Booking the War Premium

Stray Narratives, Issue 17 - Closing the "Wrong Map" tanker basket after the Hormuz deal

Stray Narratives is published when the market demands a closer look. Nothing in this publication constitutes investment advice. All views are those of the author. Please read our full disclaimer.

A crude tanker spends most of its working life earning a return that would embarrass a savings account. Then, for a few months every decade, a chokepoint makes the evening news, crude reroutes the long way round, and the holder books years of profits in a single quarter.

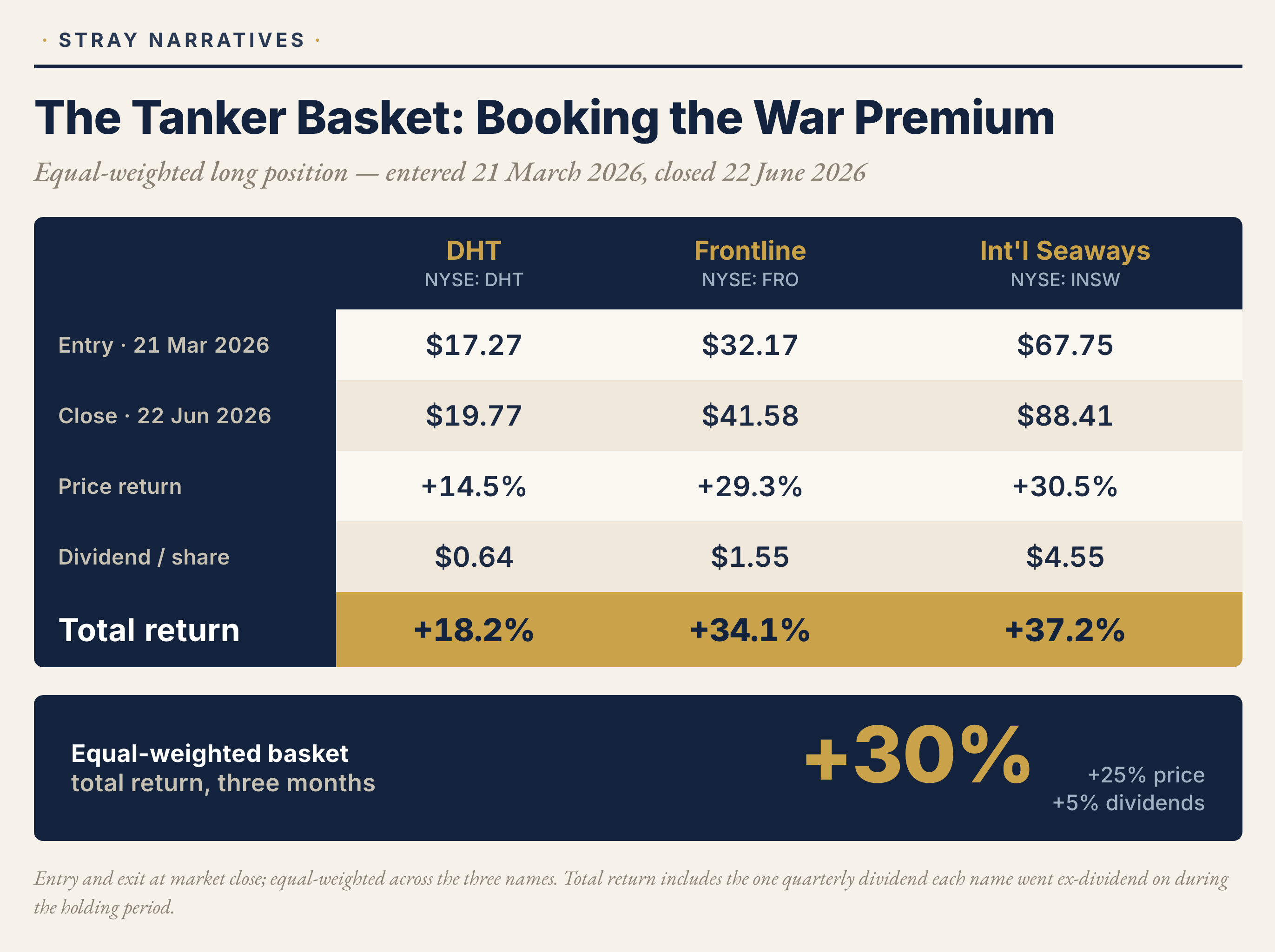

That window is the trade I put on in March. I called it the Wrong Map: a basket of three tanker equities, DHT Holdings, Frontline and International Seaways, equal-weighted, bought as a direct wager on Middle Eastern disruption. I closed it this week with a nice profit:

The reason to own these names was the disruption, and the disruption is resolving. The United States and Iran have signed a memorandum of understanding, the Strait of Hormuz is reopening, and a reopened strait is, with a lag, poor news for ton-miles: crude takes the direct route again, voyages shorten, idle capacity returns, and freight reverts toward breakeven. The war premium I was renting is being handed back.

The arithmetic

When conflict in the Gulf forces crude onto longer routes, ton-miles, the volume of oil multiplied by the distance it travels, rise, and tanker spot rates rise with them. At its early-March peak the Baltic benchmark for the Gulf-to-China route reached roughly $424,000 a day against an operating breakeven near $22,000, the spread that produces the best quarter of a shipping cycle and the record dividends that came with it. It had eased toward $100,000 by mid-June, and the congestion of the reopening keeps it bid for now, but the direction is no longer higher.

Why I am not holding out for the last dollar

Tanker equities have the awkward property of looking cheapest at the exact moment they are about to earn the least. They are priced off the prevailing spot rate, so at the crest of a disruption their trailing earnings look spectacular and the shares screen as the cheapest assets on the market, a multiple usually quoted without the word “trailing” attached. That multiple is a mirage built from a single, unrepeatable quarter, and when freight reverts the earnings behind it leave with the peace. I would rather hand the optically cheap multiple to whoever wants to own the normalisation than sell it to them a month later at a lower price.

There is a genuine floor under freight. Sanctioned Russian barrels, an expanding shadow fleet and structurally longer average hauls should keep ton-miles above the pre-war normal even after the queue clears, which is why the exit may be too early. But a floor a few thousand dollars above breakeven is a rounding error against a rate that spiked to nearly twenty times breakeven. It argues for owning these names at a normalised rate on a quiet day, not for riding them through the risk of a round trip.

Where I stand

I have now closed the Wrong Map tanker basket and all three legs finished in the black, including DHT, which spent most of the trade as the laggard before the reopening congestion firmed rates into June and pulled it level with the others. The other leg of the Wrong Map, the position in rates, runs on a different mechanism and a much longer clock, and it stays on; I will however restructure that trade in the coming weeks to make sure it embeds enough time horizon to materialise.

Really appreciate your perspective. I've subscribed and look forward to reading more!