The Discount That Did Not Close

Stray Narratives, Issue 19 - Marking the Xunlei position to market, seven weeks after the four-week catalyst

Stray Narratives is published when the market demands a closer look. Nothing in this publication constitutes investment advice. All views are those of the author. Please read our full disclaimer. As always, please share this post if you enjoy it, that’s how it stays free!

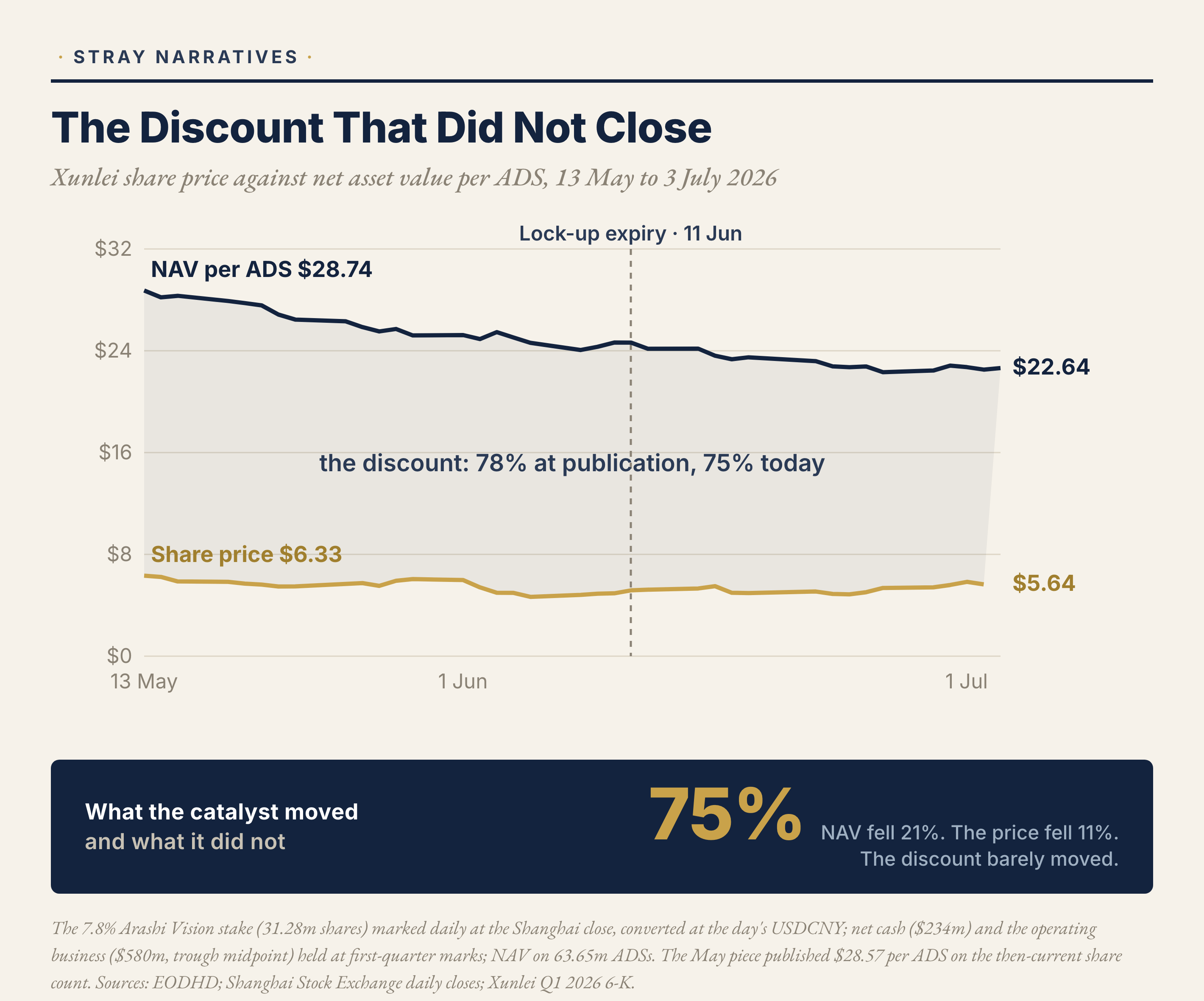

In May I published the case for Xunlei (NASDAQ: XNET) at $6.33: a 78% discount to net asset value, anchored by a 7.8% stake in Insta360, the Shanghai-listed camera maker, worth two and a half times Xunlei’s own market capitalisation, and by a hard date, the 11 June expiry of the lock-up on that stake. The title promised four weeks to close. The date has passed, the shares mark $5.64, the position is down 10.9%, and the discount has not closed [1][6]. The position stays on our list of trades, on humbler terms than the ones I published.

The discount itself behaved: 78% at publication, roughly 75% today. What fell was the net asset value. Insta360 has dropped 36% since the May mark, from 214 yuan to 135.93 [2], and Xunlei’s NAV per share has fallen by about a fifth [7]. The trade lost money the one way the piece spent least time pricing: the catalyst arrived and damaged its own collateral.

What happened

The 11 June expiry freed Xunlei to sell, and it freed everyone else: 56.5% of Insta360’s share register became tradable that day, roughly 37 billion yuan of stock across 28 pre-IPO investors, of which Xunlei’s holding is one line among many [3]. Insta360 was already de-rating from its September peak of 377.77 yuan, a price war with DJI gave the de-rating a fundamental engine through June [4], and the unlock supplied the paper. The stock set a 52-week low of 130.88 yuan on 29 June and closed at 135.93 on 3 July [2]. The May piece named 130 yuan as the level that changes the arithmetic. The mark sits two bad sessions above it.

Management, handed the moment the thesis required, chose patience. On the first-quarter call, two weeks before the unlock, there was no dividend, no timetable for the stake, and one load-bearing adverb: Xunlei would “gradually seek to adjust” its holdings toward a stated ceiling of investment securities at 45% of total assets, excluding cash and government securities [5]. No sale of Insta360 shares has been disclosed since the lock-up lifted. What has been disclosed is a repurchase: on 26 June the board approved a programme to buy back up to $20m of Xunlei’s own shares over the twelve months from 1 July, funded from the cash balance [8].

What I got wrong

The timing failed on its own stated deadline. The body of the piece described an 18-to-24-month monetisation window, but the title said four weeks, and the calendar was wrong: the discount-narrowing flow I expected into the date never appeared, and the shares closed as low as $4.66 before the unlock even arrived [6]. (The title, in hindsight, was the most falsifiable sentence in the piece.)

I priced what the unlock permitted our company to do, and missed what it permitted the other 27 unlocked holders to do. The event that made Xunlei’s exit possible cut the value of the thing being exited by a third, a scenario the published piece did not carry.

The catalyst rested on willingness. The Investment Company Act gives this management a direction and no timetable. The lesson filed in our mistake log: a catalyst date earns the name only when someone is obliged to act on it.

The published return arithmetic inherited the flaw. A base case of 55% to 75% a year was that willingness with a spreadsheet attached; the scenario that assumed the least of management, the bear case, is the one the market delivered.

The position, remarked

On the piece’s own methodology, at the 3 July close [7]: the Insta360 stake, 31.28m shares at 135.93 yuan and 6.77 to the dollar, is worth $628m, against $986m at publication. Net cash is roughly $234m, slightly higher than published. The operating business keeps its trough range of $410m to $745m, midpoint $580m: first-quarter revenue grew 54.1% and subscriptions 26.2%, though management guided to a modest slowdown ahead [5]. Net asset value is therefore about $1.44bn, or $22.65 per ADS, against $5.64 on the screen. The discount is 75%.

Two published facts survive the markdown. Net cash plus the trough value of the operating business comes to about $814m, 2.3 times the $359m market capitalisation, so the camera stake still comes free even marked a third below where I first called it free. And the regulatory pressure has not moved: at current marks investment securities sit near 74% of the relevant asset base against management’s stated 45% ceiling, and the sale required to reach that ceiling is roughly $446m, one and a quarter times the market value of the entire company [5][7].

Where I stand

The trade I published is dead, and pretending the horizon was always longer would be worse than the loss. What remains is a different position: a deep-discount holding with no clock, worth keeping only while that arithmetic holds, and re-examined in public whenever it is tested.

The case for closing is real: book NAV fell 25% in the two quarters to March, Insta360 is fighting a price war at its 52-week low, management’s pace is glacial, and wide discounts persist for years when nothing forces them shut. The case for holding is that at $5.64 the market pays less than the cash and the subscription business alone, the supply event has now happened rather than loomed, Insta360 sits at the May piece’s own bear-case mark, and the Investment Company Act still points in one direction. Selling at the bear-case mark would mean selling the cash and the subscription business below their own worth to be rid of a stake the price already writes off. The honest cost of staying is that the unlock supply has not cleared; it is now permanent.

I am holding, on those re-underwritten terms, with one mechanical exit: a next capital-allocation move of size that is an acquisition rather than a sale or a distribution. A decisive break below 130 yuan on Insta360 is a tripwire of a different kind. It sends the position back to the workbench for a fresh re-underwrite, published here, rather than forcing a sale on its own; a lower mark changes the arithmetic, and it is the arithmetic that decides. The first disclosed sale of Insta360 shares is what upgrades this from a discount we hope closes to one being closed. The watch items posted under the article in June stand, and the first has partially fired: the $20m repurchase is a real, if modest, step toward returning capital, while the pace of the 45% unwind and the next mark on the stake remain open.

References

[1] Stray Narratives Issue 11, An 80% Discount to NAV, Four Weeks to Close, published 14 May 2026 (straynarratives.com/p/an-80-discount-to-nav-four-weeks). Entry $6.33; NAV $28.57 per ADS on 62.86m ADS; net cash $230m; Insta360 stake $986m at the published 13 May mark of 214 yuan; operating business $410m to $745m at trough multiples, midpoint $580m.

[2] Arashi Vision Inc. (Insta360, SHA: 688775) closed at 135.93 yuan on 3 July 2026; 52-week low 130.88 yuan set 29 June 2026; 52-week high 377.77 yuan (September 2025). Stock Analysis and FT market data. Issue 11 published mark: 214 yuan, 13 May 2026, the basis on which the published $986m stake value was computed; the official 13 May close was 220.44 yuan.

[3] Pandaily, Insta360 at a Crossroads: 37 Billion Yuan Lock-Up Expiry Collides with DJI Rivalry, June 2026. 56.5% of shares, worth approximately 37 billion yuan, tradable from 11 June 2026; 28 pre-IPO financial investors; Xunlei at 7.84%.

[4] Caixin Global, DJI, Insta360 Lock Horns in Camera Pricing Standoff, 4 June 2026.

[5] Xunlei Limited, Unaudited Financial Results for the First Quarter Ended March 31, 2026, Form 6-K Exhibit 99.1, filed 28 May 2026, and the accompanying earnings call. Revenue +54.1% year on year to $98.6m; subscriptions +26.2%; cash, equivalents and short-term investments $303.6m; long-term investments $888.6m; total assets $1,415m. Management commentary on holding investment securities below 45% of total assets, excluding cash and government securities, and on adjusting holdings “gradually”; US Investment Company Act of 1940, s3(a)(1)(C), sets the statutory 40% test.

[6] XNET.US daily closes, EODHD: $6.33 on 13 May 2026 (entry); low close $4.66 on 5 June; $5.64 on 2 July 2026, the last session before the US holiday. Move from entry: minus 10.9%.

[7] Refreshed NAV on the Issue 11 methodology: 31.28m Arashi Vision shares × 135.93 yuan ÷ 6.7702 USDCNY = $628m. Net cash $234m ($303.6m cash, equivalents and short-term investments less $69.6m of bank borrowings, Q1 2026 balance sheet). Operating business at the published trough midpoint, $580m. NAV $1,442m ÷ 63.65m ADSs = $22.65 per ADS; market capitalisation $359m at $5.64 on 63.65m ADSs (318,268,921 shares outstanding at 31 March 2026; one ADS is five shares). Investment-securities ratio: $628m ÷ ($1,154m remarked total assets, the Q1 total of $1,415m with the $888.6m long-term investments line remarked to $628m, less $304m cash items) ≈ 74%; sale required to reach the 45% ceiling ≈ $446m.

[8] Xunlei Limited, 2026 Share Repurchase Program, Form 6-K filed 26 June 2026: up to US$20m of ADSs or common shares over the twelve months from 1 July 2026, funded from the cash balance.