The Patient Is Not Dying

Stray Narratives, Issue 18 - The medical-device makers are the cheapest they have been in a generation, and the market has the diagnosis backwards.

Stray Narratives is published when the market demands a closer look. Nothing in this publication constitutes investment advice. All views are those of the author. Please read our full disclaimer.

If you prefer to listen rather than read, here is a podcast interview version of this same subject:

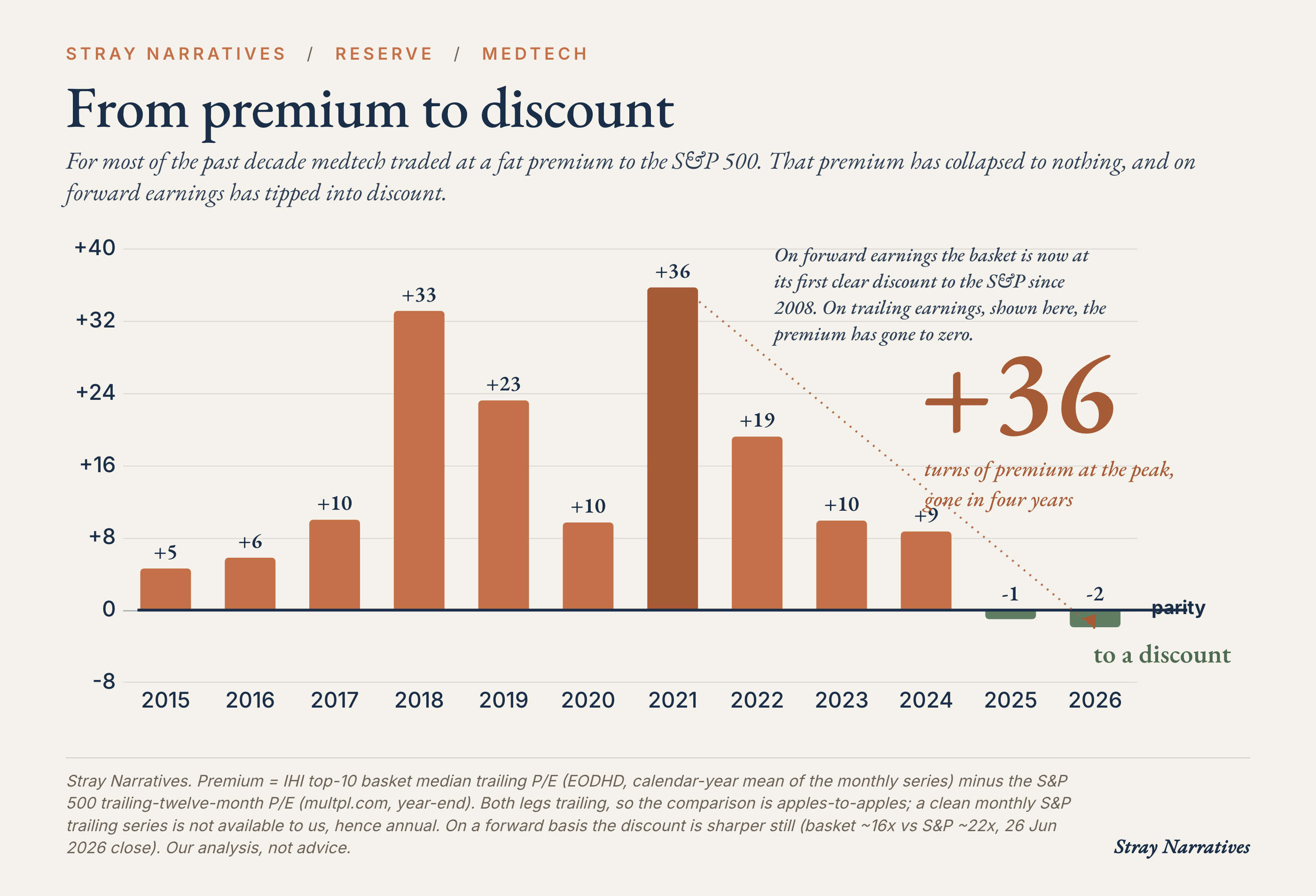

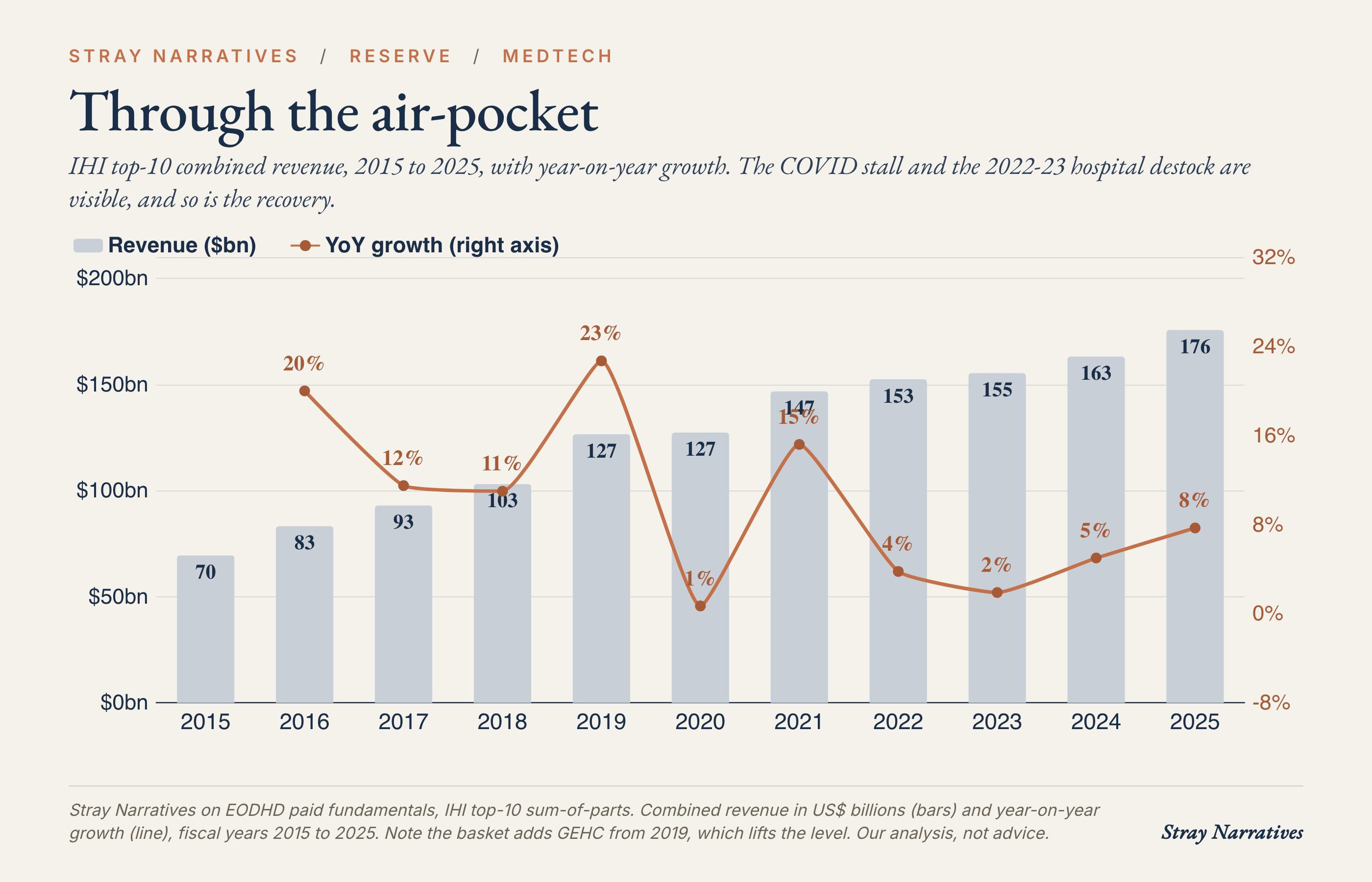

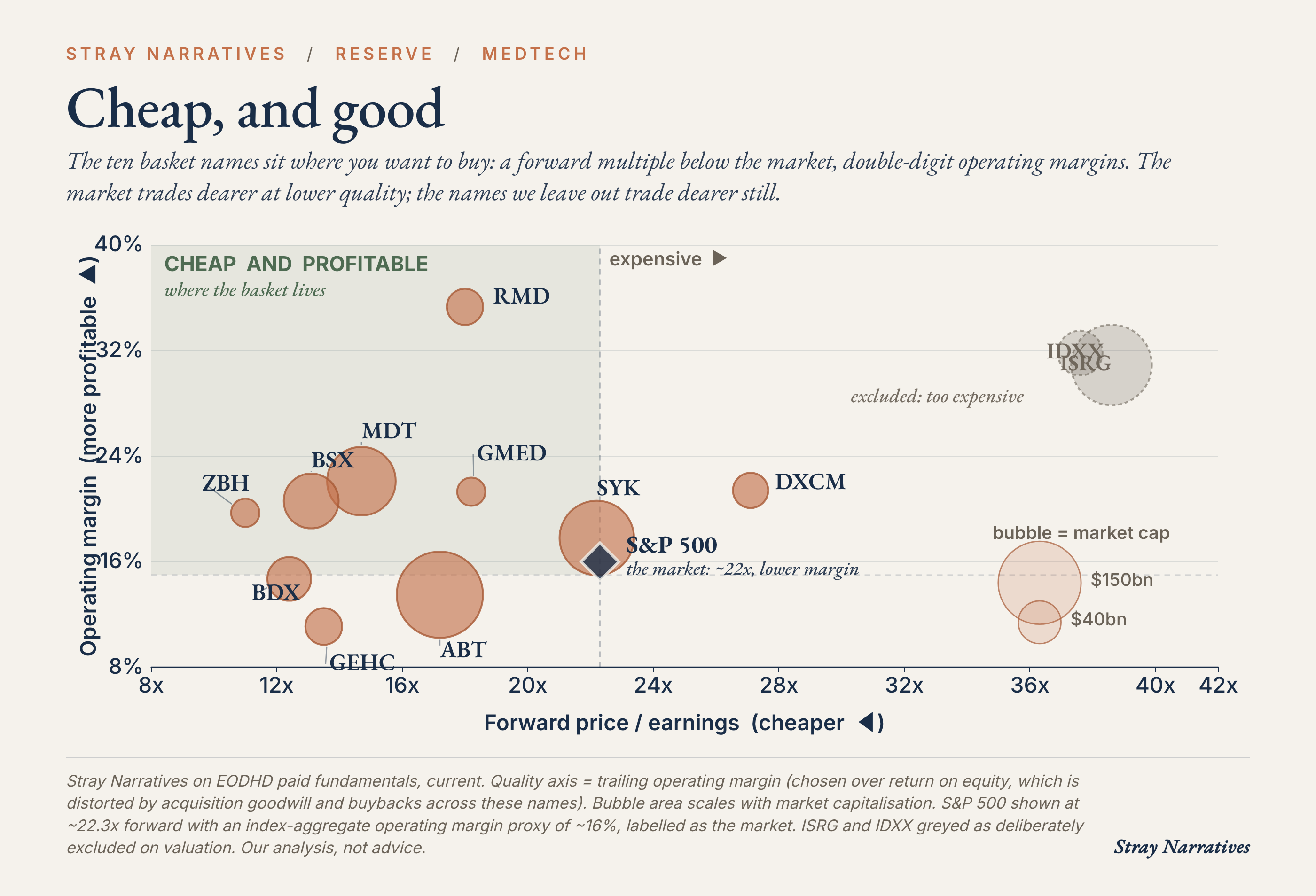

The American medical-device sector trades at its smallest premium to the wider market since the 2008 financial crisis, and on next year’s earnings it has slipped to an outright discount for the first time in living memory [1]. This is a group of companies that grew revenue from roughly seventy billion dollars to a hundred and seventy-six billion over the past decade, earns operating margins near twenty percent, and sells into the most dependable demand curve in the economy, which is the ageing of the rich world [8]. We are adding a basket of its cheapest quality names, equal-weighted, to the list of trades, because the market has priced a collapse that the businesses themselves refuse to deliver.

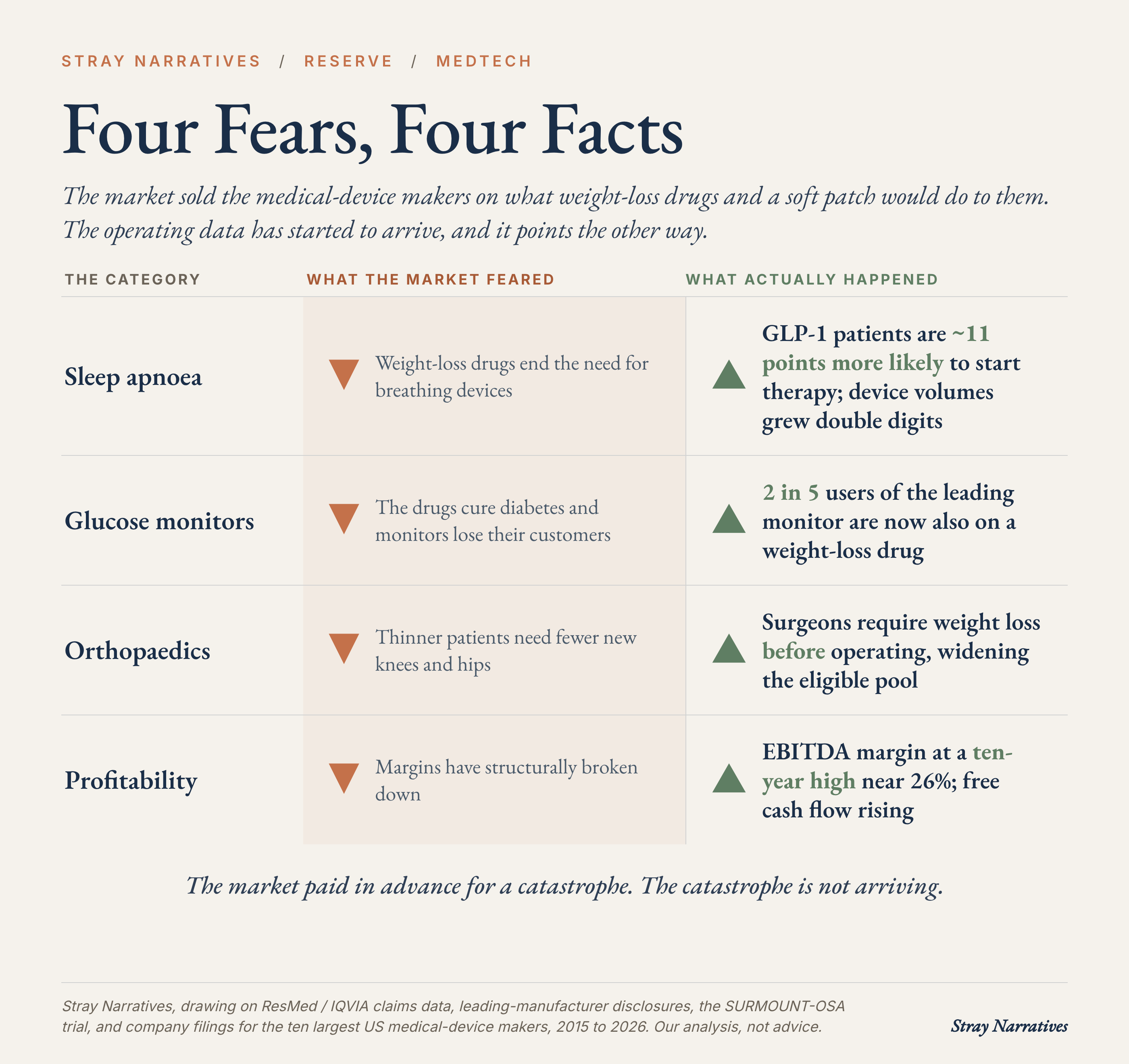

Two fears did the damage. The first is that weight-loss drugs will hollow out demand for everything from artificial knees to heart valves to glucose monitors. The second is that the sector’s profitability has quietly broken. Both are checkable against the operating numbers, and the numbers disagree with the price: the drugs are expanding several of these markets rather than shrinking them, and the margin dip everyone extrapolated was a post-pandemic inventory hangover that has already reversed.

How a good business got cheap

The de-rating is real and worth respecting. Large-cap medical devices spent most of the past decade carrying a four-to-six turn premium to the S&P 500 on forward earnings, the going rate for steady growth and recession resistance. That premium has compressed to roughly nothing, and the median name now trades near fifteen times forward earnings against an index above twenty-two [1]. The last time the sector was this cheap relative to the market, the world was busy recapitalising its banks.

Two things drove it. Through the pandemic, hospitals over-ordered devices and consumables, then spent 2022 and 2023 working that inventory back down, so reported revenue growth stalled to under two percent before recovering [2]. And from 2023 onward, every earnings call carried the same question, in one form or another: what does Ozempic do to your volumes. The market has spent two years concluding that weight-loss drugs will empty the operating theatres, and has priced the sector accordingly, which would be the correct response if the operating theatres were emptying.

The engine did not break

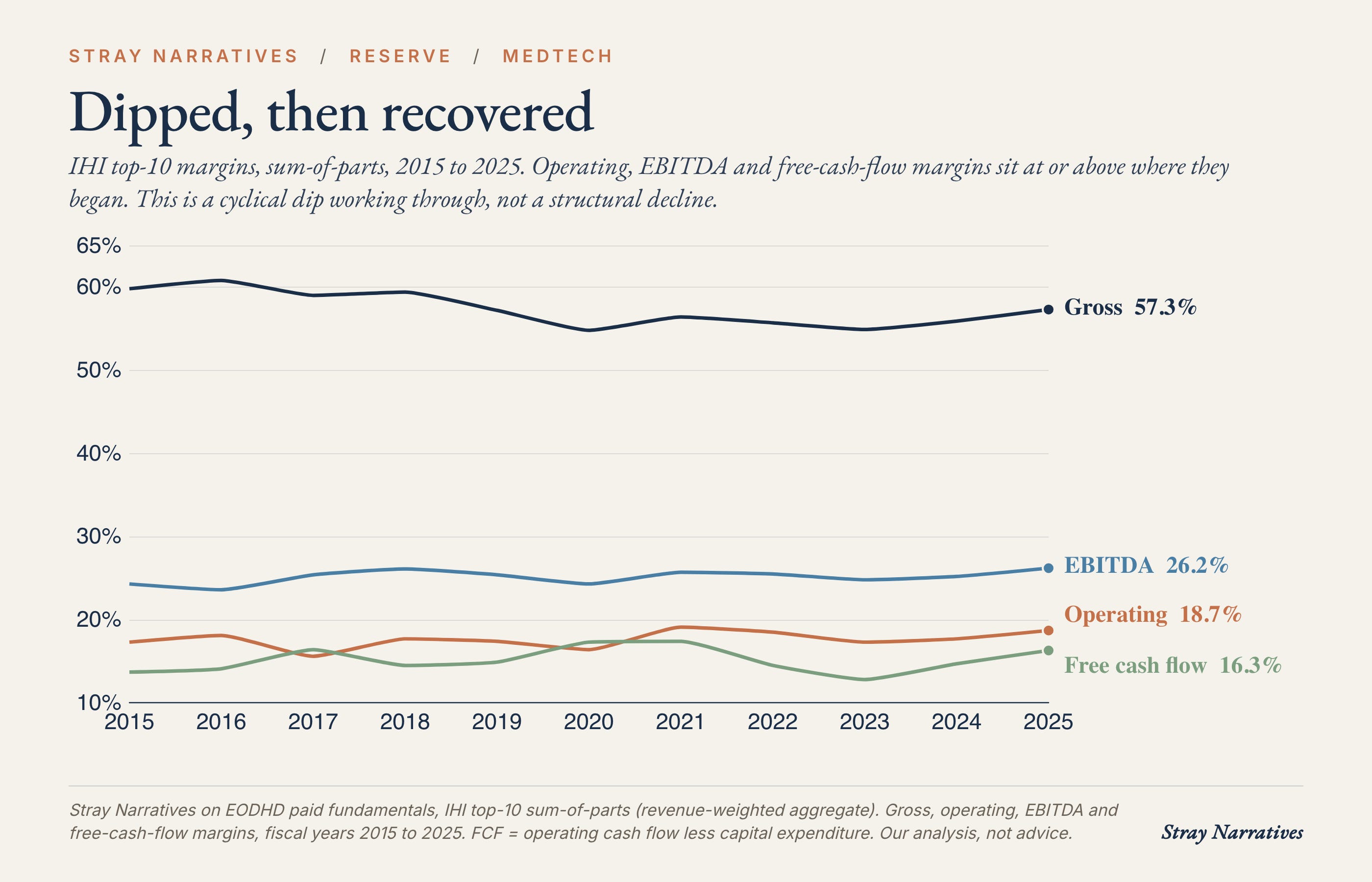

Cheap is only interesting if the business behind it is sound, and the ten-year record says it is. Set the pandemic distortions aside and the profitability picture is a cyclical dip that has already recovered: operating and free-cash-flow margins now sit at or above where they were a decade ago, EBITDA margins are at a ten-year high near twenty-six percent, cash conversion has improved, and research spending has held steady at about seven and a half percent of revenue the entire time [2]. The one genuine soft spot is gross margin, which has slipped two to three points over the decade on mix and input costs, an erosion the sector has more than recovered further down the income statement. A business that keeps investing the same share of revenue in its own future while its cash margins climb has not weakened. It has stopped commanding the market’s attention.

What the weight-loss trade got wrong

The GLP-1 fear deserves a real answer rather than a wave of the hand, because the logic is not absurd. Thinner, healthier people should, in time, need fewer of the interventions that obesity drives. The difficulty for the bears is that the operating data has begun to arrive, and for most of the sector it points the other way.

Sleep apnoea is the purest expression of the bear case, and its leading device-maker was punished hardest. The company ran its own analysis across roughly six hundred and sixty thousand patients and found that those prescribed a weight-loss drug were about eleven percentage points more likely to begin therapy, and its device volumes grew double digits straight through the scare [3]. The clinical trial that was supposed to prove the drugs cure apnoea instead found that most patients still had disease serious enough to treat [4]. The drugs are pulling people into the system, getting them diagnosed, and leaving the majority still needing the device.

The pattern repeats across the basket. Continuous glucose monitors were meant to lose their diabetic customers; instead more than two in five users of the leading monitor are now also taking a weight-loss drug and using the sensor to manage the transition [3]. Orthopaedics was meant to lose its knee and hip replacements; in practice surgeons routinely require patients to lose weight before they will operate, so a drug that reliably reduces body mass widens the pool of people eligible for surgery.

There is one place the bears are right. Bariatric surgery, the operations designed specifically to treat obesity, faces a genuine and management-acknowledged decline as the drugs substitute for the scalpel. For the diversified surgical-robotics franchise in our basket that is a small and recoverable share of a far larger procedure base, but it is the one unambiguous loss in the group, and pretending otherwise would be the sort of analysis that gets quoted back to you in eighteen months.

The asset nobody is pricing

There is a longer-dated reason to own these companies that the multiple ignores completely. The device-makers have spent two decades accumulating the one thing the artificial-intelligence boom has made suddenly precious: vast, proprietary, regulated clinical datasets that cannot be scraped from the open web or generated synthetically. The surgical-robotics leader holds the logged record of more than twenty million procedures. The connected-breathing-device maker has billions of nights of physiological data with the contractual right to use it. The diabetes and diagnostics franchises hold continuous, outcome-linked readings at a scale no model-builder can assemble, because a regulator will not accept invented data and a hospital cannot hand its patients’ records to a chatbot. Several of these firms already sell medical AI products the regulator has cleared, built on exactly this data [5]. A market paying extraordinary multiples for the companies that own AI models is paying nothing for the companies that own the one input those models cannot manufacture. We treat this as the free option on top of the value rather than the reason to buy.

The moat has one genuine challenger, and it is not a model-builder. Chinese device-makers are taking share in the high-volume, lower-margin corner of the industry, and they compete on price rather than on data. State procurement has cut the price of routine in-vitro diagnostic tests by as much as three-quarters, and China’s domestic champion in patient monitoring and bench diagnostics is moving upstream into the reagents and instruments Western firms long treated as captive; in gene sequencing a Chinese pair has already overtaken the former Western leader inside China [6]. The pressure falls hardest on the commodity-diagnostics and imaging lines, where the product is a consumable sold to a price-driven state buyer, and lightest on the franchises whose advantage is a regulated, outcome-linked dataset locked inside an installed base: a robotic-surgery record, years of physiological monitoring, a continuous glucose feed. The honest split is that the diagnostics and imaging names in the basket carry a structural margin headwind that quality does not fully offset, while the device-data franchises that anchor the thesis are the ones the substitution reaches last. It argues for leaning on the moat names inside the basket, not against owning it.

Why it re-rates

Cheap and sound can stay cheap for a long time, so the question is what closes the gap. The most concrete answer is that the buyers with the most information and the most capital are already taking these assets off the market outright. 2025 was the busiest year for medical-device dealmaking in more than a decade, including a private-equity take-private of a diagnostics company at roughly eighteen billion dollars and a twenty-one billion dollar acquisition by one of our own basket members [7]. When trade buyers and private equity pay cash for whole companies above where the public market marks them, they set a floor under the equity that sentiment struggles to break through. The slower catalyst is the ordinary one: as the inventory hangover fully laps and earnings revisions turn up, a sector at a discount to the market with a thirty-year demographic tailwind tends to be repriced by the same flows that left it. Those flows are only now beginning to reach devices: the group has turned up sharply off its June low in the past week, led by the diabetes and diagnostics names, though a few days off a six-month bottom is not yet a trend, and that hesitation is the honest timing risk in the trade.

The position

We are adding an equal-weighted basket of ten names to the list of trades at the open: ResMed, Medtronic, Abbott, GE HealthCare, Boston Scientific, Stryker, Zimmer Biomet, Becton Dickinson, Globus Medical and Dexcom. Six are quality compounders growing earnings and cash flow into the demographic tailwind; three are deep-value or special-situation names where the cheapness and a catalyst do the work; one, Dexcom, is the clearest single embodiment of the thesis, a proprietary-data franchise that the weight-loss drugs turn out to help. Equal-weighted, the basket trades near sixteen times forward earnings, well below both the market and the cap-weighted sector index, which is dragged up by paying thirty to forty times for the two most expensive names in the group. We hold the data moat through its cheaper carriers rather than overpay for the marquee one.

For readers who would rather own the theme in a single line, the iShares U.S. Medical Devices ETF (ticker IHI) delivers the same exposure, with the caveat that its cap weighting makes you pay up for exactly the expensive names the basket is built to avoid. The basket is the better expression of the view, the ETF the more convenient one. A two-line case for each holding sits at the foot of this note.

Stray Narratives is free and carries no advertising, so it travels only as far as its readers send it. If this was worth your time, a like, a restack, or a forward to one colleague who should see it is the whole of our distribution, and what keeps it free.

The position implication

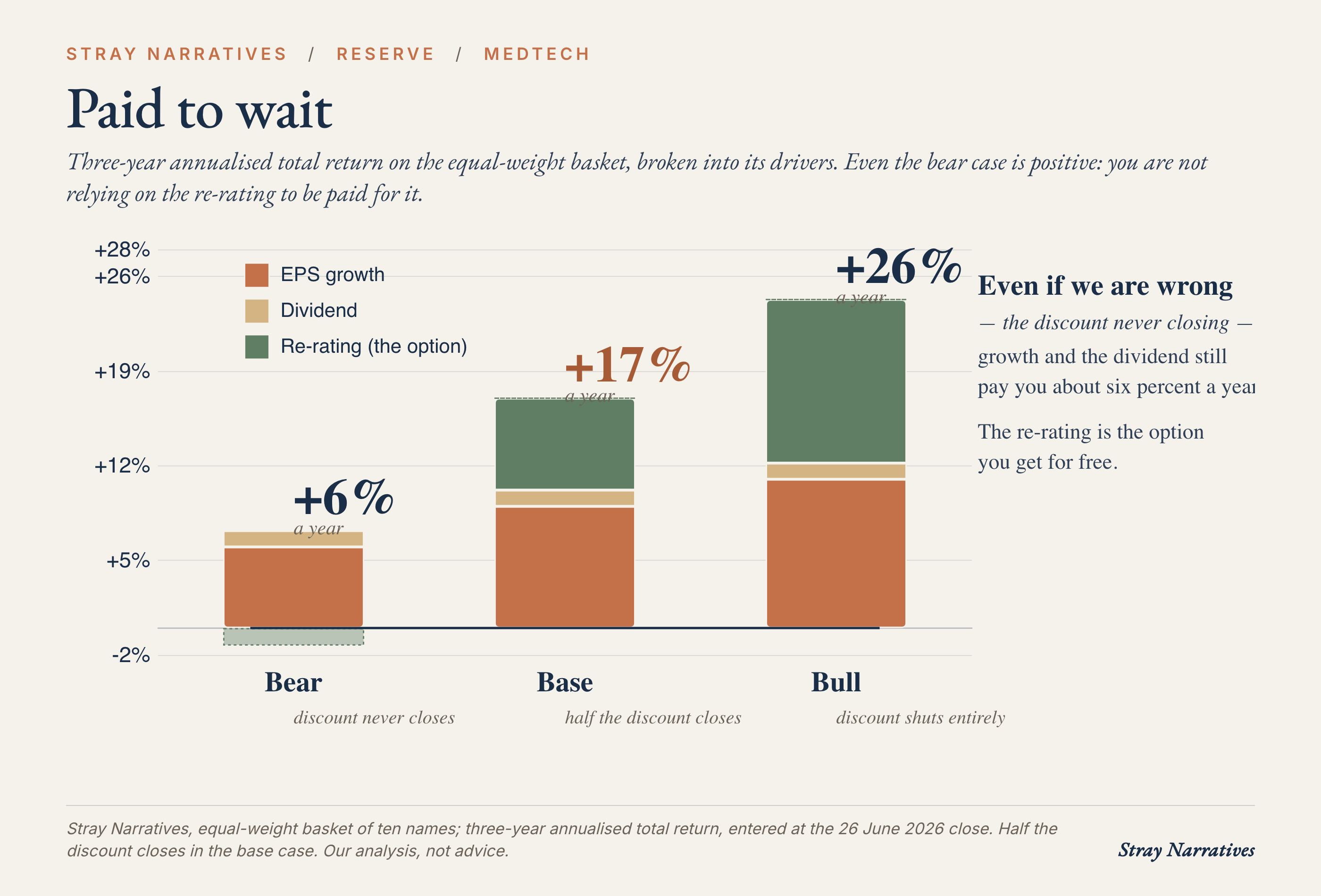

You are buying a sector at a discount to the market for the first time since 2008, with margins at decade highs, a demand curve that compounds for thirty years, acquirers setting a cash floor beneath it, and a proprietary-data moat the AI trade is pricing at zero. What that pays, on a three-year view and entered at the basket’s sixteen-times multiple, is a base case of roughly seventeen percent a year: about half the discount to the market closes, earnings compound near nine percent, and the dividend adds a point. If the discount shuts to parity and earnings run faster, the basket returns about twenty-six percent a year. If it never closes at all and earnings only grind, the basket still returns about six, because the growth and the yield carry it without the re-rating. The re-rating is the option you are handed for free.

That asymmetry is the reason to own it now: the discount exists because the market paid in advance for a catastrophe, and the catastrophe is being refuted in the operating numbers one quarter at a time. The repricing does not require the businesses to surprise anyone. It only requires the absence of the disaster that is already in the price.

References

[1] Forward and historical relative-valuation work on US large-cap medical devices (median next-twelve-month P/E versus the S&P 500 and the healthcare sector), from a sell-side equity research desk, May 2026; cross-checked against a major asset manager’s published note placing healthcare at its lowest relative valuation since 2008. Our own basket multiples are computed from company filings.

[2] Stray Narratives analysis of the ten largest US medical-device companies’ annual filings, 2015 to 2025 (revenue, gross/operating/EBITDA/free-cash-flow margins, research and development, return on equity), aggregated sum-of-parts.

[3] ResMed published analyses of GLP-1 prescription data and CPAP initiation/adherence (IQVIA claims dataset, ~660,000 patients), and company device-volume disclosures, 2025-2026; continuous-glucose-monitor co-prescription figures from the leading manufacturer’s disclosures.

[4] Eli Lilly SURMOUNT-OSA trial results and the FDA approval of tirzepatide for obstructive sleep apnoea, December 2024.

[5] FDA clearances of medical AI/machine-learning device software across the named manufacturers (FDA AI/ML-enabled device list, public).

[6] Chinese medtech competition and pricing: China’s centralised “volume-based procurement” of in-vitro diagnostics (provincial tender data via the National Healthcare Security Administration), the domestic patient-monitoring and IVD leader’s vertical-integration into reagents/raw materials, and the displacement of the incumbent gene-sequencing supplier inside China by a domestic pair (company filings and trade-press deal data; surfaced by a sell-side note, underlying primaries cited).

[7] Medical-device M&A activity, 2025: aggregate deal value and the take-private of a diagnostics company and a large strategic acquisition cited as illustrative (public deal announcements).

[8] US Census Bureau and UN Department of Economic and Social Affairs population projections (US 65+ population toward 71 million by 2030; global 65+ toward ~1.5 billion by 2050).

The basket, name by name

ResMed (RMD). The cleanest rebuttal to the GLP-1 bear: its own claims data shows patients on weight-loss drugs are more likely to start CPAP, not less, while device volumes still grew double digits. At 16x forward earnings with operating margins above 30 percent, the market is paying late-cycle prices for a structural grower.

Medtronic (MDT). The lowest-multiple way to own the data moat: several FDA-cleared AI products already run on its proprietary device data, and it converts roughly five billion dollars of free cash flow a year. At 13x forward earnings it is priced as a no-growth utility while revenue has returned to mid-single-digit growth.

Abbott (ABT). The diversified ballast, spanning glucose monitors, diagnostics and devices, with free cash flow up roughly half over three years to more than seven billion dollars. Its Libre franchise is a GLP-1 beneficiary, as drug users adopt monitoring rather than abandon it.

GE HealthCare (GEHC). The cheapest large-cap imaging franchise at 13x forward earnings, and the most prolific filer of FDA-cleared AI in the group. Growth is slow, so the case rests on the re-rating of a misjudged spin-off rather than on accelerating fundamentals.

Boston Scientific (BSX). The Farapulse cardiac-ablation cycle is still driving low-double-digit revenue growth and steady share gains, with free cash flow roughly doubled over three years. At around 13x forward earnings it is the cheapest of the growth names, partly because the stock has sold off sharply in recent weeks on a flagged stagnation in its Watchman left-atrial-appendage line, a setback in a different franchise from the Farapulse ablation business that underpins the growth case.

Stryker (SYK). Orthopaedic robotics with a genuine data moat: its Mako system has logged more than a million cases a rival cannot replicate, and weight-loss drugs help by clearing the BMI thresholds that gate joint replacement. The 21x multiple is the one premium we pay for quality and moat together.

Zimmer Biomet (ZBH). The deepest value at under 11x forward earnings, a mean-reversion bet on an orthopaedics recovery rather than a growth story. The same GLP-1 dynamic that worries the bears makes more patients eligible for the hips and knees Zimmer sells.

Becton Dickinson (BDX). The special situation: 11x forward earnings against a company pursuing a separation that could surface value the conglomerate structure hides. It also carries the most debt in the basket, so this is the position underwritten on the catalyst rather than the margins.

Globus Medical (GMED). The quality mid-cap: a net-cash balance sheet, a double-digit return on equity, and operating margins climbing back toward the high teens as the NuVasive merger integrates. Small enough to stay a credible acquisition target in a consolidating sector.

Dexcom (DXCM). The thesis in a single name: a proprietary glucose-data moat, a verified GLP-1 tailwind as drug users adopt monitoring, and free cash flow more than doubled to over a billion dollars. The 27x multiple is the basket’s richest, and the risk to watch is the price war with Abbott, not the drugs.