The Case for China

Stray Narratives, Issue 13 - Trading the Gap Between Perception and Reality

Stray Narratives is published when the market demands a closer look. Nothing in this publication constitutes investment advice. All views are those of the author. Please read our full disclaimer.

Markets anchor to trauma. When an asset class burns investors badly enough, as Chinese equities did through the tech crackdowns, zero-COVID lockdowns, and the property collapse, the consensus simply stops looking at the data. The narrative hardens into a single word: uninvestable.

But the market’s refusal to look is exactly where the alpha lives.

Right now, China is quietly handing us three massive, structural tailwinds firing simultaneously:

Cloud and AI pricing power is expanding.

The consumer is shifting from defensive hoarding to equity participation.

The real estate drag is finally finding a floor.

The country has not seen these three pillars align in over a decade.

Yet, because the crowd is still trading the trauma of 2022, the biggest beneficiary of the global AI boom is being priced as if the AI revolution is passing it by entirely.

At the open, I am adding KWEB (China internet) and MCHI (broader China) to the model portfolio, sized for a 12-to-18-month window. MSCI China is currently trading at roughly 12.6x consensus 2026 earnings. Compare that to the S&P 500 at 21.4x. They are posting broadly comparable EPS growth, yet you are getting the Chinese tech-internet segment, which is actually growing faster than the US aggregate, at a 41% discount [1].

I am not playing for a dead-cat bounce but a potential structural rerating. Here is the case for why I am making this move.

Pillar 1: The new era of tech pricing power

To understand the Chinese tech opportunity, you have to look at the global compute market. Compute is structurally scarce. Through 2024 and 2025, the AI story was about land grabs and volume as companies subsidized access to build their user bases.

Today, that phase is over. Pricing power has taken the wheel. Anthropic stopped subsidizing enterprise plans this spring, and per-token prices have jumped [2]. Customer demand has vastly exceeded installed capacity globally, meaning the providers now hold the pen on price. The race-to-the-bottom on per-token cost has officially reversed.

The West operates under the assumption that China is locked out of this dynamic due to semiconductor sanctions, but the data says otherwise.

According to Stanford’s 2026 AI Index, the US-China frontier-model performance gap has collapsed from 17.5% in 2023 to just 2.7% today [3]. Chinese models are running roughly 12.6 trillion tokens per week (quadruple the US volume in recent tracking) [4], and they are doing it at 8% to 14% of the unit cost of leading US closed-frontier models [5]. China is running the AI economy on a vastly steeper, cheaper domestic demand curve.

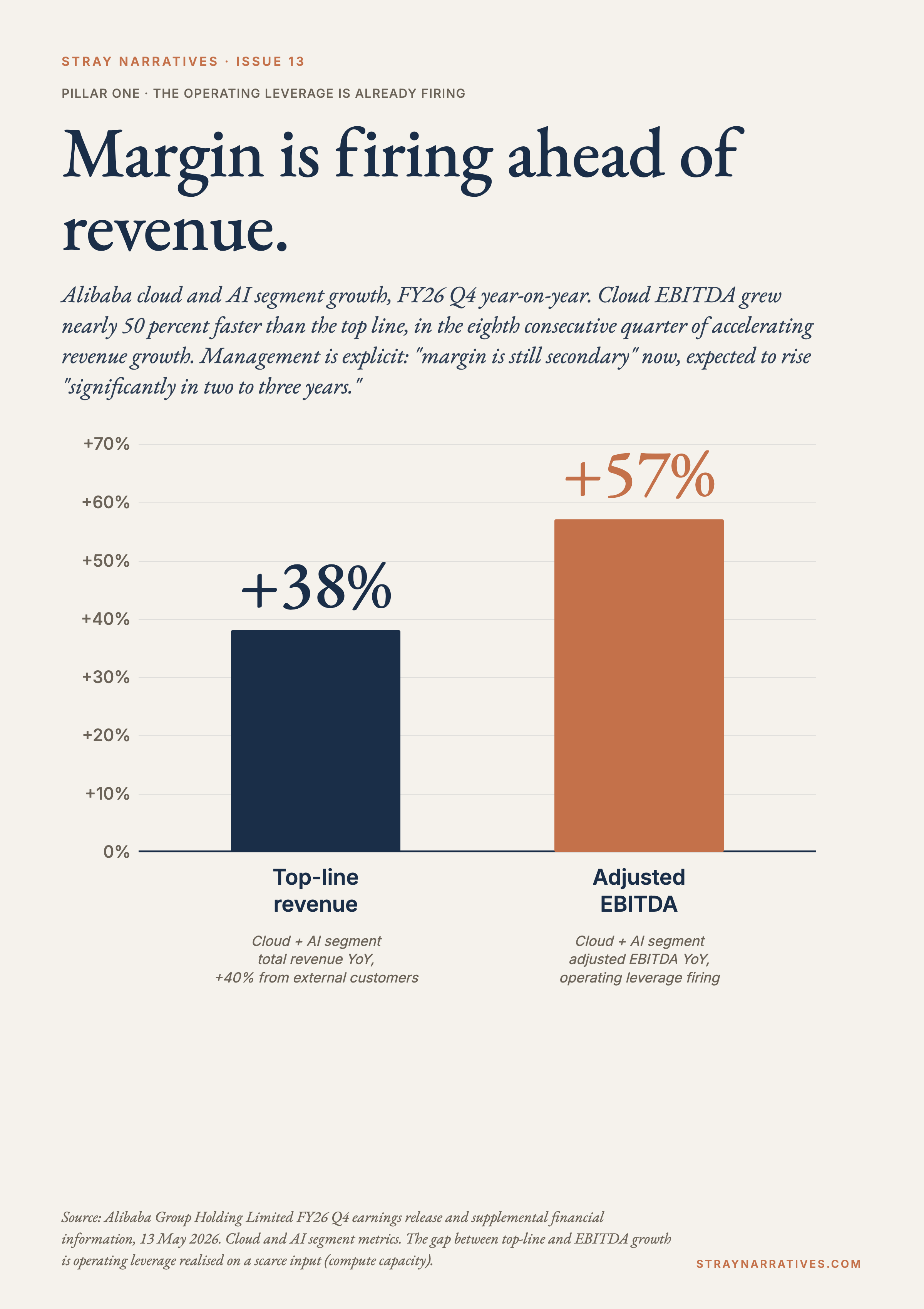

When a scarce input meets immense demand, you get multiple expansion and profitability acceleration at the same time. Alibaba is the cleanest proof of concept. In their FY26 Q4, cloud and AI revenue grew 38% year-over-year. But more importantly, cloud and AI adjusted EBITDA grew 57% [6].

That 19-point spread between revenue growth and profit growth is the sound of operating leverage firing on all cylinders. The capex is already yielding cash. As Alibaba CEO Eddie Wu put it on the 13 May earnings call:

“There isn’t a single card on our service that is idle... we have a lot of customers still waiting to access the service.” [6]

Pillar 2: The saver-to-investor rotation

The persistent bear argument against China is the lack of a “bazooka” fiscal stimulus to revive the consumer. What this argument misses is that a second stimulus event isn’t necessary. The capital is already sitting on the household balance sheet; it just needs a reason to move.

Over the last few years, the Chinese consumer played aggressive defense. But the premium tier is turning. Alibaba’s 88VIP membership (their top-decile capture) hit 62 million in Q4, with growth accelerating to 24% [6]. Merchant ad spend on the platform is accelerating [6]. This is wallet-share capture among the knowledge-economy professionals in Hangzhou, Shenzhen, and Shanghai who are already reaping the AI windfall.

The mechanism that turns this premium-tier spending into broad market participation is financialization. There is a towering 50 trillion yuan wall of one-year-plus deposits maturing in 2026. In Q1 alone, 7.6 trillion yuan landed in personal deposits [7].

But savers are waking up to the reality that parking cash in defensive assets is a dead end. In January 2026, the China Securities Depository and Clearing Corporation reported 4.9 million new individual investor accounts, the highest monthly print since the stimulus peak in late 2024 [8]. The retail investor is beginning to speculate in equities again on a scale we haven’t seen since the 2014-2015 cycle. The cash is migrating to the stock market and the impact compounds.

Pillar 3: Property is clearing

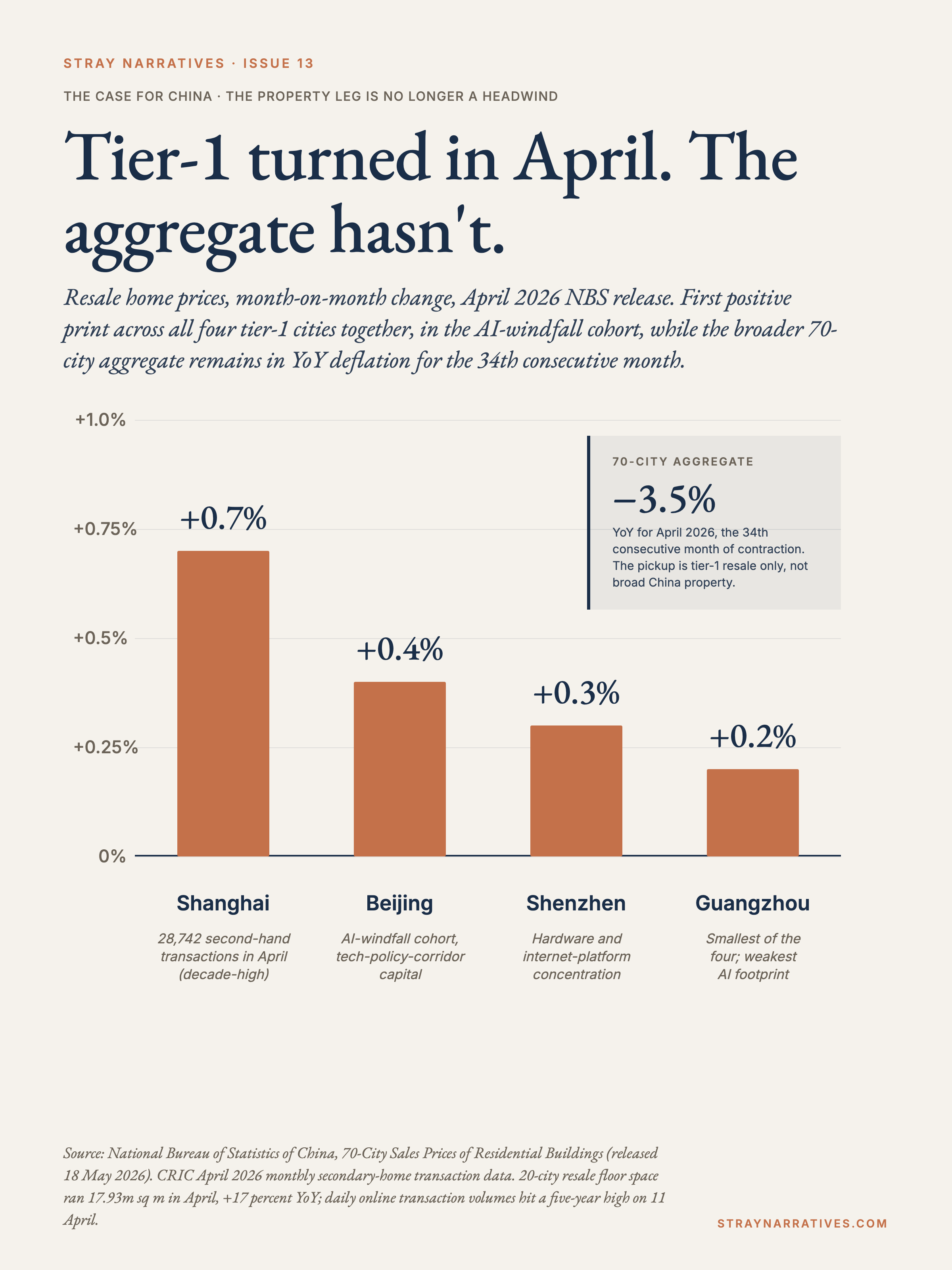

I am not making a sweeping, optimistic call on Chinese real estate. The aggregate numbers across 70 cities are still in deflation [9]. But to use the aggregate as a reason to avoid China is lazy analysis.

What matters to the broader equity indices is that the drag is effectively capped, and in the areas that matter, the market is clearing.

First, Tier-1 resale has officially turned positive. In April, Shanghai, Beijing, Shenzhen, and Guangzhou all printed positive month-over-month price action [9]. Shanghai just recorded its highest secondary-home transaction volume for the month of April in a decade, surpassing the 2019 pre-crisis peak [10]. The recovery is highly specific to the AI-windfall cohort cities, and it is widening.

Second, and more importantly, the supply side has been obliterated. New construction starts are down more than 70% from their peak [9]. Developers are solely focused on completing existing projects.

This mirrors the exact mechanics of the Spanish and Irish real estate markets in 2014 and 2015. When you completely halt new supply, the residual inventory gets absorbed, prices flatten, and the sector stops being a black hole for GDP. The math points to a transition in 2027 where property actually shifts from a drag to a contributor. Until then, it is simply no longer the weight that sinks the ship.

The reality check: what could break this trade

I take the failure points seriously. Here is what can go wrong:

The AI capex air pocket. This is the most legitimate threat. The defense against a tech bust is the $1.9 trillion in aggregate Remaining Performance Obligations (RPO) logged by the Big Four hyperscalers. But that backlog is dangerously concentrated (Oracle’s $455B total RPO is roughly $300B in OpenAI commitments) [11]. Historically, suppliers re-rate the moment a major customer guides capex down, not when a bust is confirmed. If a US hyperscaler trims its 2027 capex guide by 10-15%, the Asian supplier base will compress 20-30% within a week. The Chinese internet leg is partially insulated by domestic demand, but it would not escape the gravity.

Geopolitics. A 41% multiple discount already prices in a heavy geopolitical premium. However, a Trump escalation (a blanket Section 301 tariff above 60% and an expanded Entity List) is the modal bear path. It would be worth a 10% to 15% net drawdown.

The policy regime. Central Huijin (the state fund) operates as a PBoC-backstopped floor, but it doesn’t buy for upside [12]. The implicit bet of this trade is that Beijing maintains its current pro-AI posture. If they revert to 2021-style platform crackdowns, the trade requires immediate liquidation.

The 90-day watchlist. I am actively monitoring the mid-June NBS release for any Tier-1 city resale flipping back to negative, alongside May PPI data and Alibaba cloud growth (a dip below 30% breaks the momentum thesis). I am also watching for any formal Beijing action constraining AI commercialization.

The playbook and expected returns

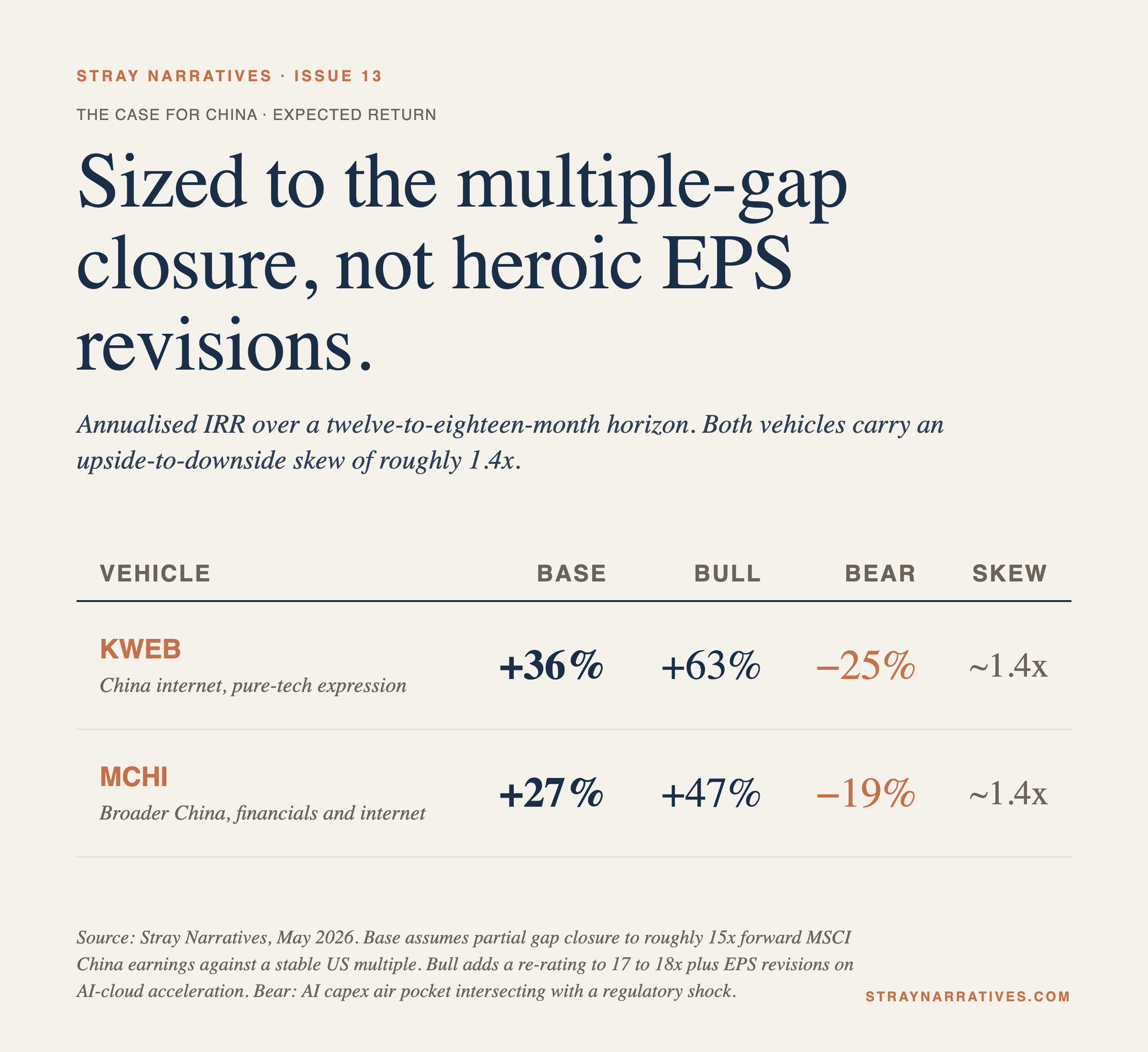

This is a timing-arbitrage trade, sized to capture the closure of the multiple gap rather than relying on heroic EPS revisions.

The Base case assumes a partial gap closure to roughly 15x forward earnings on MSCI China against a stable US multiple. The Bull case adds a re-rating to 17-18x plus upward EPS revisions on AI-cloud acceleration. The Bear case accounts for the AI capex air pocket intersecting with a regulatory shock.

JD.com is the multiple-recovery candidate at the defensive end of the KWEB basket. It trades at roughly 9 to 10 times consensus 2026 earnings against a balance sheet closer to a fixed-income instrument than to a Chinese e-commerce platform. The market is pricing it as if the franchise has permanently lost share to PDD and Meituan, which is not what the operating numbers say. JD bounds the downside of the basket if the broader AI rerating thesis takes longer than 12 months to play out.

Alibaba is the multiple-recovery candidate at the offensive end of the KWEB basket. The 57% cloud and AI EBITDA growth that anchored Pillar 1 is being priced at roughly 12 times forward earnings, against US peers trading at 25 to 30 times for materially less acceleration. The market still has Alibaba in the 2022-platform-crackdown frame even as the cloud segment compounds. If pricing power on compute holds, this is the name in the basket where EBITDA growth flows into the multiple first.

Bottom line

The financial media is treating Chinese equities as uninvestable value traps. But true value traps are defined by deteriorating fundamentals, shrinking margins, and capital flight. They do not exhibit 57% EBITDA growth in frontier technologies, a rapidly steepening domestic demand curve, and millions of retail investors rotating out of cash and into equities.

The dislocation between the dominant market narrative and the actual cash flows being generated on the ground is the widest it has been in ten years. You do not need a geopolitical miracle or a massive government bailout for this trade to work. You simply need the market to realize it is aggressively pricing in an apocalypse that is no longer happening.

References

[1] MSCI China and S&P 500 consensus forward P/E and 2026 EPS growth: MSCI factsheets (30 April 2026); S&P 500 consensus via FactSet aggregate.

[2] Anthropic enterprise pricing communications, spring 2026; OpenAI, Google Cloud, and AWS public API price lists through Q1-Q2 2026; NVIDIA earnings commentary on GPU pricing and inference wait-lists.

[3] Stanford Institute for Human-Centered AI (HAI), 2026 AI Index Report — frontier-model benchmark performance gap.

[4] OpenRouter weekly token-consumption analytics, late March / early April 2026; reporting via Bloomberg secondary coverage.

[5] DeepSeek V3.2 and GPT-5.2 published inference pricing per million tokens; benchmark comparisons from Inference.net independent compilation; Anthropic Claude Sonnet 4.5 published rate card.

[6] Alibaba Group Holding Limited, FY26 Q4 earnings release, supplemental financial information, and earnings call transcript (CEO Eddie Wu management commentary), 13 May 2026.

[7] People’s Bank of China, Quarterly Financial Statistics Q1 2026, released 13 April 2026.

[8] China Securities Depository and Clearing Corporation (CSDC), Monthly Investor Account Data, January 2026 release.

[9] National Bureau of Statistics of China releases, April 2026 cycle: 70-City Sales Prices of Residential Buildings (18 May), Producer Price Index (10 May), and new-construction-starts series.

[10] China Real Estate Information Corporation (CRIC), April 2026 monthly secondary-home transaction data.

[11] Hyperscaler RPO disclosures, Q1 2026: Microsoft, Alphabet (Q1 2026 Form 10-Q cloud RPO), Amazon, Oracle (FY26 Q1, $455bn total RPO). Aggregate roughly $1.9 trillion across the Big Four.

[12] Bloomberg reporting on Central Huijin Q1 2026 position adjustment and PBoC backstop commitment, April 2026; PBoC press communications on the Central Huijin lending facility.

Agree with most of this but in regard to cloud margins we have yet to see any real/true expansion yet…

BABA cloud has been at roughly ~9% EBITA margins for 8 consecutive quarters… all EBITDA growth is directly tied to revenue growth. I do think it will improve from here but only time will tell 🤷♂️