What Will Be Scarce After AI?

Stray Narratives, Issue 14: The Post-Commodity Economy and What AI Cannot Make

Key Takeaways

The Law of the Post-AI Economy: What an algorithm can codify drops to near-zero cost; what it cannot produce becomes exponentially more valuable. The wealth freed up by collapsing commodity costs doesn’t vanish—it migrates directly toward scarcity. The engine is psychological, not technological. Comin and Lashkari find that roughly three-quarters of the century-long shift in consumption is driven by income effects rather than Baumol’s cost disease: as people get richer, they stop paying for utility and start paying for human provenance and social signal.

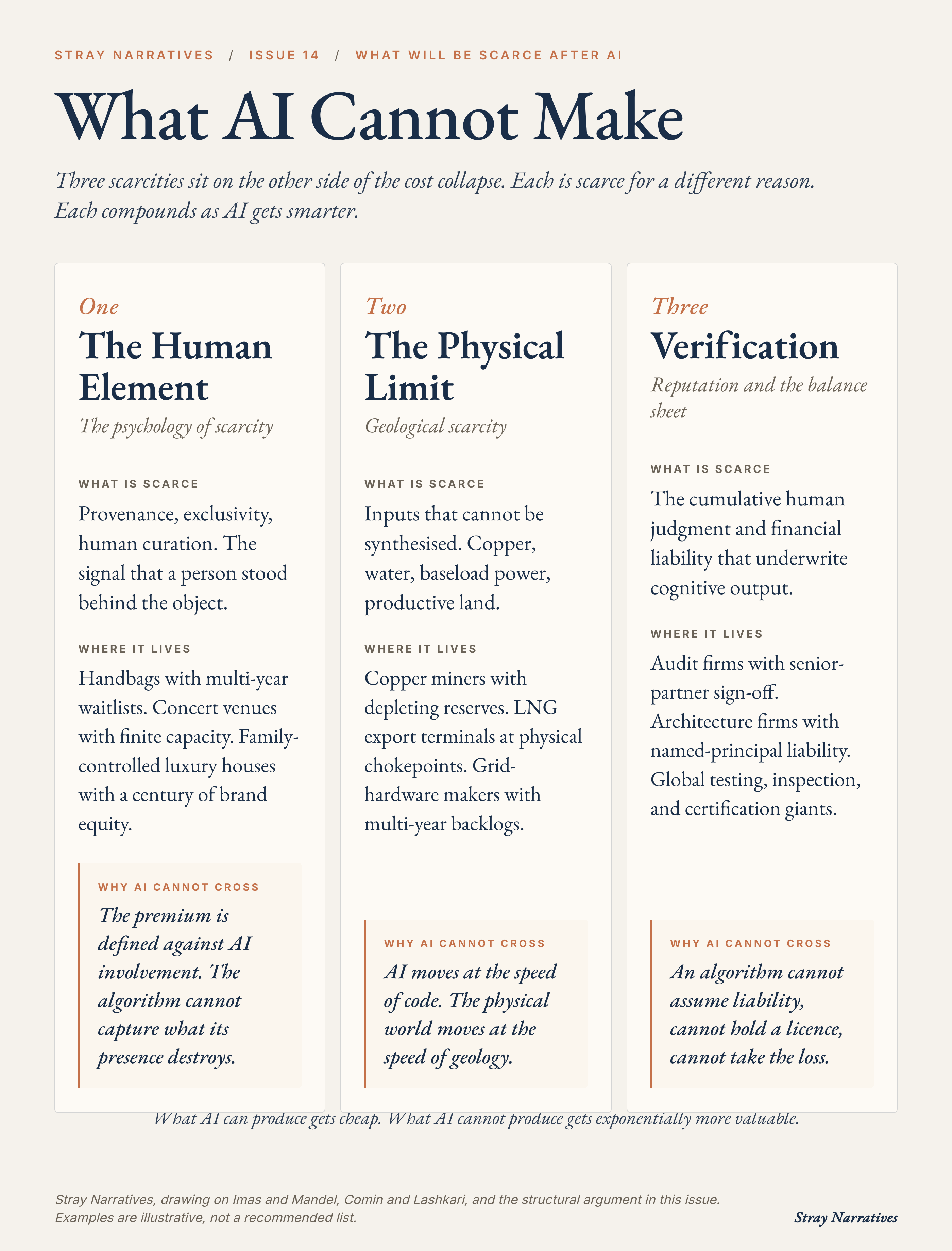

Three scarcities sit on the far side of the cost collapse, each scarce for a different reason and each compounding as AI improves: the Human Element (provenance, exclusivity, curation), the Physical Limit (copper, power, and land that cannot be synthesised), and Verification (the judgment and liability that underwrite cognitive output).

The labour market splits in two: the junior doing commodity work loses leverage to the model, the senior holding the licence and the liability keeps the margin, and the middle is squeezed. One honest correction to our earlier work — the early hollowing-out of entry-level hiring tracked remote work more closely than AI. The AI displacement is additive, and still ahead of us.

The conclusion is to own the chokepoints, not the AI software winners: human-element brands with waitlists, physically constrained real-asset producers, and the verification moats of audit, certification, and named-principal liability. Late in the Kondratiev cycle, with the next secular bear likely inflationary, these hold pricing power while commoditized producers compress to zero real margin.

Here below is the AI Podcast version of this same article:

Starbucks tried to automate. A $112 billion company selling one of the most standardised products in the modern economy spent years systematically removing labour from its stores.

Then, this spring, CEO Brian Niccol reversed course. He brought back handwritten notes on cups. Ceramic mugs. The return of great seats. More baristas, not fewer. He reinvested in the hospitality, not the coffee. [1]

Read carefully, that decision points at the entire post-AI economy. Starbucks reached for what AI could not replace, because what AI could replace was no longer the thing customers were actually paying for.

The consensus story about artificial intelligence assumes that when machines can produce anything humans can produce, the jobs disappear and human economic value goes to zero. That view is fundamentally backward.

The principle of the new economy is entirely mechanical, and it fits into one sentence: What AI can produce gets cheap; what AI cannot produce gets exponentially more valuable.

AI is a production technology. It compresses the cost of producing the things it can codify. Anything fungible, anything modular—the cost curve collapses, and the price follows. But as the cost of these commodities drops to near-zero, the freed-up capital and consumer spending do not disappear. They migrate.

The most important investable question of the next decade is where that money flows. The data shows it flowing directly toward three distinct scarcities that possess moats an algorithm fundamentally cannot cross.

The Engine: The Psychology of Wealth

We are consistently told that services dominate the modern economy because they resist automation. That is mostly false. In 2021, economists Diego Comin and Danial Lashkari showed that this price effect—Baumol’s cost disease—only accounts for about a quarter of the macroeconomic shift. The other 75% is driven by income effects. [2]

When income rises, people stop paying for pure utility and start paying for social signals. You can see this clearly in US consumer data: the wealthiest 20% of households don’t just consume a larger volume of goods than the bottom 20%; they disproportionately shift their wealth toward categories with a heavy relational component—in-person dining, entertainment, and exclusive services. [3]

This is the macro engine of the post-AI economy. The structural reallocation of wealth runs on human psychology, not just technology. Even if AI can automate a luxury service for pennies, wealthy consumers will still shift their spending toward the human alternative—because paying for the human alternative is the point.

Which brings us to the first scarcity.

1. The Human Element (The Psychology of Scarcity)

Nobody who buys a $3,000 Armani suit is buying a more efficient way to stay warm. They are buying the brand, the social meaning, and the fact that other people know what it is but cannot have it.

As utility gets cheap, the premium on social signalling skyrockets. Demand shifts toward goods whose entire value is derived from human provenance, exclusivity, and taste.

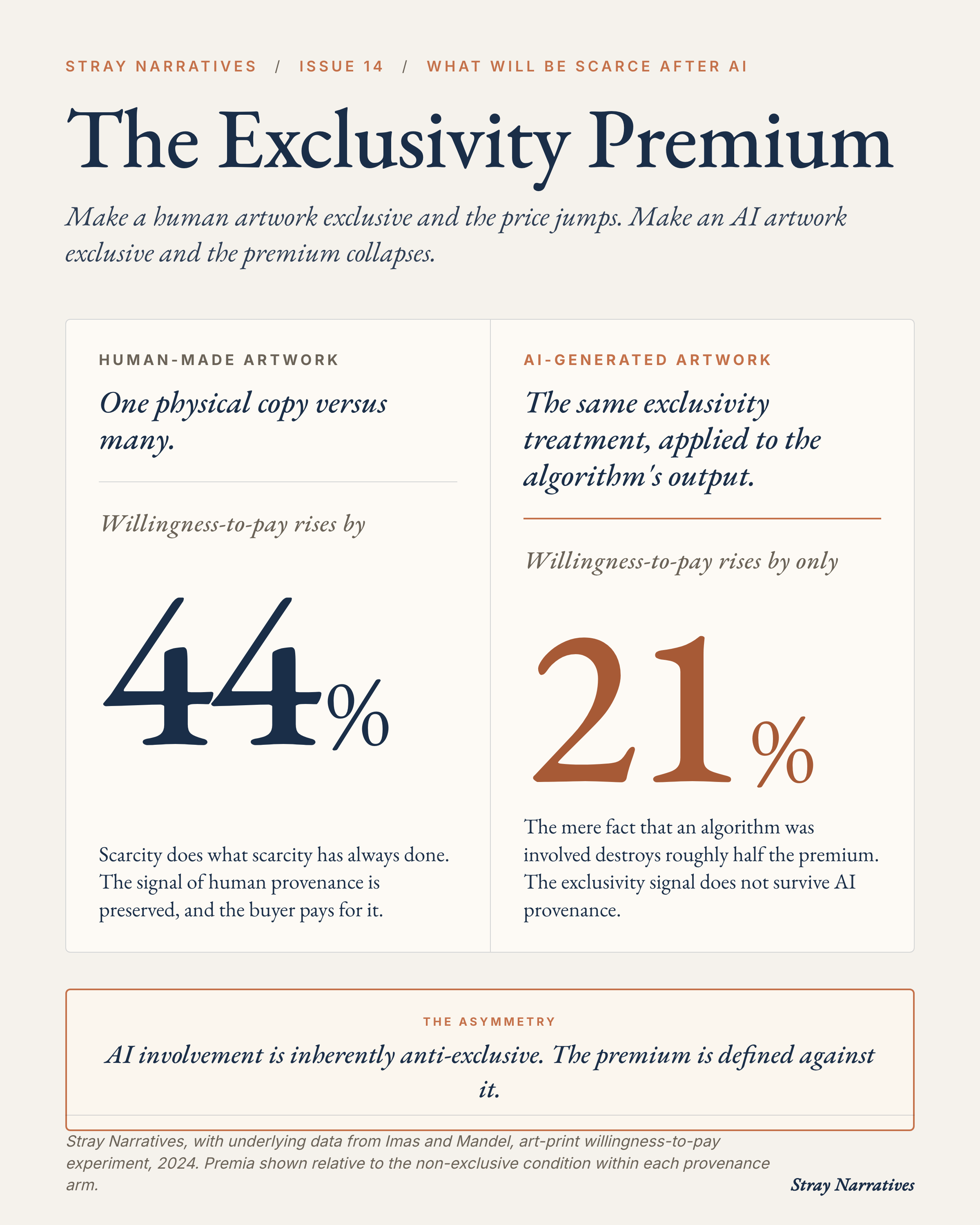

Economists Alex Imas and Graelin Mandel recently ran an experiment using physical art prints that serves as the single most important data point for understanding consumer behaviour in the AI era. When human-made artwork was made exclusive (one physical copy versus many), its value jumped by 44%. But when AI-generated artwork was made exclusive, that premium collapsed to just 21%. [4]

Sit with that finding. The mere fact that an algorithm was involved in producing the object destroyed the exclusivity premium. AI involvement is inherently anti-exclusive. It cannot capture the premium that comes from human provenance because that premium is defined entirely against AI involvement.

Furthermore, as AI drops the cost of generating content and products to zero, supply becomes infinite. When supply is infinite, the ultimate scarcity is the Filter. The market will pay massive premiums for human curators, tastemakers, and editors who filter the deluge of AI-generated noise and dictate what is actually worth our attention.

2. The Physical Limit (Geological Scarcity)

AI moves at the speed of code. The physical world moves at the speed of geology.

You can prompt-engineer a million lines of code in seconds, but you cannot prompt-engineer a new copper mine, a gigawatt of baseload power, or a new water basin. We are currently watching the algorithmic, exponential growth of AI compute collide directly with a physical supply curve that refuses to budge.

Look at the agricultural equivalent: productive land and water rights. In California’s Central Valley, the breakeven on planting a new almond orchard has stretched to twenty years because water is so physically and regulatorily constrained. [5] The marginal acre is uneconomic. The supply curve is effectively dead. A coming issue will lay out the investment case on this specifically.

Just as AI destroys the exclusivity premium of luxury goods, it is completely powerless to synthesise base reality. Whether you are looking at copper miners with depleting reserves, LNG export terminals with physical chokepoints, or grid hardware manufacturers with multi-year backlogs, the thesis holds.

3. Verification (Reputational Scarcity & The Balance Sheet)

If the demand side of the new economy is driven by the human element, the supply side is driven by verification and risk.

AI is aggressively commoditising the raw materials of cognitive work: drafting, data analysis, calculation, and pattern recognition. When the cost of producing complex cognitive output drops to near-zero, the output itself is no longer the product. What stays valuable is the signature and the balance sheet.

An AI can draft a flawless 50-story architectural blueprint for a fraction of a cent. But an AI cannot assume liability if the building collapses. It cannot go to jail. It cannot hold a licence. Similarly, an AI can mathematically underwrite a massive commercial real estate loan, but the AI cannot take the financial loss if the borrower defaults. Risk capacity is strictly constrained by human or institutional capital.

The medical opinion, the audit letter, the legal interpretation, the structural stamp—the underlying work product gets cheap, but the cumulative human judgment and financial liability that underwrites it stays scarce.

This dynamic will produce a bimodal compression in the labour market as AI capability matures. The junior associate doing commodity drafting loses leverage to the model; the senior partner holding the liability licence captures the margin. The middle gets squeezed, the top compounds—and the speed of that compression will be the central question of the next five years.

A Note on Sequencing and a Correction: We have argued in previous issues that AI was already compressing entry-level hiring across the professional services pyramid. We were wrong. The decline in entry-level cognitive jobs through 2024 pre-dates the deployment of frontier AI models and tracks the rise of remote work far more closely than AI adoption. Recent SSRN research, sharpened by Paul Kedrosky’s analysis, makes this point cleanly [6]: WFH did the early hollowing-out, and we got carried away by a narrative that fit our broader thesis a little too well. It was the wrong attribution made for the right structural reason.

This matters, and how we handle it matters more. We must hold our views with the same conviction we hold our trades: tight when the evidence supports them, updated the moment it doesn’t. We are here to learn more, and to learn better — and the evidence has just moved again. The thesis remains structural, but it is no longer purely forward-looking. The newest firm-level data shows the AI leg has begun: among companies a year or more into AI deployment, roles are already being cut, a net loss on the order of five per cent over the past year, and the cuts land hardest on the youngest, several times harder than on senior staff [7]. The economy-wide picture stays muted, because deep adoption is still narrow: across the whole business population, most firms still report no employment effect at all [8]. Both are true at once, and the reconciliation is the point. Remote work did the first hollowing of the junior pipeline; AI has started the second, at the adoption frontier, and on the young, and it broadens as adoption spreads. The shock is additive, and it has already begun.

Where the Capital Should Sit

The investment framework over time will not be about picking the AI software winners. It will be about owning the chokepoints of the post-commodity economy.

The Human Element (Product as Signal & Filter): Businesses where the human element, curation, or exclusivity is the product itself. Handbags with multi-year waitlists. Concert venues with finite capacity. Family-controlled luxury houses with a century of brand equity.

The Physical Limit (Dead Supply Curves): Businesses where the input is physically constrained. Copper miners with depleting reserves. Energy infrastructure and grid hardware manufacturers with multi-year backlogs.

The Verification Moat (Irreducible Signature): Businesses on the supply side of cognitive production where the human signature and balance sheet are the units of value. Global testing, inspection, and certification (TIC) giants. Audit firms with senior-partner sign-off authority. Architecture firms with named-principal liability.

The Bottom Line

The consensus assumes that because the commodity form is completing itself—delivering products with zero human involvement at near-zero marginal cost—the value of human economic output goes to zero.

In reality, cheap commodities free up real income. That income flows directly toward comparative preferences, physical constraints, human curation, and liability-bearing signatures.

The macro environment makes positioning for this reallocation urgent. We are sitting on the late-stage side of the Kondratiev long cycle. [9] Historical patterns—moving through 1930s deflation, 1970s inflation, and 2000s deflation—suggest the next secular bear market will likely be inflationary. Real-asset businesses and luxury brands with pricing power survive inflationary regimes by definition. Commoditised producers compress against zero real margin.

But there is a looming, darker question here. If AI concentrates wealth into the hands of capital owners, and systematically compresses the wages and leverage of the middle class, the tax base of the sovereign state collapses exactly when society demands a bailout.

What happens politically when a highly educated, newly displaced class gets angry? That is the subject of a coming issue.

References

[1] Starbucks “Back to Starbucks” turnaround under CEO Brian Niccol: the reversal of in-store automation in favour of hospitality — return of ceramic mugs, handwritten notes on cups, and condiment bars, alongside increased barista staffing (staffing raised at ~3,000 stores; a 700-store coverage pilot). Niccol’s remark that the chain had “ran like a manufacturing facility” per Fortune, 23 March 2026; programme detail per Starbucks corporate, “Back to Starbucks,” 2025, and Reuters reporting, May 2025.

[2] Diego Comin, Danièle Lashkari, and Martí Mestieri, “Structural Change with Long-Run Income and Price Effects,” Econometrica, Vol. 89, No. 1 (2021). Income effects account for roughly three-quarters of the long-run shift in consumption structure; the Baumol price / cost-disease channel for about a quarter.

[3] US Bureau of Labor Statistics, Consumer Expenditure Survey, 2022 — top-quintile versus bottom-quintile expenditure on relational categories (in-person dining, entertainment, personal services). Corroborated across the universe of US consumer spending by Joachim Hubmer, “The Race Between Preferences and Technology,” Econometrica, 2023.

[4] Alex Imas and Graelin Mandel, experimental findings on AI involvement and the exclusivity premium for human-made versus AI-generated artwork — a +44% exclusivity premium on human-made prints versus +21% on AI-generated prints. Summarised in Alex Imas, “What Will Be Scarce?”, Ghosts of Electricity (Substack), 2026, with companion technical note at aleximas.com.

[5] California’s Sustainable Groundwater Management Act (SGMA), now in enforcement across the San Joaquin Valley, with irrigation districts shutting deep-well agricultural pumps from 2026; the Public Policy Institute of California projects that pumping reductions could take up to ~20% of San Joaquin Valley farmland out of production by 2040. Almond orchards (3–4 acre-feet of water per acre, and non-fallowable once planted) are the marginal casualty.

[6] Peter John Lambert and Yannick Schindler, "The Broken Ladder: AI, Remote Work, and Early-Career Hiring," SSRN working paper, 2026 (analysis of ~243 million new hires and ~407 million job postings across the US, UK, Canada and Australia, 2017–2025); when work-from-home and generative-AI exposure are estimated jointly, the work-from-home effect on the junior-hire share holds while the AI coefficient attenuates toward zero. Analysis sharpened by Paul Kedrosky.

[7] A major global investment bank’s proprietary adoption survey (April 2026; ~800 companies across banking, software, tech hardware, semiconductors and professional services in the US, UK, Germany, Japan and Australia, all 12-month-plus AI adopters): a net ~5% reduction in roles over the prior year, with eliminations and non-backfilled positions concentrated in early-career staff — roughly six times the rate of the most experienced. Anonymised per house sell-side policy.

[8] US Census Bureau, Business Trends and Outlook Survey (BTOS), 2026: fewer than 20% of US firms report any AI use in a given two-week window; over 90% report no employment effect from AI over the prior six months; among firms reporting an effect, more cite increased than decreased employment. The most AI-exposed sectors account for roughly 15% of total US employment.

[9] Kondratiev long-cycle framework as documented across roughly a century of bond-yield and secular equity-cycle data; current late-cycle position per a long-cycle macro strategist’s May 2026 work (anonymised per house attribution policy). The three prior US secular bear markets — 1930s deflationary, 1970s inflationary, 2000s deflationary — bracket the pattern.