Anyone Care for Some Ice Cream?

Stray Narratives, Issue 09 - ad-hoc article on ice cream

Stray Narratives is published when the market demands a closer look. Nothing in this publication constitutes investment advice. All views are those of the author. Please read our full disclaimer.

The mandate event, already priced

The market voted before it counted the votes.

Magnum was distributed to Unilever’s shareholders the way unwanted assets always are: handed across and let go of, fast, by funds whose mandates did not allow an Amsterdam-listed ice cream stock to stay on the book. By 22 April, the share price had drawn 34% off its February high. The Amsterdam line sat as the eighteenth-most-shorted name in the STOXX 600 at 19% of free float (the share count actually available for trading), and the listing-day valuation already trailed a European broker’s pre-listing fair-value range by €2-3bn.[3][3a][3b][4] The supply was being priced before any operating evidence had a chance to land.

Then the operating evidence landed. The Q1 2026 trading update on 30 April printed organic growth of +4.5%, volume +2.9%, with Europe & ANZ at +4.3% volume on -0.3% price. That is unit pull, not promotional defence. FY2026 guidance was reaffirmed.[24] The price moved on the print, the cleanest leg of the near-term trade taken in a single session, much of it absorbed by short-cover.

The forced-seller overhang is no longer hypothetical. It has landed, it has been priced, and it has begun to unwind. That changes the question. The bull case is no longer a claim that the forced-seller compression will happen. It is a claim about what comes after the compression that has already been paid for.

Worth stating out loud: a Q1 trading update discloses revenue. It does not disclose margin. The bull case turns on margin. So the print confirms the volume thesis the bears were betting against, narrows the structural claim by exactly that much, and leaves the load-bearing question unresolved. The 1H 2026 release in late July is the first window in which the load-bearing question gets answered.

The category sits in pressure

Magnum is not a standalone case. The whole branded CPG aisle is under pressure. The US and UK middle-class consumer has traded down to discount and private-label brands at a pace the incumbent operators have finally been forced to admit on calls. The Wall Street Journal in November 2024 led on the fact: households earning over $100,000 are now the fastest-growing cohort at Aldi, Lidl, and the US dollar chains.[5] Six-figure households shopping at the discounter is not a recession story. It is a structural one. Private-label has moved from recessionary backstop to default preference, and has survived wage growth and improving sentiment without giving any of the share back.

The issuer side runs parallel. Kroger’s 10-K carries Our Brands sales above $32bn at 90%+ household penetration with 900 new items in the year, which is the language of a strategic asset, not a defensive line.[6] Kraft Heinz, P&G, Unilever, and Colgate have each said versions of the same thing on calls for the past two years: the price gap to private label has widened past the sustainable range.[7] Bronnenberg, Dubé and Sanders’ 2018 NBER work on scanner data, including ice cream as a tested category, found that consumer blind-test preference does not distinguish private-label from national brand.[8] That finding is a decade old. What has changed since is the arrival of retailer cohorts that have professionalised private-label packaging to a point where the informational gap has narrowed.

The ice-cream evidence is issuer-recorded, in the parent’s own voice on the parent’s own call. Hein Schumacher, then-CEO of Unilever, on the Q4 2023 results call, verbatim: “very disappointing year for Ice Cream with price elasticity in the in-home channel much more negative than that seen in other categories and with a strong consumer down-trading to private label.”[9] That is Magnum’s inherited book.

The investment case turns on a single question. Are Magnum’s specific moats (brand occasion, cabinet distribution, category archetype) the exception inside the pressure, or the next item on the list?

The near-term trade

Issue 01 mapped what we called the Kill Zone: when a product is easy to compare on price and quality, and cheap to switch between brands, one or two players end up taking nearly all the market.[23] An AI-powered shopping assistant that reads ingredient lists and price gaps at the shelf makes products more comparable by definition. Functional FMCG sits inside the zone. The middle-class downtrading documented above is not only cyclical; it is verifiability shifting under the brand premium.

Ice cream is not a uniformly functional category, which is the Magnum-specific hinge. The franchise outside the in-home tub (the supermarket multipack eaten at home) is emotional, seasonal, experiential, impulse-weighted. The purchase is not an optimisation problem the assistant resolves, because the consumer is not at the shelf with time to read. That is the structural defence the bull leans on. The bear reads the same fact pattern as a partial defence at best: the in-home tub channel is c. 60% of revenue, and that is where the 2023 trade-down (the moment branded ice cream lost shoppers to private label on price) landed.

The forced-seller arithmetic is where bull and bear briefly agree. About 60% of the float had to be sold inside six to twelve months. Natural buying capacity was around half of that.[4] Between 8 December and 22 April, the stock did what supply-and-demand demanded. The 34% drawdown, the 19%-of-float short register, and the multi-billion-euro discount to broker fair value are the same fact in three notations.

A 19% short position at the eighteenth-most-shorted seat in the STOXX 600 is a crowded trade. Crowded bear trades work until they do not, which is to say they work until you find yourself wedged in next to seventeen other people on the same side of the boat. That is what 30 April looked like in the post-print session.

The next forced flow is a buy. Once Unilever clears the first batch from its retained 19.85%, the share count freely available for trading rises enough to lift Magnum into full benchmark weighting on STOXX 600, MSCI Europe, and FTSE 350. The index funds tracking those benchmarks then have to buy. That mechanical buying is typically 1-3% of market cap inside a 1-3 day window, which on today’s level implies $80-240m of committed flow into a register that the short position has already squeezed.[4]

The base case from here is +5-15% over six to twelve months on residual overhang absorption, first-tranche disposal, index recalibration, and short-cover on any further upside catalyst. The range is -10% on disposal slippage plus a Q2 miss to +25% on a first-tranche announcement landing inside the inclusion window. Both bull and bear concede this leg.

The 12-month inflection

Past index inclusion, the consensus dissolves.

Two questions, defensible from the same fact base, define the bull and bear past 12 months.

The bull’s question. Do Fernando Fernandez at Unilever plc and Peter ter Kulve at Magnum execute the disclosed €500m productivity programme on the disclosed calendar, and does the resulting margin structure compound toward a 19-22% adjusted EBITDA band by FY2028-FY2030?

The bear’s question. Does category drift (cabinet atrophy, GLP-1 frequency compression, private-label compounding under verifiability pressure) reassert after the near-term mechanics unwind, and does the plc-form ceiling structurally cap the margin arithmetic below Froneri’s accessible range?

The remainder presents each at its strongest.

The longer-term bull

For ten years, the ice cream division ran an operating margin of 9.6-12.1%, capped by a matrix organisation that allocated marketing budget across detergents, deodorants, tea, and ice cream from the same group pot. Cabinet investment in Manila lost to deodorant media in Detroit, year after year, in board meetings the ice cream people did not always attend. That is not a management failure. It is what happens to ice cream inside a diversified FMCG conglomerate, and it is why ice cream never earned its category-native margin structure inside Unilever.

Magnum’s standalone machinery is now in place. Single-category board chaired by ter Kulve. Single-category P&L. The €500m productivity programme is disclosed in three tranches (supply-chain, overhead, technology), with €250m already delivered by end-2025, and the Q1 update reporting “good progress... on track for the full year”.[12][24] Half is in the bag before management has had a single contested earnings print to defend.

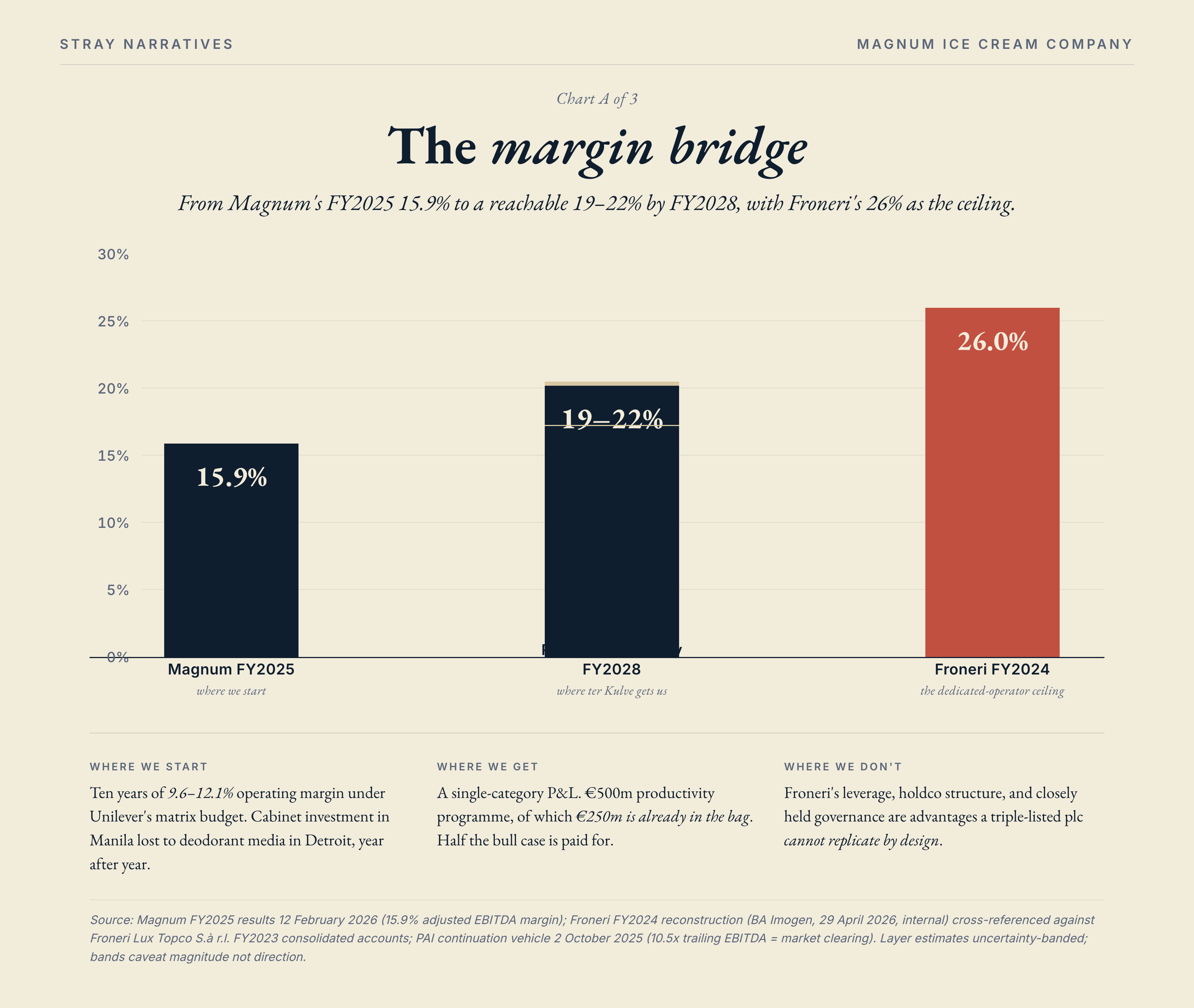

The reference point is Froneri, a privately-owned ice-cream maker (joint venture between Nestlé and the private-equity firm PAI Partners) operating in the same category with the same dairy, cocoa, and packaging cost base. Froneri runs at roughly 26% EBITDA margin on FY2024 revenue of €5.53bn.[13] On 2 October 2025, PAI completed a €3.6bn continuation vehicle at an enterprise value of approximately €15bn, 10.5x trailing EBITDA, with the operator-aligned capital electing to extend rather than exit nine years into the hold.[10][14] That is the market-clearing price for a dedicated ice-cream operator, paid by investors who have read the internal books.

The Froneri perimeter is now expanding. On 19 February 2026, Nestlé confirmed the phased sale of its remaining ice-cream operations (Canada, Chile, Peru, China, Malaysia, Thailand; ~CHF 1bn turnover; brands including KitKat ice cream) to Froneri.[25] The reference benchmark is consolidating in real time, on a calendar that overlaps Magnum’s first two earnings prints. That fact strengthens both sides of the argument: it confirms the destination the bull names andwidens the moat the bear says Magnum cannot replicate.

The margin bridge from Magnum’s FY2025 15.9% to Froneri’s 26% breaks into addressable layers and a structural residual.

Chart A — The margin bridge: Magnum FY2025 15.9% to a reachable 19-22% by FY2028, with Froneri's 26% as the ceiling.

The bands caveat the magnitude, not the direction. Roughly 400-700bp of the gap is addressable, 100-200bp is not, and Magnum has a three-to-five-year programme running at the addressable portion. At a 60% retention rate (high end of productivity-programme precedent, although ter Kulve already has €250m of the €500m in the bag), the reachable margin lands in the 19-22% band by FY2028-FY2030. Above company guidance, below Froneri by the plc-inaccessible residual, and above today’s entry multiple by enough to compound into terminal valuation. Half the bull case is paid for already. The other half is what the next two earnings prints test.

The cabinet network is the execution lever a dedicated operator with single-category decision rights actually has.[15]

Chart B — Cabinet economics: Magnum at €2,640 per cabinet vs Froneri at €3,950 per cabinet.

The bull case rests on two named executives. Fernandez sits at the plc parent, weighted toward the disposal calendar. Ter Kulve sits as the dedicated operator with a single-category P&L and a productivity programme on his desk of which half is already in the bag. The reader is asked to make a judgement on these two people, on the €500m disclosure, and on what the delivered €250m implies about the remainder.

The longer-term bear

On 27 August 2025, in a fireside chat, ter Kulve said in his own voice as the incoming CEO that the global cabinet fleet had been declining “approximately 2% a year” before the current reinvestment programme.[16] One sentence; the whole separation narrative, said unguarded. Three million cabinets contracting at sixty thousand a year for the Unilever decade is not an under-investment problem a productivity programme fixes. It is the physical signature of a channel quietly withdrawing floor while nobody at group level was looking.

Three mechanics compound the contraction. Consolidation in convenience retail (corner shops and petrol stations merging or closing) shrinks the number of locations willing to host a branded freezer. Migration of ice-cream sales into fast-food chains drops Magnum’s sticks into a case shared with Froneri and Häagen-Dazs. Grocery-aisle substitution of branded impulse sticks by own-label take-home tubs pulls the household occasion off the branded-cabinet page entirely. The conclusion is not a slower-growing fleet but a shrinking one in a channel whose three largest structural hosts are each quietly withdrawing floor.

The cabinet-specific capex disclosure, of which there was none across the Unilever decade, is the second thing worth saying. A parent that did not treat cabinet capex as a material disclosure theme for ten years is a parent that did not treat the cabinet as a strategic asset. Which is why the rebuild is not the release of an under-invested asset; it is a reconstruction project on something whose prior owner did not think was worth talking about.

The plc-form ceiling is the structural reason the drift reasserts. Three features make it a form-factor problem, not an operational one. Froneri’s pro forma leverage of 5.7x sits on the back of a June 2025 €3.9bn debt recap that funded a €4.4bn shareholder dividend.[18] Froneri’s incentive architecture is a single-purpose Luxembourg holdco with equity-linked management participation at operating-company level. Froneri’s governance is a closely held JV with two strategic owners and no quarterly disclosure to a free-float register. Each one of those is a structural advantage a triple-listed plc cannot replicate by design. The ceiling is the visible surface of an operating model a plc cannot copy.

The royalty-free Häagen-Dazs asymmetry is the second structural piece. Froneri operates Häagen-Dazs in the United States and Canada under a 99-year paid-in-full royalty-free licence running to 2110.[1][19] Häagen-Dazs holds over 38% of the US premium snacking segment at brand sales of roughly $1.4bn.[20] Froneri carries zero ongoing royalty cost on the single largest premium brand in the single largest premium ice-cream market. Every Magnum stick cabinet in North America competes at direct cabinet-level against a premium-brand operator whose brand cost on its largest US asset is effectively zero. The $641m Nestlé paid in December 2001 was the market-clearing price for perpetual access to the US premium-tier leader. Magnum does not have an equivalent asset, and no productivity programme can create one. The Froneri perimeter expansion announced 19 February 2026 widens the asymmetry, not narrowing it.[25]

GLP-1 (the Ozempic class of weight-loss drugs that suppress appetite) is the demand-side compounding layer. Adoption is tracking 2-3% of developed-market adult population by 2030 in the central scenario. Calorie reduction reported at 15-30% across all food categories. The bull frame bounds the category impact at 1-5% by FY2030 on calorific compression alone. The bear reading on the frequency axis is sharper. GLP-1 does not substitute the Magnum for something else. It eliminates the second and third Magnum from the weekly basket. One quarter of post-elasticity volume recovery does not settle that question; it narrows the mechanical claim and leaves the structural claim intact.

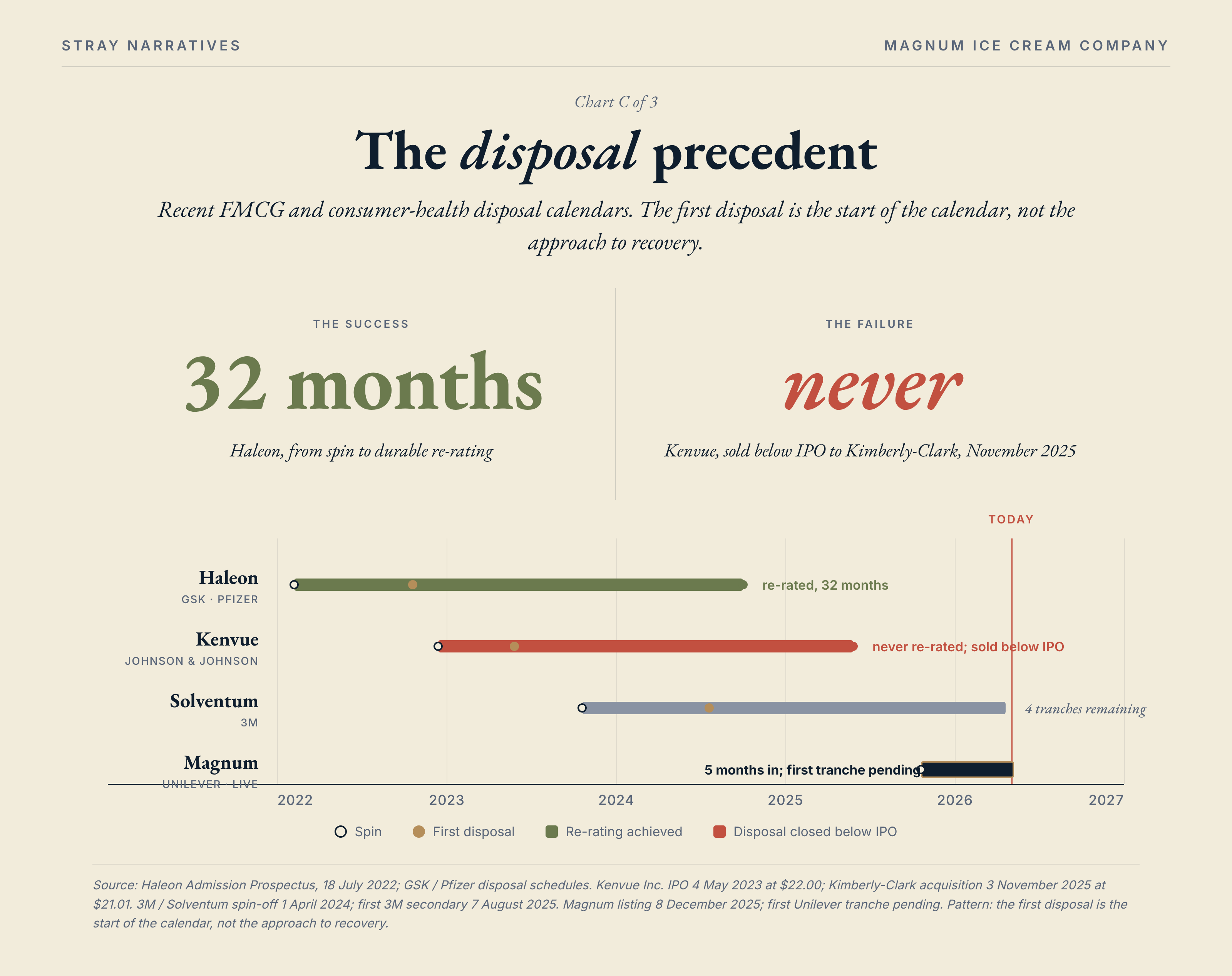

The disposal overhang is the five-year structural drag, not a twelve-month window.

Chart C — Disposal precedent timeline: Haleon, Kenvue, Solventum, Magnum.

The pattern is consistent. The first disposal is the start of the calendar, not the approach to recovery, which is why one operational beat is informative about the operating asset and silent on the disposal mechanics.[21][22]

The judgement

The market overpaid for the supply. The earnings will eventually price the asset. We now have one print’s worth of evidence that the volume thesis the bears were short on has narrowed.

The bear case kept the rest: cabinet contraction, plc-form ceiling, royalty-free Häagen-Dazs asymmetry, GLP-1 frequency compression past 2027. None of those is refuted by Q1. They are still on the page, and they remain the strongest possible test of the position.

I think the asset is attractive at this level. The forced-seller drag is mostly past. The dedicated operator has half the productivity programme banked. The reference comparable, Froneri, is widening its perimeter in real time. None of that requires the bear case to be wrong. It requires only that the operating evidence between now and FY2028 keep doing what the first print started to do.

I should have started buying earlier. Looking at the chart now, the eighteenth-most-shorted seat in the STOXX 600 was the trade, the 19%-of-float short register was the trade, and the broker-fair-value gap was the trade. The chance to take it without paying for the rerating-already-in-progress closed in a single April session, while I was still asking whether the operating evidence was reliable enough to lean on. The cleaner risk-reward window was the day before the print, not the day after.

I’m taking a position now anyway, on the bull case rather than the rebound. That ter Kulve delivers the €500m. That the cabinet network responds to single-category decision rights. That the index-inclusion mechanic provides the next forced flow upward. And that 18-24 months from here, the multiple gap to Froneri compresses by enough to compound past the entry-point premium I am paying for having waited.

None of that is settled by one quarter. None of that is what the position is taken on. The position is taken on the €250m delivered against the €500m promised, on the cabinet rebuild plus single-category decision rights, on the index-mechanic flow ahead, and on the 18-24 months in which the operating thesis either lands or it does not. The first 1H print, in late July, is the first window in which the position has to defend itself.

The expected return

Taking today’s level as the entry, and assuming margin lands in the lower half of the 19-22% band by FY2028 with Magnum trading at roughly 9x adjusted EBITDA (a measured discount to Froneri’s 10.5x continuation-vehicle clearing price), the base case implies an IRR of roughly 20-25% per annum over a 24-30 month horizon.

The bull case (margin reaching 22%, multiple recovering to 10x as Froneri’s perimeter expansion makes the comparable harder to discount) lifts that IRR to roughly 35-40%. The bear case (margin stalling at 17% and the multiple compressing to 8x on disposal slippage and a Q2 miss) compounds to about 8-12%. Positive, but no longer differentiated from a benchmark return.

The path is staged. The first six to twelve months carry +5-15% from forced-seller absorption plus the index-inclusion mechanic. The remainder is in the margin delivery between FY2026 and FY2028. Re-read points: the 1H 2026 print in late July, the FY2026 full-year results in February 2027, and the first index-inclusion announcement window.

I should add: I like ice cream. Summer is coming. If there was ever a time to own an ice cream stock, this is it.

Appendix: Häagen-Dazs reconciliation

The Häagen-Dazs trademark is owned globally by General Mills, Inc. (acquired via its 2001 purchase of The Pillsbury Company, which had owned the brand since 1983). General Mills licences the trademark royalty-free and exclusively to Nestlé and its authorised sublicensees for ice cream and other frozen-dessert products in the United States and Canada, under a 99-year paid-in-full licence established when Nestlé bought out General Mills’ 50% interest in Ice Cream Partners USA in December 2001 for $641m; the licence runs to 2110. In December 2019 (closed Q1 2020), Nestlé sold its US ice cream business, comprising Dreyer’s, Edy’s, Drumstick, Outshine, Skinny Cow and, importantly, its contractual Häagen-Dazs US and Canadian licence rights, to Froneri (the Nestlé / PAI Partners JV) for $4.0bn.[1][2] General Mills owns and operates Häagen-Dazs directly outside North America and Japan, manufacturing most of the rest-of-world volume at its Tilloy-lès-Mofflaines (Arras) plant in France. In Japan, Häagen-Dazs is produced and sold by Häagen-Dazs Japan, Inc., a joint venture majority-owned by Suntory (40%) and Takanashi Milk Products (10%) alongside General Mills (50%, inherited from Pillsbury, 1984). The Magnum Ice Cream Company holds no Häagen-Dazs rights in any territory; Häagen-Dazs is a direct premium-tier competitor.

References

[1] Nestlé USA, “Nestlé USA Acquires Fifty Percent Ownership Stake in Ice Cream Partners USA from General Mills,” press release, 26 December 2001 (99-year paid-in-full royalty-free Häagen-Dazs US and Canada licence; $641m consideration). Retrieved via nestle.com press-release archive.

[2] PAI Partners, “PAI Partners-backed Froneri announces acquisition of Nestlé’s US ice cream business for $4.0 billion,” press release, 11-12 December 2019. Retrieved via paipartners.com.

[3] The Magnum Ice Cream Company N.V., listing materials, 8 December 2025; €12.80 reference price; €7.8bn initial market capitalisation. Retrieved via Food Business News and Food Navigator listing coverage.

[3a] MICC NYSE and Euronext Amsterdam market data, close 22 April 2026, $13.07; 52-week range $13.06-$19.93; all-time high $19.87 recorded 11 February 2026. Retrieved via the Magnum Ice Cream Company N.V. investor relations page (themagnumicecreamcompany.com/investors) and the NYSE primary listing market-data page.

[3b] AFM Register of Net Short Positions (afm.nl), filings as of 17 April 2026, aggregate disclosed net short position equal to 19% of free float; STOXX 600 ranking via the primary European stock-loan data provider’s public weekly summary page.

[4] Stage A v2 and Stage B Demerger Precedent memo, BA Imogen, April-May 2026, internal. European broker pre-listing equity range €10.1-10.8bn (Irish Times, BNN Bloomberg, MarketScreener, ESM Magazine, 8 December 2025).

[5] The Wall Street Journal, “America’s Middle Class Embraces Discount Brands,” November 2024.

[6] The Kroger Co., Form 10-K, fiscal year ended 1 February 2025. Retrieved via SEC EDGAR.

[7] Kraft Heinz, Procter & Gamble, Unilever, Colgate-Palmolive FY2024 and Q1-Q3 FY2025 earnings transcripts.

[8] Bronnenberg, Dubé and Sanders, “Consumer Misinformation and the Brand Premium: A Private Label Blind Taste Test,” NBER Working Paper 25214, 2018.

[9] Unilever plc, Q4 2023 results transcript, 8 February 2024. Retrieved via unilever.com/files/transcript-unilever-q4-2023-results-8-february-2024.pdf.

[10] PAI Partners, continuation vehicle completion press release, 2 October 2025; €3.6bn equity transaction; ~€15bn EV; 10.5x FY2024 EBITDA.

[11] Unilever plc, FY2023 and FY2024 full-year statements; Unilever demerger circular, October 2025.

[12] The Magnum Ice Cream Company N.V., FY2025 full-year results, 12 February 2026; €7.91bn revenue; 15.9% adjusted EBITDA margin; €500m productivity programme disclosure; €250m delivered end-2025. Capital Markets Day 2025, 9 September 2025.

[13] Stage B Froneri Reconstruction, BA Imogen, 29 April 2026, internal. Underlying primary sources: Froneri Lux Topco S.à r.l. FY2023 consolidated accounts (Luxembourg RCS B241537); Nestlé FY2024 JV disclosure.

[14] Private Equity Wire, “PAI Partners secures €3.6bn for Froneri,” 3 October 2025.

[15] The Magnum Ice Cream Company N.V., prospectus, December 2025.

[16] Peter ter Kulve, CEO-designate, TMICC, Fireside Chat with Warren Ackerman (Barclays), 27 August 2025. Retrieved via Unilever IR posted transcript (unilever.com/files/tmicc-fireside-chat-video-transcript.pdf).

[18] Private Equity Insights, June-July 2025 coverage of Froneri €4.4bn shareholder payout and €3.9bn debt financing; Bloomberg, “Haagen-Dazs Maker Froneri to Raise €4 Billion Debt as PAI Seeks to Keep Stake,” 3 June 2025.

[19] General Mills, Inc., Form 10-K fiscal year ended 25 May 2025, Häagen-Dazs trademark disclosure. Retrieved via SEC EDGAR.

[20] Dairy Reporter, “Froneri’s success shows why Unilever is right to spin-off ice cream,” 27 October 2025.

[21] Haleon plc, Admission Prospectus, 18 July 2022; GSK and Pfizer disposal schedules.

[22] Kenvue Inc. and Johnson & Johnson disposal chain, IPO 4 May 2023 at $22.00; Kimberly-Clark acquisition 3 November 2025 at $21.01. 3M / Solventum spin-off 1 April 2024.

[23] Stray Narratives, “The Sorting Machine,” Issue 01, 4 March 2026.

[24] The Magnum Ice Cream Company N.V., “Q1 2026 Trading Update,” 30 April 2026. Retrieved via assets.unileversolutions.com/v1/147150923.pdf.

[25] Nestlé S.A., phased sale of remaining ice-cream operations to Froneri, 19 February 2026.

Research, not investment advice. Stray Narratives is the publishing arm of an investment-research operation; positions are disclosed alongside the analysis where they exist. Past performance does not guarantee future returns. Full disclaimer at straynarratives.substack.com.