The One Price

Stray Narratives, Issue 21 - Our foundational essay, and the first of a series: what happens when the market pays a software premium for a utility bill?

If you want to understand how Stray Narratives reads the world, start here - this is the foundational piece for everything else we will publish in the coming weeks.

The most important question for the next five years for your portfolio has absolutely nothing to do with whether artificial intelligence is “real.”

AI is real. So were the railroads, the telegraph, and the fibre-optic cable. Each of them was still real on the morning after its bubble burst.

The question that will actually dictate the next decade of returns is much drier: What holds the American economy up when the spending on AI slows down? And the slightly more awkward follow-up: Does anything?

The United States is sitting in the final stage of a forty-year disinflationary bull market. The technology currently credited with extending that bull market is being dangerously misread. AI is not a new paradigm. It is a late-cycle efficiency input arriving at the maturity phase of a long technology cycle, not the dawn of a fresh one.

Sameer Singh’s reference class is exactly right: AI is the new microprocessor.

Here is the problem with microprocessors. An efficiency input makes the entire economy more productive, while its own profit margins are ruthlessly beaten to death in a commodity price war. The economic surplus flows downstream to the users, not to the companies supplying the hardware.

The rent does not disappear so much as relocate. It gathers at the one or two chokepoints no one can design around, the instruction set and the single foundry that can etch it, and drains away from the vast, undifferentiated capacity the hyperscalers are buying and renting back out.

A two-sided platform (like an App Store or a search engine) does the exact opposite. It traps users, extracts rent, and keeps its pricing power for a generation.

Right now, the market is paying the platform’s price for the microprocessor’s economics.

Stray Narratives has so far published individual investment ideas and a few intellectual articles on how we are understanding AI. This piece opens a series that steps back to the picture they sit inside: where the market stands in its long cycle, what this AI boom actually is, how it rhymes with the booms before it and where it turns worse, what lies underneath it, and what to do about it. The pieces that follow take it up one question at a time.

The 200-Year Loop

Every infrastructure build-out in the history of capitalism runs the exact same loop. Capital violently crowds into the “new thing.” The few companies who can afford the scale overbuild it. The financing strains. The bubble bursts, leaving a pile of stranded assets when the assumed cash flows mysteriously fail to appear.

Canals, railroads, rural electrification, fibre optics, and shale oil each completed this exact, predictable circuit.

To be a structural bull today, you have to make a spectacular assumption. You have to look at two hundred years of financial history and say with a straight face: “Yes, but this time the guys burning the cash are really smart.” You must believe that this AI build-out will be the very first to magically escape the loop, and that the firms currently spending the money are acting rationally against revenues that literally none of them can forecast.

Hyperscaler capital expenditure is now running above 2% of GDP. This is among the largest peacetime build-outs on record. But this specific cycle is uniquely dangerous in three ways:

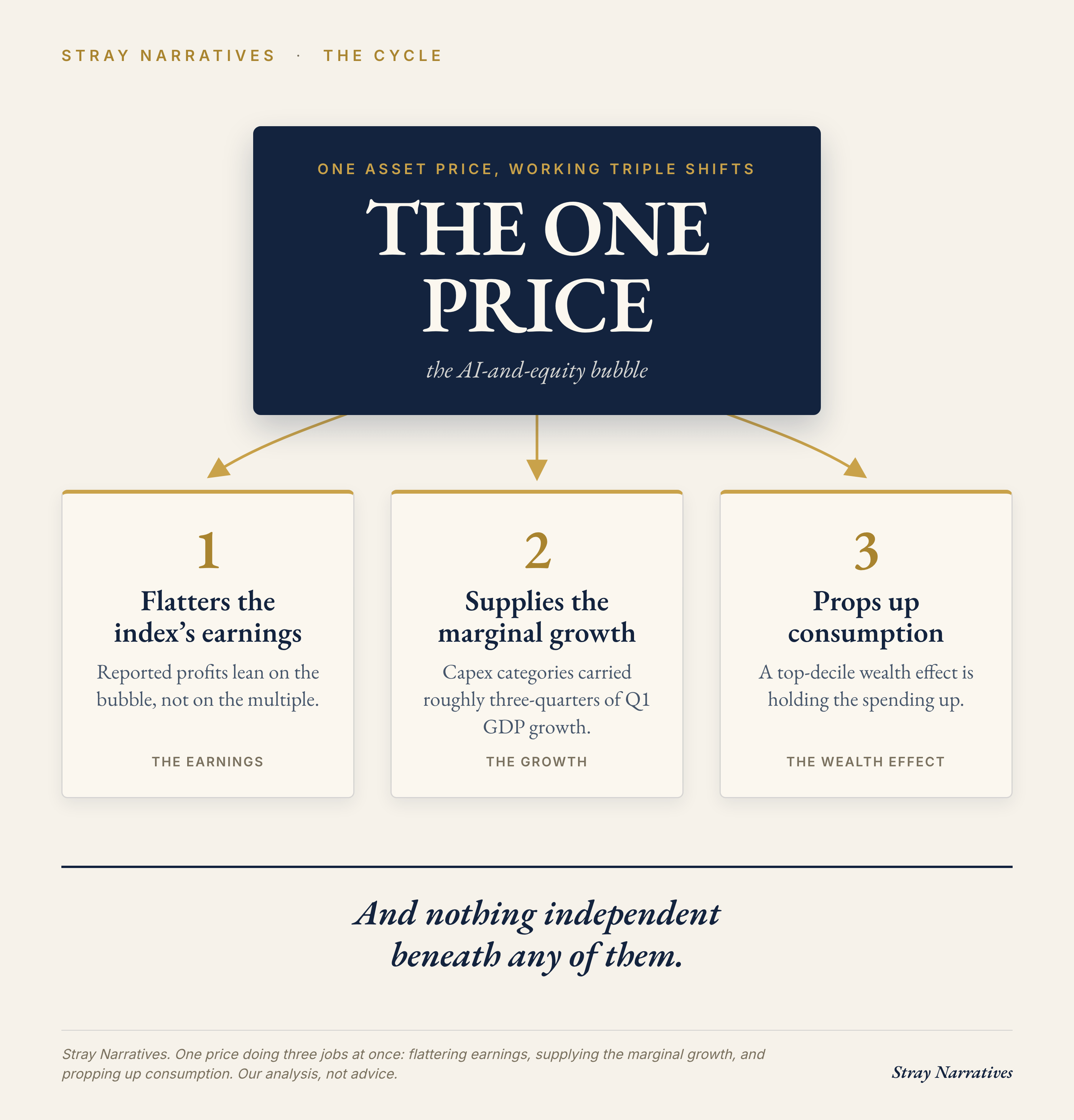

The Illusion of Earnings: Silicon Valley has leaned ever harder on the ancient, magical art of depreciation accounting. The excess is hiding in reported earnings rather than the multiple, as hyperscalers mysteriously decide their hardware will last much longer than anyone thought. Meanwhile the revenue, though real, still covers only a fraction of the cumulative bill, which the BIS now puts above a trillion dollars across 2025 and 2026, and is increasingly financed with debt, and free cash flow is evaporating: at Amazon alone from a filed $26 billion to barely $1 billion in a single year. It is a spectacular business model if you don’t like money.

The Duration Mismatch: We are currently funding thirty-year data-centre debt to produce a deflationary token whose cost, for any given level of capability, drops 70% to 90% a year. The entire structure is running on chips with the effective lifespan of a flagship phone (18 to 36 months). And just to keep things interesting, a state-backed Chinese competitor is actively trying to drive the marginal cost of that token to absolute zero.

The Stranded Asset Trap: When the railroad bubble burst, it politely left behind tracks that built the modern economy. When this bubble bursts, the buildings and the power lines will find new owners at a fraction of their financed cost, while the returns that were meant to justify them simply never appear, and the loss lands where the money did, on repriced debt syndicated through the insurers and pension funds of middle America.

The Economy Beneath the Bubble

The American economy that will eventually have to absorb this bust is, to put it politely, exhausted.

Once you strip out the AI capital spending, the foundation looks incredibly weak. Capex categories supplied roughly three-quarters of Q1 GDP growth. Beneath that capex sits a frozen labour market, housing rolling over, and a personal savings rate slashed to 3%, nearing its pre-crisis lows.

Consumption is holding up in large part because the equity bubble itself is sustaining a wealth effect for the top decile of earners.

One asset price is currently working triple shifts: it is flattering the index’s earnings, supplying the marginal GDP growth, and propping up the consumption beneath both. Aswath Damodaran’s caution about pricing versus value applies to this entire house of cards, not merely the semiconductor leaders.

The Asymmetry

This is the asymmetry of the current market, and it is the reason we are laying this groundwork now rather than writing a witty autopsy later.

The market looks undeniably safe right now precisely because the thing inflating it is so fragile. The wealth effect, the earnings, and the growth all rest on a single price, with nothing independent beneath any of them. John Templeton famously noted that bull markets die on euphoria. That euphoria is always strongest at the point of maximum dependence on one single input.

We are positioning our capital for that specific shape, rather than trying to guess the exact timing. Because if the history of these cycles teaches us one thing, it is that the timing of a break is the one secret the market flatly refuses to tell you in advance.

Next in the series: before you can say what this cycle will do, you have to know where you are standing in it. The next piece takes two hundred years to answer.