The Channel Controllers

Stray Narratives, Issue 04

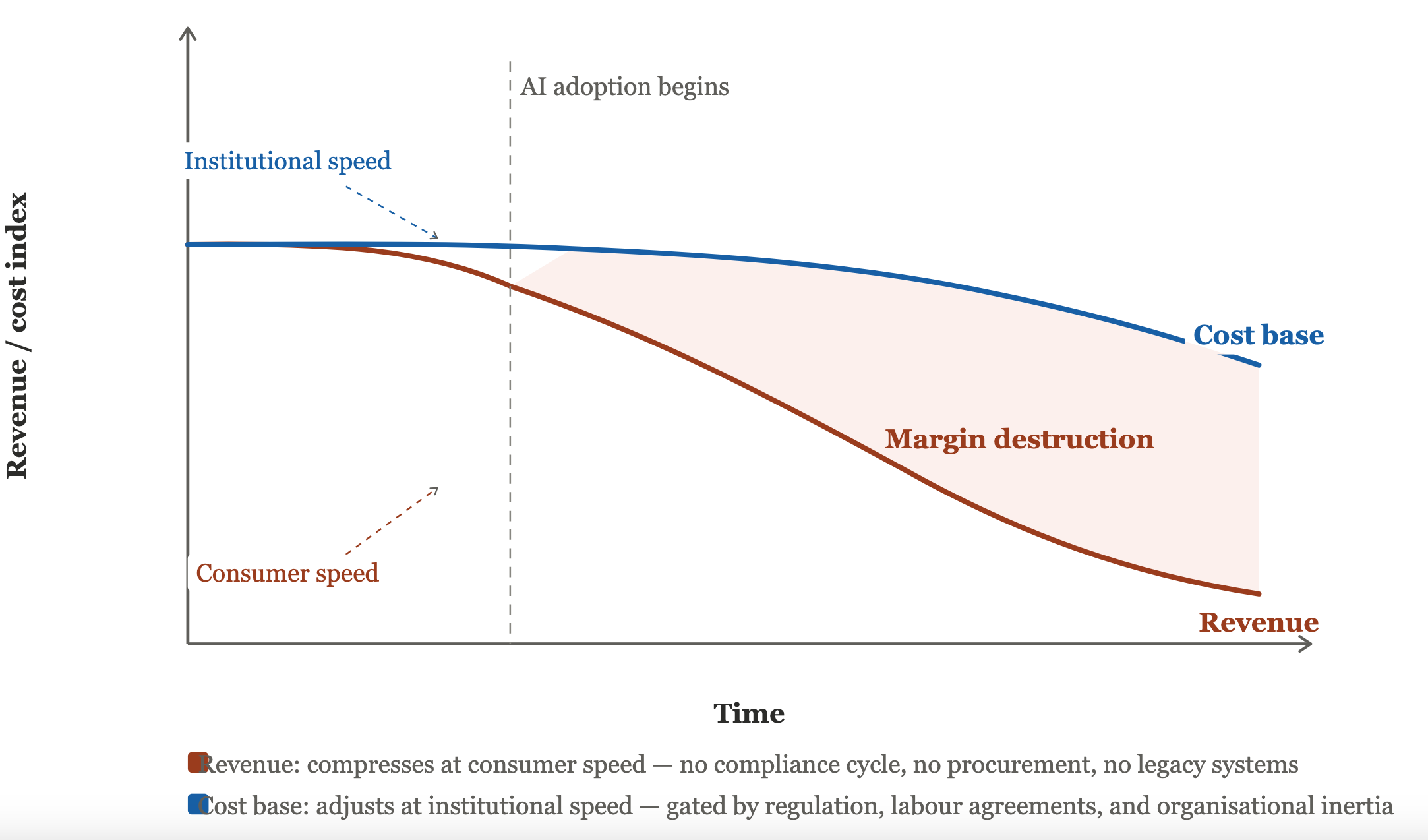

The previous issue of Stray Narratives closed with a question I deliberately left unanswered. If the Adoption Asymmetry is correct, if revenue compresses at consumer speed while costs adjust at institutional speed, then the mid-tier insurer, the second-quartile law firm, the regional financial services provider is dying in the scissors. This looks like an opportunity. A startup built from scratch on AI-native workflows should be able to offer the same service at a fraction of the cost, enter the market, and take the business. The incumbents are too slow. The challengers are nimble. Creative destruction proceeds as advertised.

It does not. The reason has nothing to do with technology and everything to do with a distinction the market has almost entirely missed.

I should acknowledge the obvious counterargument. Somewhere, as you read this, there is a venture capitalist nodding vigorously and pointing to a portfolio company doing exactly what I have just described. AI-native insurance platforms exist. AI-native legal services firms exist. Some of them are growing. I am not arguing otherwise. I am arguing that the existence of a startup is not the same thing as the existence of a distribution channel. And without a new distribution channel, the Adoption Asymmetry does not resolve. It concentrates.

A Technology Shift Is Not a Platform Shift

Sameer Singh, writing in September 2025, drew a distinction between a technology shift and a platform shift that I have not seen adequately digested in any of the investment commentary I have since encountered.

A genuine platform shift requires four conditions simultaneously: an underlying technology, a development framework built on top of it, a new access or matching mechanism that connects producers and consumers in a way that did not previously exist, and a compelling economic benefit. The personal computer was a platform shift. The internet was a platform shift. The smartphone was a platform shift. Each created not merely a new technology but a new channel through which entirely new businesses could reach entirely new customers.

AI satisfies three of the four. The technology is real. The development framework is rich and rapidly evolving. The economic benefit, particularly in the Kill Zone sectors, is beyond serious dispute. What is missing is the third condition: a new access or matching mechanism. AI products travel through the existing internet and the existing app stores. The most successful consumer AI products are so thoroughly embedded in familiar interfaces that most users interact with them without knowing they are there. The AI is inside the existing channel, not beside it.

The historical parallel Singh reaches for is the microprocessor, and it is illuminating. The microprocessor arrived in 1975. Arguably the most transformative piece of technology of the twentieth century — and for its first decade of commercial life, absorbed almost entirely by incumbents. IBM dominated the first wave of personal computing not because it built the best chip, but because it had the distribution, the enterprise relationships, and the institutional trust to reach the customers who mattered. New winners emerged only when genuine platform shifts created new channels. The PC was a new channel. The internet was a new channel. Without them, the microprocessor’s transformative potential accrued to whoever already controlled access to the customer.

We are in the same position today. The AI-native startup that wants to sell insurance must still acquire customers through the channels the incumbent already dominates: digital advertising, price comparison platforms, broker networks. It must satisfy the same regulators, obtain the same licences, maintain the same capital reserves. The technology has made these requirements slightly cheaper to satisfy. Slightly cheaper is not the same as absent.

Who Controls the Channel Controls the Gain

The investment implication follows directly, and it is worth stating plainly before examining the nuances.

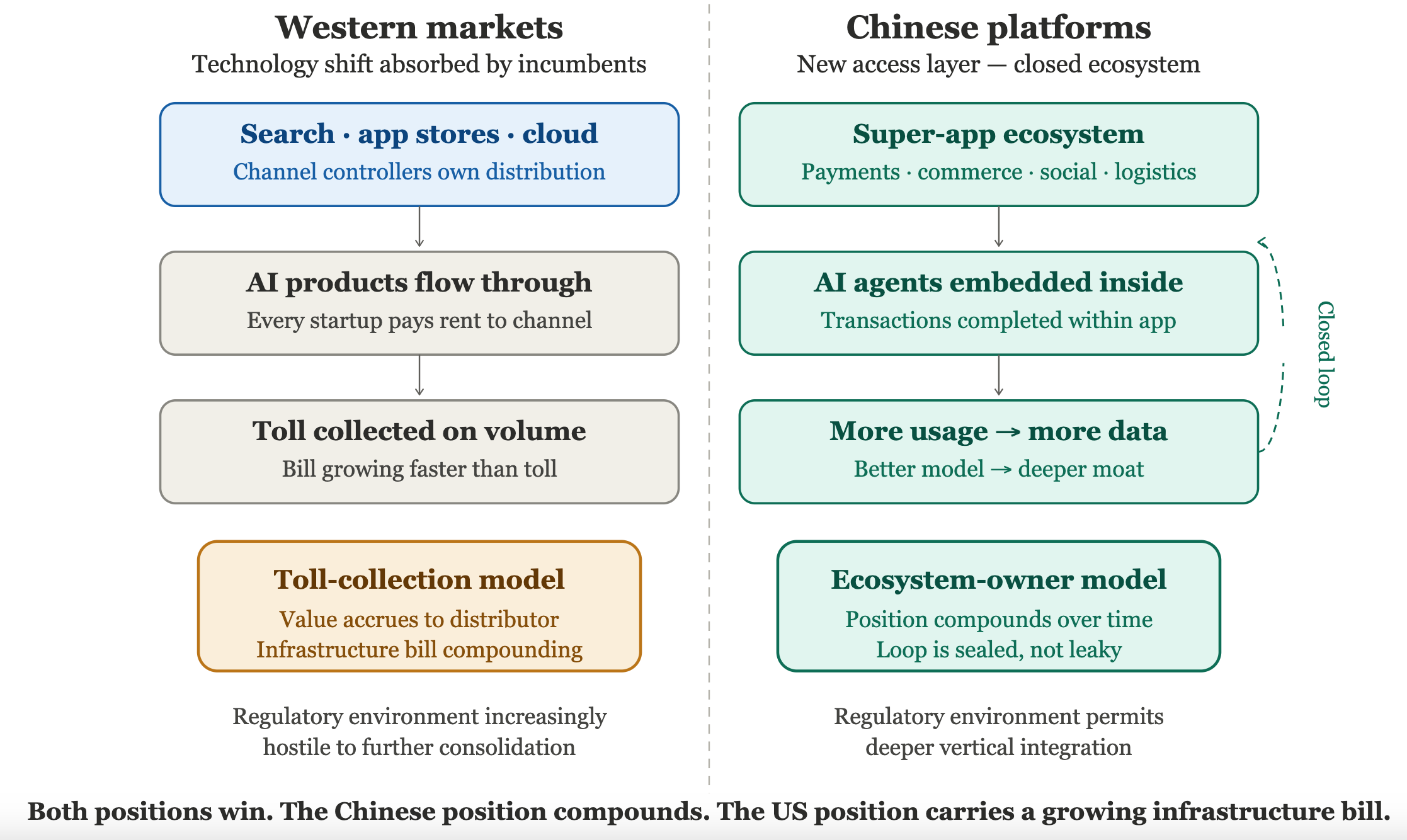

In Western markets, the channel controllers are the large technology platforms that own search, e-commerce, mobile distribution, and cloud infrastructure. Every AI product that reaches consumers in the West travels through their networks. Every AI-native startup that builds on their infrastructure pays them rent. They do not need to be the most capable AI developers. They need only to be the channel, which they already are. AI, as a technology shift absorbed into existing distribution, makes the channel controllers more valuable, not because they built the technology, but because no one can reach the consumer without them. The toll is real. But so is the bill, and the bill is growing considerably faster than the toll. The channel controllers are not entirely comfortable on their thrones. They are building infrastructure at a pace the economics of distribution alone cannot justify, and the consequences of that particular miscalculation are a subject for a later issue.

The Chinese platforms tell a structurally different story, and the contrast sharpens the argument rather than complicating it. The super-app ecosystem, WeChat, Alibaba’s Qwen, ByteDance’s Doubao is, by any reasonable definition, what Singh’s missing fourth condition looks like in practice. These platforms handle payments, commerce, messaging, logistics, and entertainment within a single environment. AI agents embedded inside them can now complete transactions, book travel, and switch between services without the consumer leaving the interface. This is a new access layer. It exists.

It exists because China’s consumer internet developed almost entirely on mobile, leapfrogging the desktop era that shaped Western markets. There were no entrenched search engines, no established e-commerce giants, no legacy financial services distribution networks to displace. There was a clean surface on which to build something genuinely new.

Western markets never had that surface. Google already owned search. Amazon already owned e-commerce. The major app stores already controlled mobile distribution. A Western super-app would need to displace all of these simultaneously, against incumbents with vast resources and deep regulatory relationships. The structural reason it has not happened is that the desktop-internet channel controllers filled the space before mobile could build something new on top of it. The China example does not undermine Singh’s argument for Western markets. It confirms it, by showing precisely what a genuine new access layer looks like, and precisely why the conditions required to build one do not exist here.

The result is an asymmetry within the winning camp. US platform operators benefit from AI as distributors: value flows through their channels, and they collect a toll. Chinese platform operators benefit from AI as ecosystem owners: every interaction deepens a closed loop in which more usage generates more data, a better model increases engagement, and the platform becomes progressively more indispensable. In the US, this loop leaks across competing platforms. In China, it is sealed. Both positions win. The Chinese position compounds. The US regulatory environment is increasingly hostile to further consolidation among large technology platforms; the Chinese regulatory environment has consistently permitted deeper vertical integration. The regulatory asymmetry compounds the structural one.

From Information to Transaction

There is a development the original Sorting Machine framework did not fully capture, and which changes the texture of the Kill Zone without altering its fundamental logic.

In the first issue of this series, I described AI as a tireless verification engine that collapses information asymmetry in every market where quality can be objectively measured. The consumer who once satisficed, who booked a good-enough holiday because finding the optimal one was prohibitively costly, now has a system that can compare every provider, read every policy document, and identify the best choice in seconds.

But AI’s trajectory in consumer markets is moving from information tool to transacting agent. An AI agent does not merely inform the consumer that a better insurance policy exists. It identifies it, completes the application, cancels the existing policy, and manages the transition, without the consumer’s active involvement beyond an initial authorisation. Researchers at MIT describe this precisely: the economic promise of agentic AI is the dramatic reduction of transaction costs, meaning not just the cost of searching, but the cost of communicating, contracting, and switching. The entire friction of changing provider, compressed to zero.

The Kill Zone implication is material. In the first wave, consumer inertia provides a residual brake on concentration. The insurer who has lost the information advantage has not necessarily lost the customer, because the customer may not get around to switching. We have all not got around to switching something. It is one of the few remaining areas of human endeavour in which I am genuinely world-class.

In the second wave, the agentic consumer switches automatically, at renewal, every year. The residual brake is gone. The best provider in each verifiable category gains share on a clock the consumer does not have to wind.

And yet this escalation takes place entirely within the existing distribution architecture. The AI agent that switches your insurance does so through existing comparison platforms, existing broker networks, existing direct sales channels. It accelerates concentration toward the best incumbent. It does not produce a new entrant.

What Margin Actually Is

Before walking through the four quadrants, I want to name a concept that sits underneath all of them, because it reframes something investors use every day without quite examining what it means.

Margin is conventionally understood as price minus cost. But looked at through this framework, margin is something more specific: it is the reward for operating in territory where neither party can fully price what is being exchanged. The seller knows something the buyer does not, or the buyer values something the seller cannot fully quantify, and the gap between those two states of incomplete knowledge is where margin lives.

What AI does, with extraordinary efficiency, is eliminate that incompleteness wherever it is artificial, wherever the asymmetry existed not because the value was genuinely uncertain, but simply because the consumer lacked the tools to measure it. Insurance premiums. Holiday pricing. The efficacy of the supplements one takes each morning with such conviction. The margin in these markets was never a reward for genuine uncertainty. It was a reward for the consumer’s inability to know better. That reward is gone.

What survives is the margin rooted in genuine uncertainty on both sides: the adviser who cannot fully price her judgment, the client who cannot fully articulate what he is paying for, the craftsman and the collector who meet in a space where neither party could produce a defensible valuation if pressed.

I should, in the interests of intellectual honesty, acknowledge the most conspicuous surviving example of margin sustained by imperfect knowledge: the financial services industry itself. An industry that publishes extraordinary volumes of research simultaneously arguing every conceivable position, that charges considerable fees to help clients navigate systems of almost infinite complexity it demonstrably does not fully understand, and that has somehow maintained its pricing power through multiple decades of embarrassing forecasting records, this is not, I would suggest, primarily a story of superior analytical capability. It is a story of genuine uncertainty on both sides of the relationship, dressed in enough conviction to justify the fee. Which is, on reflection, precisely what the framework predicts should survive. I find this more comforting than I probably should.

AI does not destroy margin. It destroys the margin that should never have existed, and in doing so, makes the question of what remains considerably more important.

Where the Value Goes

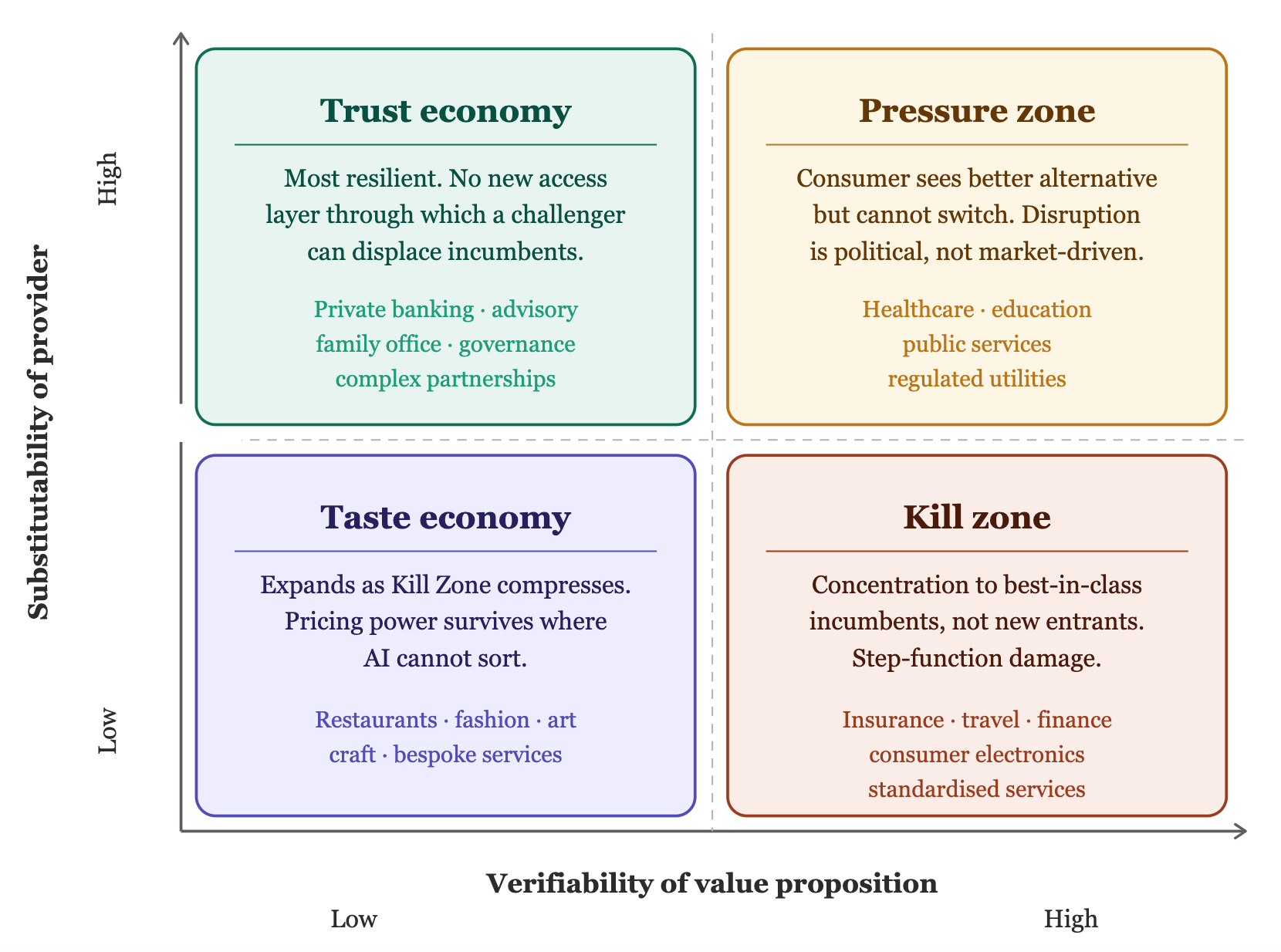

The Kill Zone. Concentration accelerates, and more severely than the first-wave analysis suggested. The agentic escalation removes consumer inertia as a brake on switching. The best-in-class provider in each verifiable category no longer competes for the marginal customer who might eventually switch. It competes for the automatic, frictionless capture of every consumer whose AI agent has identified it as optimal.

The concentration does not flow to AI-native entrants. It flows to whoever is already best-in-class, because they occupy the top of the ranking the AI agent consults. The thirty year old insurer with the best claims ratio captures the gains. The AI-native challenger must first build a claims ratio, years of underwriting experience, a capital base adequate for the regulator, customers acquired through channels the incumbent already dominates. The technology accelerates the existing competitive structure. It does not disrupt it.

The damage to mid-tier incumbents is a step-function, not a gradual decline. A regional insurer losing thirty percent of its book in twelve months crosses a viability threshold no cost-cutting programme can address on the required timeline. The business that emerges from its ruins is not a nimble challenger. It is the market leader, larger than before.

The Pressure Zone. AI gives consumers and citizens the tools to see the gap between what exists and what is possible, the school that performs worse than the one across the boundary, the hospital with higher infection rates. But the consumer cannot switch. Switching costs are geographical, regulatory, or infrastructural. Disruption here is political rather than market-driven: the voter who now has the data to demand accountability becomes more dangerous to incumbents than any startup. The political cycle, not the product cycle, is the relevant clock.

The Taste Economy. This quadrant expands, and more durably than the consensus expects. As Kill Zone margins collapse, consumer spending and entrepreneurial energy migrate toward domains where subjective judgment is the value proposition. The restaurant that resists comparison on a standardised metric. The fashion label whose value is cultural cachet. The craftsman whose work means something precisely because no algorithm selected it. The consumer who spends her working life in an economy of frictionless optimisation wants, in her discretionary spending, the experience of choosing for reasons she cannot fully defend. Taste cannot be learned by aggregate pattern recognition. If it could, it would not be taste.

The Trust Economy. This is the most resilient quadrant, and the distribution argument explains why more precisely than the obvious observation that trust takes time to build.

The Trust Economy is protected not because trust accumulates slowly, but because there is no new distribution layer through which a challenger could reach the client in the first place. The private client who has worked with the same adviser for twenty years receives unsolicited approaches regularly. She ignores them not because they are technically inferior, but because switching means rebuilding from scratch a shared understanding of her situation: the family’s governance structure, the tensions between generations, the assets whose disposal carries emotional as well as financial weight. No AI agent can intermediate that transition. It requires exactly the contested, coordinative, trust-dependent work that sits in the quadrant where AI cannot operate.

When the verifiable layer compresses and the Kill Zone concentrates, the decisions that remain are disproportionately those that resist verification: how to structure a business succession, how to navigate a regulatory investigation, how to advise a family whose patriarch and heirs disagree about what the wealth is for. These decisions do not migrate to the AI platform. They migrate to the Trust Economy’s existing networks, and those networks face no new distribution threat, because no new distribution exists.

What the Market Is Pricing

The consensus is right that AI compresses margins in verifiable sectors. The Adoption Asymmetry is real, its mechanism is operating, and it is not priced in anything like its full severity. On this point, the bears are closer to correct than the bulls, even if the bears have the wrong causal story.

What the consensus is not pricing is the distribution of the gains. AI is a technology shift absorbed into existing channels, not a platform shift that displaces them. The benefits do not accrue in proportion to AI capability. They accrue to whoever controls the distribution layer through which the capability reaches the consumer. The market is pricing the means of verification: chips, data centres, models, inference infrastructure. The scarce resource, in an economy where verification is becoming free, is the channel that delivers the verified product, and the institutional trust that makes the consumer accept the delivery.

There is a further irony worth noting, with the restraint appropriate to a publication that takes itself, if not too seriously, at least seriously enough. The companies investing most heavily in AI capability are, by the logic of their own products, learning the institutional grammar of every industry they serve. The consulting firm that uses an AI platform to improve its analytical output is, in aggregate with every other consulting firm doing the same, contributing to the platform's ability to offer consulting services directly. Andrea Pignataro describes this as a tragedy of the commons: every firm's individually rational adoption of AI accelerates the platform's ability to disintermediate the entire industry. The firms will, in due course, have taught the system everything it needs to make them unnecessary. I mention this not as a counsel of despair but as a final reminder that value ends up, reliably, with whoever controls the access layer.

What Comes Next

The distribution argument answers the question left open at the end of the previous issue. New AI-native competitors cannot resolve the Adoption Asymmetry because the Adoption Asymmetry is not a technology problem. It is a distribution problem. The scissors closes on mid-tier incumbents not because they are outcompeted by more capable challengers, but because the best incumbent in each verifiable category captures a disproportionate share of a market sorted by an increasingly agentic optimisation engine, operating through existing channels the incumbent already controls.

When a mid-tier business crosses its viability threshold, and the step-function nature of the Kill Zone means crossings are sudden not gradual, the sequence that follows is not orderly restructuring. It is the sequence businesses under severe margin pressure have always followed: hiring freezes before layoffs, bonus pools before salaries, real-terms cuts before nominal ones. The labour market effects propagate through this sequence in businesses that have not yet failed and may not for some time. The scissors compresses wages before it eliminates jobs, and the suppression extends well beyond the directly affected sectors: the worker in an adjacent industry who might otherwise have negotiated a raise knows perfectly well what is happening to her peers.

When those viability thresholds are crossed not in one sector but in every verifiable consumer-facing sector simultaneously, at consumer speed, the aggregate effect is something the standard productivity analysis, which examines industries in isolation, is not designed to see.

What that looks like is the subject of the next issue.

This newsletter takes many hours to research, report out, and write. If you find value in this essay, please press the “like” button. Many thanks!

The Distribution Argument: A Quick Reference

Platform shift vs technology shift: A genuine platform shift requires a new access or matching mechanism. AI has no such mechanism in Western markets. Without a new distribution layer, AI capability accrues to whoever controls the existing channels, not to new entrants.

Who controls the channel: US platform operators win as distributors — AI flows through infrastructure they already own. Chinese platform operators win as ecosystem owners, closed super-app loops compound. Both win. The Chinese position is structurally deeper. The US position carries a growing infrastructure bill that distribution economics alone cannot justify.

The agentic escalation: Moving from AI as information tool to AI as transacting agent removes consumer inertia as a brake on concentration. The Kill Zone intensifies: the best incumbent gains share automatically. The challenger still needs to reach the consumer through channels the incumbent dominates.

Margin as imperfect knowledge: Margin is the reward for operating where neither party can fully price what is exchanged. AI eliminates the margin earned on artificial information asymmetry. The margin that survives is rooted in genuine uncertainty on both sides. AI does not destroy margin. It destroys the margin that should never have existed.

Value migration: Kill Zone concentration flows to best-in-class incumbents. Pressure Zone disruption is political, not market-driven. Taste Economy expands as pricing power migrates toward the unverifiable. Trust Economy is most resilient: no new distribution layer through which a challenger could displace existing trust networks.

References

[1] Stray Narratives, Issues 01 and 02: “The Sorting Machine” and “Contested Ground.” The Verification-Substitution Matrix, the Adoption Asymmetry, and the revenue-cost scissors are developed in full in those issues.

[2] Sameer Singh, “AI is a Technology Shift, not a Platform Shift,” breadcrumb.vc, September 2, 2025. The four-condition framework for platform shifts, the microprocessor historical parallel, and the argument that AI’s missing condition is a new access layer are drawn from this essay.

[3] Andrea Pignataro, “The Wrong Apocalypse,” February 15, 2026. The substitution fallacy, the grammar of organisational life, and the tragedy of the commons argument are drawn from this essay.

[4] MIT Sloan School of Management, “Agentic AI, Explained,” February 18, 2026, drawing on research by Horton, Shahidi, Kellogg, and Aral. The formulation of agentic AI’s economic promise as the dramatic reduction of transaction costs is drawn from this piece.