Is Now the Time to Invest in Nuclear?

Stray Narratives, Issue 08

Stray Narratives is published when the market demands a closer look. Nothing in this publication constitutes investment advice. All views are those of the author. Please read our full disclaimer.

There is a particular kind of investing frustration that is worse than being wrong. It is being right, structurally, fundamentally, analytically right, and watching the market ignore you with complete serenity while you pay the opportunity cost in silence. Uranium investors have been living in this frustration for three years.

The structural case for uranium has been broadly correct since at least 2022. Supply runs structurally short of demand. The deficit is widening. The world’s largest producer keeps cutting guidance. Reactor construction is accelerating. Utilities must contract. There is no substitution, no switching, no clever workaround. And yet: the spot price peaked at $107 per pound in February 2024 [1] and has since drifted. Equities have underperformed indices. Meanwhile, for a period in late 2024, Dogecoin’s market capitalisation exceeded the entire tradable uranium equity universe by roughly two billion dollars [2], which tells you everything you need to know about what the market was thinking about and what it was not.

The question I want to address is not whether the thesis is right. It is whether the clock has finally aligned with it, and, more usefully, where in the nuclear investment universe the thesis is actually still available to buy.

The Accounting Argument

The structural case can be stated briefly because it does not require much elaboration. It is closer to accounting than forecasting.

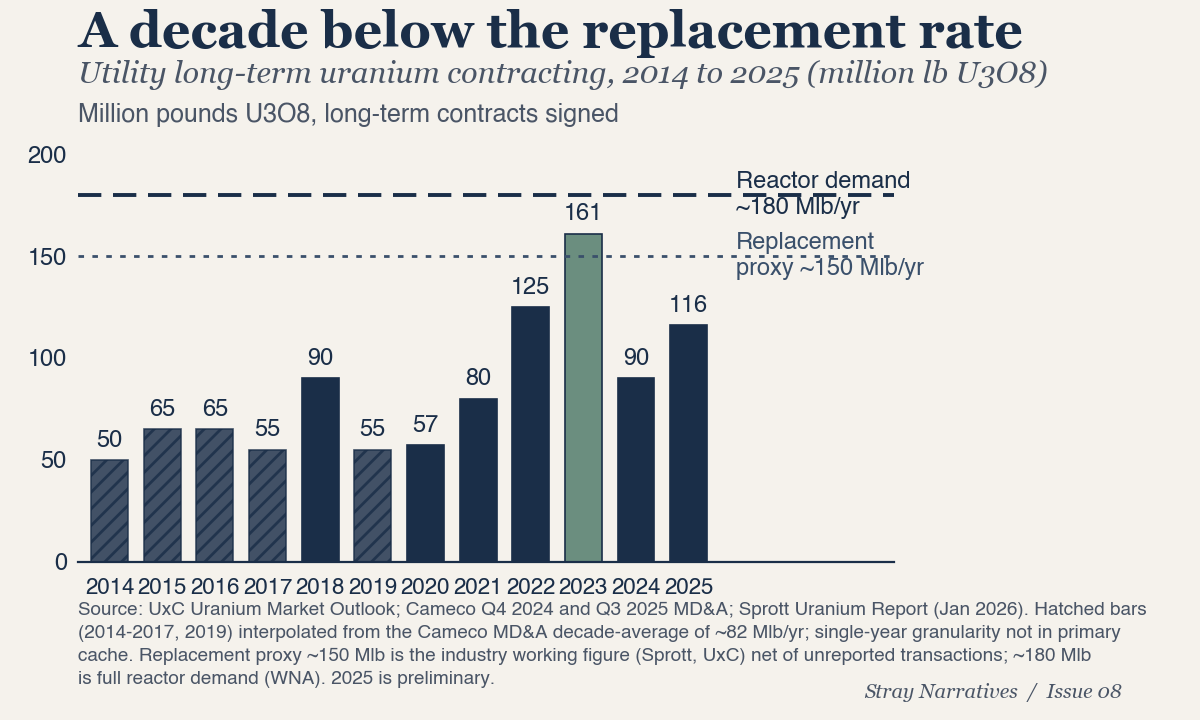

Global uranium demand runs at approximately 180 million pounds per year, consumed by 440 operating reactors and 65 more under construction [3]. Primary mine supply produces roughly 140 to 150 million pounds per year [3]. That gap does not close easily: new uranium mines take ten to fifteen years from discovery to production, and a decade-long bear market between 2011 and 2021 starved exploration. The pipeline of new supply is thin relative to what the demand trajectory requires.

Kazakhstan, through its state producer Kazatomprom and its joint-venture partners, is responsible for approximately 45 percent of global primary supply. Kazatomprom confirmed its 2026 production guidance cut across its Q4 2025 operations update in January and its 2025 full-year results in March [4]. This follows a multi-year pattern of underperformance driven by sulphuric acid supply chain constraints that show no signs of resolving. Their inventories sit at a ten-year low: four months of production [4]. These are not the numbers of a producer about to rescue the market.

The one element that makes uranium demand unlike almost any other commodity is that it is contractually predetermined. Utilities sign long-term supply agreements years before they need fuel. Once a reactor is built, it runs for sixty years regardless of the uranium price. Demand is not a guess. It is a schedule. The question has never been whether the market would eventually tighten. It has always been when utilities would be forced to recognise what the schedule requires.

The Market Has Already Voted, Just in the Wrong Place

Here is the observation that changes the shape of the question.

This is the kind of error the publication has described before as a wrong-map problem: the market is reading the map confidently, just not the map that matters.

The market has not, in fact, ignored the uranium thesis. It has embraced it enthusiastically. It has just placed its bets in the wrong instrument.

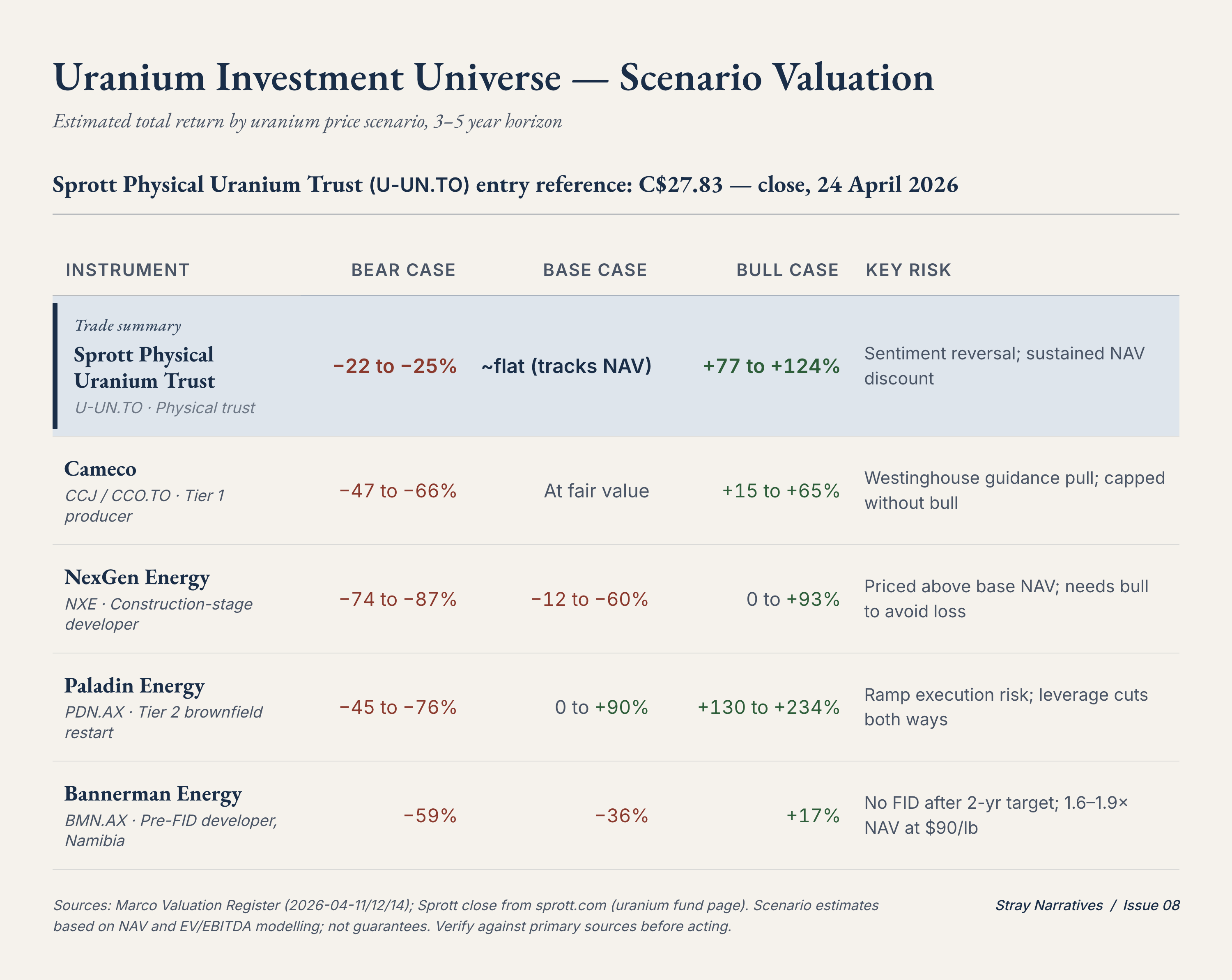

Nuclear equities and developers have been re-rated substantially over the past three years. NexGen Energy, the company sitting on what may be the largest and highest-grade undeveloped uranium deposit in the world, trades meaningfully above its base-case net asset value at current uranium prices. The stock requires the full bull scenario, uranium at $150 per pound or more, simply to avoid losing money at today’s price. Cameco, the senior miner and the closest thing the sector has to a blue chip, is priced at base-case fair value, which sounds reasonable until you realise that base case offers limited upside from current levels and the bear case still takes forty-seven to sixty-six percent off.

SMR stocks, the small modular reactor developers, are in a category of their own. These are companies whose products will not reach commercial scale until the 2030s at the earliest. The stocks trade on narrative, and the narrative is at least a decade ahead of the physical reality.

The result is a strange inversion. Across the nuclear investment universe, the market has already answered the question “will the thesis play out?” with a fairly confident yes. It just expressed that answer through the equities rather than through the commodity.

The uranium price itself has not moved to reflect this. Physical uranium, held through vehicles like the Sprott Physical Uranium Trust, trades near net asset value [8]. The bull case upside, if the contracting cycle fires and prices move toward $120 to $150 per pound, is roughly seventy-seven to one hundred and twenty-four percent from current levels. The bear case, if the thesis is wrong or delayed, is a loss of twenty-two to twenty-five percent.

That is a meaningfully different risk profile than a developer priced for resolution. The equity market has been enthusiastically pricing in a thesis that the commodity market has not yet confirmed. When those two things diverge, one of them is wrong. They are rarely both right.

What Would Actually Signal the Clock Has Aligned

The structural case being correct and the clock being correct are separable skills. Uranium has a long track record of making fools of people who confused the two. So what would actually signal the thesis is firing, rather than merely strengthening?

Three conditions matter:

Utility contracting at or above replacement rate. The replacement rate is approximately 180 million pounds per year. In 2024, global contracting ran at roughly 90 million pounds: half the replacement rate [5]. The majority of that was Chinese and Ukrainian utilities, not the Western utilities whose behaviour drives the price. Q4 2025 showed the first real contracting inflection. That is a necessary beginning, not a sufficient signal.

Kazatomprom’s inventory buffer exhausted. Guidance cuts are necessary but not sufficient. They tell you supply is running slow. What matters is when the buffer is gone. At four months of production and declining, that point is getting close. When it arrives, the physical tightness becomes unavoidable rather than theoretical.

Long-term contract price moving decisively above current levels. The long-term price sits at approximately $90 per pound [7]: already the highest level in history at the beginning of a contracting cycle, which is itself an extraordinary fact. But utilities signing contracts in volume at $90 and above is qualitatively different from the price sitting at $90 because nobody is signing anything.

Where Each Signal Stands

The honest assessment against that framework:

Kazatomprom’s guidance cut is confirmed as structural, not temporary. The first condition is advancing materially. NexGen received its construction licence from the Canadian Nuclear Safety Commission on 5 March 2026 [6]. The largest undeveloped uranium deposit in the world is now a project under construction, removing what had been the thesis’s most significant binary risk. These are real developments.

And yet the contracting inflection of Q4 2025 remains, by definition, an inflection from a very low base. Utilities remain substantially under-contracted relative to their forward needs. The long-term price has not moved decisively. The Sprott trust is roughly at net asset value, not at a sustained premium, which would signal Sprott’s buying mechanism re-engaging in earnest.

The trigger has not fired but the conditions for it are the most advanced they have been.

The Genuine Uncertainty

The uranium market has a specific and well-documented failure mode: the “imminent inflection” call. The number of analysts who correctly identified the structural deficit and incorrectly identified the timing is large. Utilities have demonstrated a remarkable capacity to remain under-contracted for longer than any reasonable person expected. They have kept finding levers (secondary market purchases, existing inventory, creative procurement) that have deferred the moment of reckoning further than the supply-side arithmetic suggested was possible.

There is also a consensus problem. Every major research house is bullish uranium. Two significant catalysts, the NexGen licence and the Kazatomprom confirmation, are now public information, available to every market participant. When a trade becomes consensus, the variant perception that generates returns has largely been captured. The setup is not the same as it was in 2020 when the thesis was lonely.

This is not an argument that the thesis is wrong. It is an argument that “the thesis is right” and “now is the optimal entry point” are different claims, and the second is harder to make than the first.

Being right and being paid are separable. When a structural case is lonely, the early mover earns both the fundamental return and the re-rating as consensus arrives. When the case is consensus, the re-rating has already happened, or is happening, and only the fundamental return remains. The structural reality stays intact. The edge compresses anyway. The sharpest version of this for uranium is right thesis with wrong timing: you hold the position for eighteen months of cost of carry and foregone returns elsewhere, then exit flat when the thesis finally fires for the next cohort.

What the Disciplined Investor Does

The consequence is that instrument selection matters more than the timing call. Sprott at NAV preserves the asymmetry at the commodity level even if the equities have already de-rated the edge.

The answer to “right thesis, uncertain clock” is not to wait for certainty. Certainty arrives after the move. By the time the contracting cycle is visibly firing, with utilities scrambling, spot price spiking, and headlines appearing, the easy money is already made.

But neither is the answer to bet heavily on precise timing. The track record of “imminent inflection” calls in uranium specifically argues against that.

The distinction that matters is between conviction sizing and timing sizing. If the structural case commands genuine conviction, and the accounting above suggests it should, the position should reflect that conviction. But it should be sized for the possibility that the clock is still twelve to twenty-four months from aligning, not sized as though the move is imminent. There is a cost to being early, and that cost is real and should be acknowledged honestly rather than wished away.

The epistemically cleanest vehicle remains physical uranium via Sprott. It provides direct exposure to the commodity without operational risk, without relying on any individual miner to execute a multi-year construction project in a difficult jurisdiction on a schedule and within a budget. Miners offer leverage to the upside. The leverage cuts both ways, and most of the accessible miners have already priced in a version of the bull case that the commodity itself has not yet confirmed.

The reason Sprott at NAV is the right vehicle, and not merely an available one, is mechanical. When the units trade at a premium to net asset value, the trust issues new units at the market, uses the proceeds to buy physical U3O8, and stores it in licensed facilities. Spot demand gets created mechanically, and the trust’s accumulation itself tightens the market. The NAV premium is therefore the leading indicator: when it widens, Sprott is buying, and the feedback loop is firing.

When the units trade at or near NAV, the at-the-market issuance stops. No new units, no new uranium purchases, no mechanical spot bid. The mechanism has not broken. It is dormant, waiting for the premium to return. Buying near NAV is buying ahead of the bid, not alongside it.

Sometimes the most sophisticated thing you can do in a crowded trade is to go back to the underlying. The equity market has been buying the thesis. The commodity has not moved yet. One of those is closer to the price that will matter.

References

[1] UxC Uranium Market Outlook, historical spot price series, February 2024. [Spot peak of $107/lb.]

[2] CoinGecko and Sprott Uranium Miners UCITS ETF constituent market-cap aggregation, Q4 2024 snapshot. [Dogecoin market cap vs tradable uranium equity universe.]

[3] World Nuclear Association, “World Nuclear Power Reactors & Uranium Requirements,” updated 2026. [Operating reactor count, reactors under construction, annual uranium demand, and primary mine supply figures.]

[4] Kazatomprom Investor Relations, “4Q 2025 Operations and Trading Update” (January 2026) and “2025 Full-Year Results” (March 2026), kazatomprom.kz. [2026 production guidance cut; inventory at four months.]

[5] UxC Contracting Volume, calendar year 2024. [Global utility contracting at approximately 90 million pounds.]

[6] Canadian Nuclear Safety Commission, Rook I construction licence decision, 5 March 2026, nuclearsafety.gc.ca. [NexGen construction licence issuance.]

[7] UxC and TradeTech long-term price indicators, April 2026. [Long-term price at approximately $90/lb.]

[8] Sprott Asset Management, Physical Uranium Trust (U.UN/U-UN.TO), NAV pulled 2026-04-20, sprott.com. [Premium to NAV of +0.56%, i.e. trust trading at net asset value.]