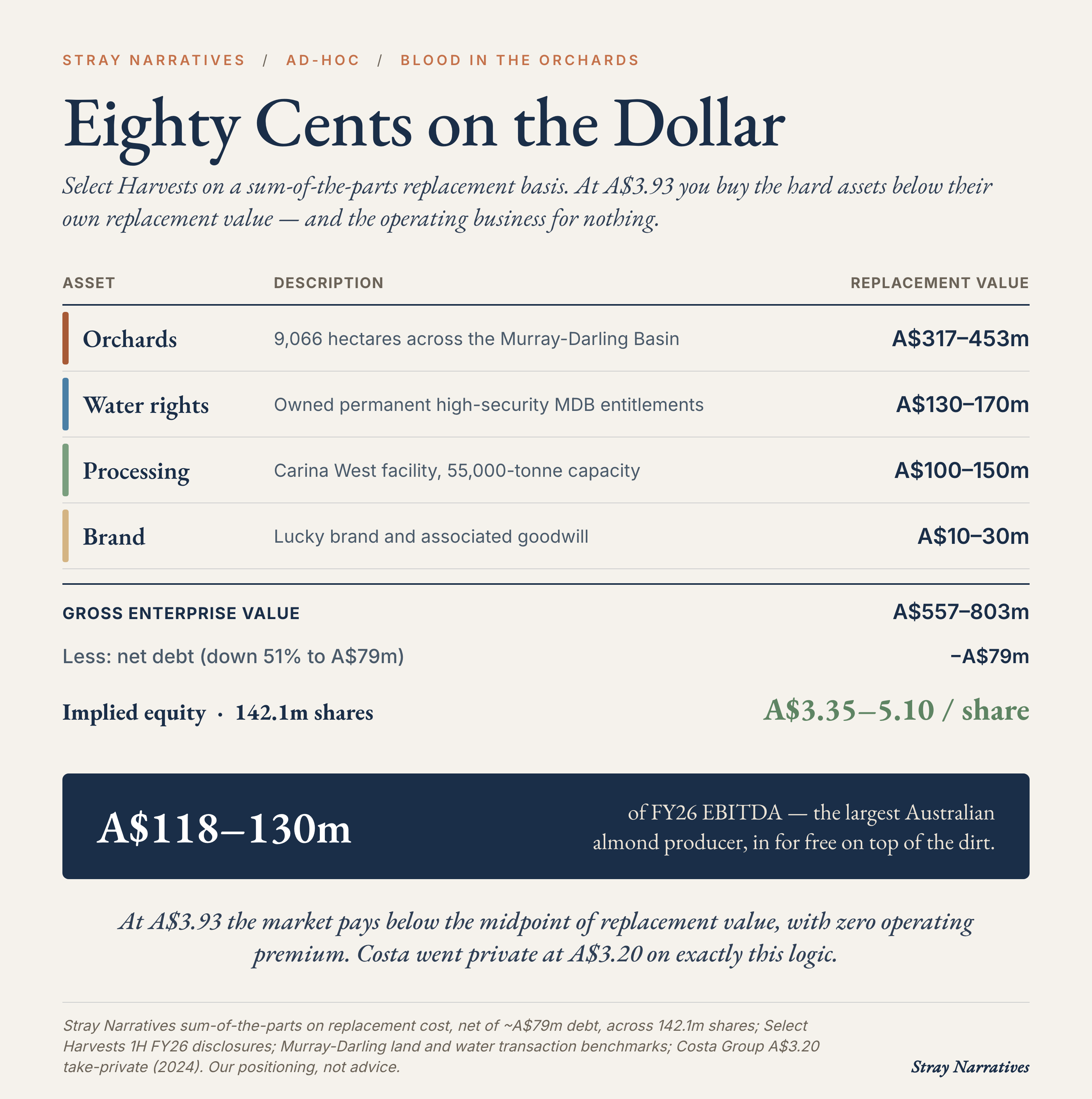

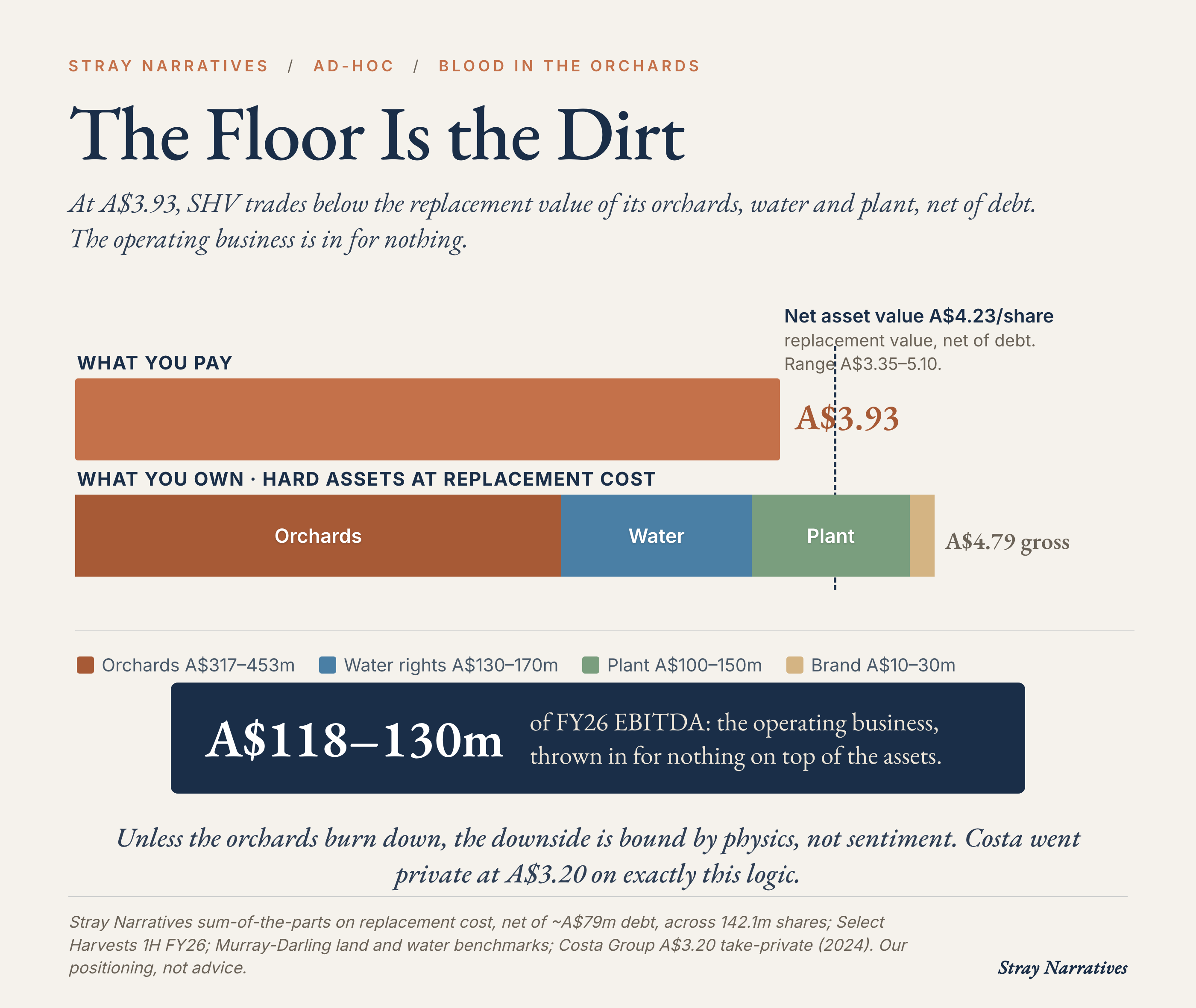

The Asset-Backing Floor

Replacement-cost analysis is the discipline that stops a cyclical equity from becoming a cyclical trade. On a sum-of-the-parts replacement basis [3][4]:

That is an enterprise value of A$557–803 million. Strip out net debt of roughly A$80 million — down 51% to A$79 million at the last full year — and, across 142 million shares, the implied equity sits at A$3.35–5.10 per share [3][4].

At around A$4.00, the market is paying for the assets at below the midpoint of their own replacement value, with zero operating premium. You get the largest Australian almond producer — A$118–130 million of FY26 base-case EBITDA — thrown in for free on top of the dirt [3].

Unless the orchards literally burn down, the hard assets bind the downside around A$3.30–3.50. Below that, the assets are worth more than the equity, which makes a private buyout increasingly plausible — the kind of valuation that tends to attract people with cheque books and patience. Precedent: Costa Group went private at A$3.20 in 2024 on exactly this sub-replacement logic [4].

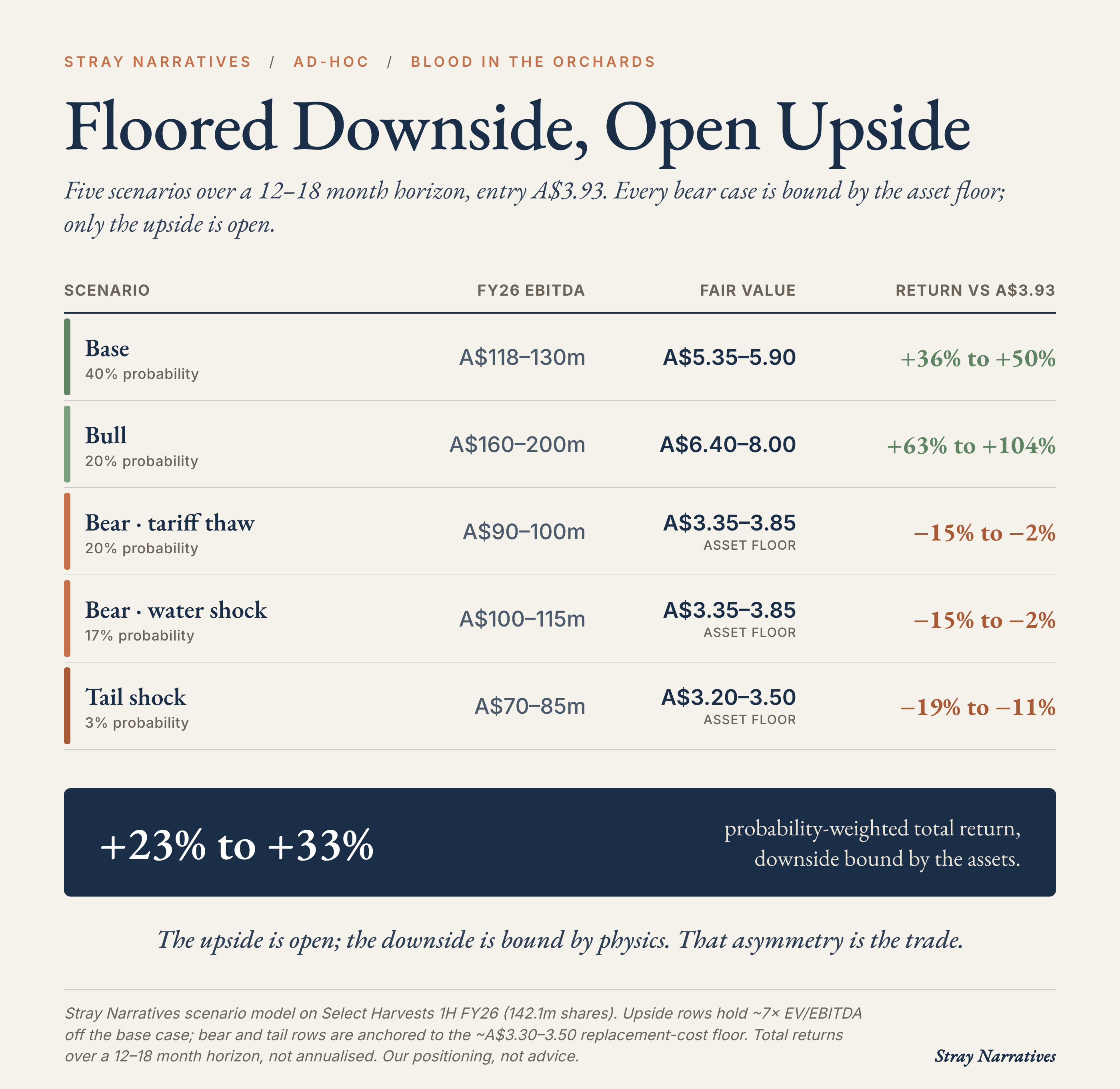

Reality Check: The Bear Cases

A thesis is only as strong as its weakest link. Here is what breaks this trade, in order of probability.

1. A Trump-China tariff thaw (~12–15%). Australian almonds have been winning share in China on the US-China tariff differential. A partial agricultural deal in late 2026 or 2027 narrows that gap and reroutes Chinese buyers back toward US origin. Impact: a 15–20% cut to the realised-price assumption.

2. A Murray-Darling water shock (~8–12%). This is the hidden leverage in the model. SHV owns the permanent rights to only about 18% of the water it needs and sources the rest from the allocation market — which is to say, from the spot market and the goodwill of the sky. Under El Niño conditions, Australian allocation prices spike viciously (A$300+/ML) [4]. In a concurrent drought, global almond prices rise but SHV’s unit margins compress as spot water costs bite. Impact:15–25% off EBITDA in the affected year — though the hard-asset floor still protects the equity base.

3. Tail shocks (~3–5%). August-September frost, or a resurgence of the varroa mite that hit Australian hives in 2022. Impact: a 20–30% drawdown.

The unifying point: in every realistic bear case, the asset floor binds. Outside the tail scenario, SHV does not go meaningfully below ~A$3.30 without the assets being worth more than the equity. The downside is capped by physics, not by sentiment.

Position and Expected Return

Adding SHV to the list at the open, ~A$3.93, for a 12-to-18-month window — with optionality to extend into the 2028–2030 production gap if the supply-destruction story fully materialises.

*Fair values recomputed on the corrected 142.1m share count (the 1H result confirmed 142.1m, not the 152m the original model used). Upside rows hold a ~7× EV/EBITDA backed out of the base case; bear and tail rows are anchored to the ~A$3.30–3.50 asset floor. These are total returns over the 12–18 month horizon, not annualised. Probability-weighted, the trade carries roughly +23% to +33%, with the downside floored by the assets — a sharper asymmetry than the original model showed, because fewer shares lift every per-share figure and the buyback is retiring stock below replacement value.*

What would make me add: California’s 2026 crop confirmed at ≤2.65 billion pounds; Murray-Darling allocation easing below A$120/ML; FY26 EBITDA tracking above A$130 million. What would make me trim: a US-China deal that narrows the tariff differential; spot water sustained above A$250/ML for two quarters; FY26 EBITDA tracking below A$95 million.

Bottom line. The cycle is not at its peak. The cycle has broken. New orchards do not get planted at twenty-year breakevens, the pipeline has collapsed, and the industry has stopped publishing the number that used to keep it honest. Select Harvests is the cleanest way to own that break: capped downside bound by physical assets, asymmetric upside, and a management team compounding capital while everyone else is reading the cycle backwards. There is, occasionally, a free lunch in markets. It is usually buried under something nobody wants to look at — in this case, more than 210,000 acres of dead trees.

References

[1] University of California, Davis — 2024 Almond Cost Study (Sacramento Valley & Southern San Joaquin editions), for the new-orchard breakeven horizon; Almond Board of California position reports, including the December 2025 vote to discontinue funding the USDA Objective Measurement Report.

[2] Land IQ Standing Almond Acreage estimates (commissioned by the Almond Board of California; the USDA NASS standalone California almond acreage survey was discontinued), 2022–2026 — bearing removals (more than 210,000 acres / ~15% since 2022; first bearing-acreage decline since 1995, 1,401,097 → 1,385,870), the ~26% drop in non-bearing acreage to the 2025 final (142,306 → 104,900), and Westlands Water District / Land IQ planting data; California ≈ 80% of global production (International Nut & Dried Fruit Council). (SGMA — California’s Sustainable Groundwater Management Act — is the regime behind the elevated marginal-acre water costs.)

[3] Select Harvests 1H FY2026 results announcement and presentation, 28 May 2026 — FY26 EBITDA guidance, the 10% on-market buyback, A$60m debt facility, resumed interim dividend, and orchard / processing / water-entitlement asset disclosures.

[4] Asset-floor anchors — Australian agricultural land and water transaction benchmarks (incl. Murray-Darling Basin entitlement and allocation pricing) and the Costa Group / Paine Schwartz Partners take-private at A$3.20 (completed early 2024; asset-backed precedent).