The Bull Market In Politics

Stray Narratives, Issue 15: What happens when AI hollows out the middle class and the political system comes for the winners.

In May, India’s Chief Justice described the country’s unemployed graduates as “cockroaches” and “parasites of society” in open court. Within six days, a satirical Cockroach Janta Party had more Instagram followers than the ruling party that has governed India since 2014. Behind the joke sits the number that made it land: roughly 40% of Indian graduates under 25 have no job [1]. When a society produces far more credentialed aspirants than it can absorb, the surplus turns political. We have entered the era of the jobless boom, where output rises, payrolls stall, and the gains accrue to capital.

When a technology concentrates wealth this completely in the hands of capital owners, the political system reacts, as it has at every comparable point in modern history. AI does not ask for stock options, does not unionise, and does not complain about the return-to-office mandate, which is precisely why the reaction will not come from inside the companies. The previous issues in this series traced where economic value migrates as the cost of cognition collapses: toward what AI cannot make — the human element, physical limits, and verification capacity.

The central investable question of the next decade is what the political system will do to the winners.

Morrow’s Diagnosis

In the years around the Great Financial Crisis, Robertson Morrow, a macro thinker and former CIO at Peter Thiel’s Clarium Capital, wrote a paper titled “The Bull Market in Politics” — the paper this issue takes its name from [2]. His argument was simple: going forward, government influence over trade, immigration, social policy, and the decisions of war and peace would matter more to investors than business fundamentals ever would.

He was exactly right, and his thesis perfectly describes the post-AI economy. When the economic engine stops working for the median voter, policy swings take over the wheel.

What is currently breaking that engine? We are watching the bimodal compression of cognitive labour begin [3]. It is driven by two opposing forces acting on the market simultaneously:

The Pull of Commodification: Capital pushes anything codifiable toward zero cost. If a task can be modelled, AI does it for fractions of a cent. The cost curve for that work collapses.

The Pull of Irreducibility: What AI cannot do — cumulative judgment, signature liability, primary-source relationships, taste, and verification authority — becomes aggressively more scarce and exponentially more expensive.

The middle will get eaten from both sides. The routinely competent professional — the junior associate, the mid-tier analyst, the junior radiologist — is structurally exposed: their commodifiable output is absorbable by the model, while they lack the accumulated reputation and liability-bearing capacity that defines the top tier. As AI capability matures, the two ends of the economic spectrum will pull violently apart, and the middle will vanish.

Roughly 13% of US cognitive jobs, over 21 million workers, sit directly in the path of that compression [4]. Wage data reveals polarisation of this kind only in retrospect, on a lag of years, and the deployment wave is barely three years old. What shows up so far is concentrated in the occupations where adoption ran first. But the real political danger isn’t happening at the bottom of the income ladder. It is happening in the upper-middle-class waiting room that this compression is emptying.

Elite Overproduction: The Holding Pen is on Fire

This brings us to Elite Overproduction, a concept pioneered by historical macro-sociologist Peter Turchin [5].

Turchin studies history through the lens of population dynamics, and his thesis is dangerously relevant today: late-cycle societies produce far more credentialed “elite aspirants” than there are elite slots to absorb them. The American numbers tell the story plainly. The number of US lawyers tripled from roughly 400,000 in the mid-1970s to 1.2 million by 2011, while the population grew only 45 percent. MBAs over the same window grew six-fold [6]. The supply of credentialed aspirants for elite positions has run miles ahead of the fixed supply of positions themselves.

For decades, the economy kept these surplus elites pacified with high-paying, middle-management cognitive jobs. It was a massive holding pen for ambition. AI is the match held to it.

Nothing radicalises a population faster than a newly minted professional who realises their expensive master’s degree merely qualifies them to supervise a chatbot. When you have too many ambitious, highly educated people fighting over a rapidly shrinking pool of status-bearing jobs, they don’t form a support group. They fracture the political system.

Historically — whether you are looking at the late Roman Republic, pre-revolution France, or the late Russian Empire — intra-elite competition destroys institutional trust. The frustrated elite aspirants turn populist, harnessing the anger of the broader working class to tear down the very structures that locked them out.

The Fujiwara Effect: When Labour Throws a Brick

If Elite Overproduction explains the anger of the professional class, the Fujiwara Effect explains the mechanics of how that anger rewrites the rules of the market.

Borrowed from meteorology, where it describes two or more cyclones merging into a single larger system, the Fujiwara Effect has been made the organising metaphor of Viktor Shvets’s recent work as Global Strategist at Macquarie Capital, most fully developed in The Twilight Before the Storm [7]. In Shvets’s reading, three cyclones are converging: three decades of neoliberal policy, deep financialisation, and the disruptive Information Age now turbo-charged by AI. The central observation is grim: as these forces compound, the “winner-takes-all” dynamic becomes absolute, and the marginal economic utility of human labour collapses. First they came for the blue-collar assembly lines; now they have come for the white-collar spreadsheets.

But Shvets makes a lethal political observation: the changing value of votes.

When a median worker realises their labour no longer gives them any leverage over capital, they remember they still possess one asset the market hasn’t fully depreciated: their vote. And they tend to throw it like a brick.

The democratic system’s traditional mechanism for absorbing inequality is to translate economic discontent into gradual policy shifts. But when labour’s leverage falls this fast, gradualism dies. Silicon Valley billionaires suddenly discovering a deep, philosophical interest in Universal Basic Income isn’t altruism [8]. It is fire insurance. The serious versions are already being drafted, from corporate “displacement taxes” to an AI dividend fund modelled on Alaska’s [9]. They can read the room. They understand that a society where capital owns everything AI cannot make, and labour fights over the shrinking pie of what it can, is a society begging for a wealth tax.

The Catalyst: The Sovereign Accounting Trap

The sociological anger is the fuel, but the spark that ignites the political snapback is pure accounting. Modern Western governments fund themselves primarily through taxing labour (income and payroll taxes). Capital is highly mobile and taxed at much lower effective rates.

Every point of GDP that migrates from salaries to capital income leaves the payroll-tax net with it. If the bimodal compression runs its course, the sovereign tax base hollows out at precisely the moment the political system requires trillions of dollars to pacify a fractured, jobless middle class (via UBI, bailouts, or aggressive stimulus).

How does a sovereign fund a massive redistribution with a shrinking tax base? It cannot do it through gradual policy. It is forced into draconian asset taxes, financial repression, and aggressive currency debasement. This is the mechanical proof for why the coming crisis resolves via inflation.

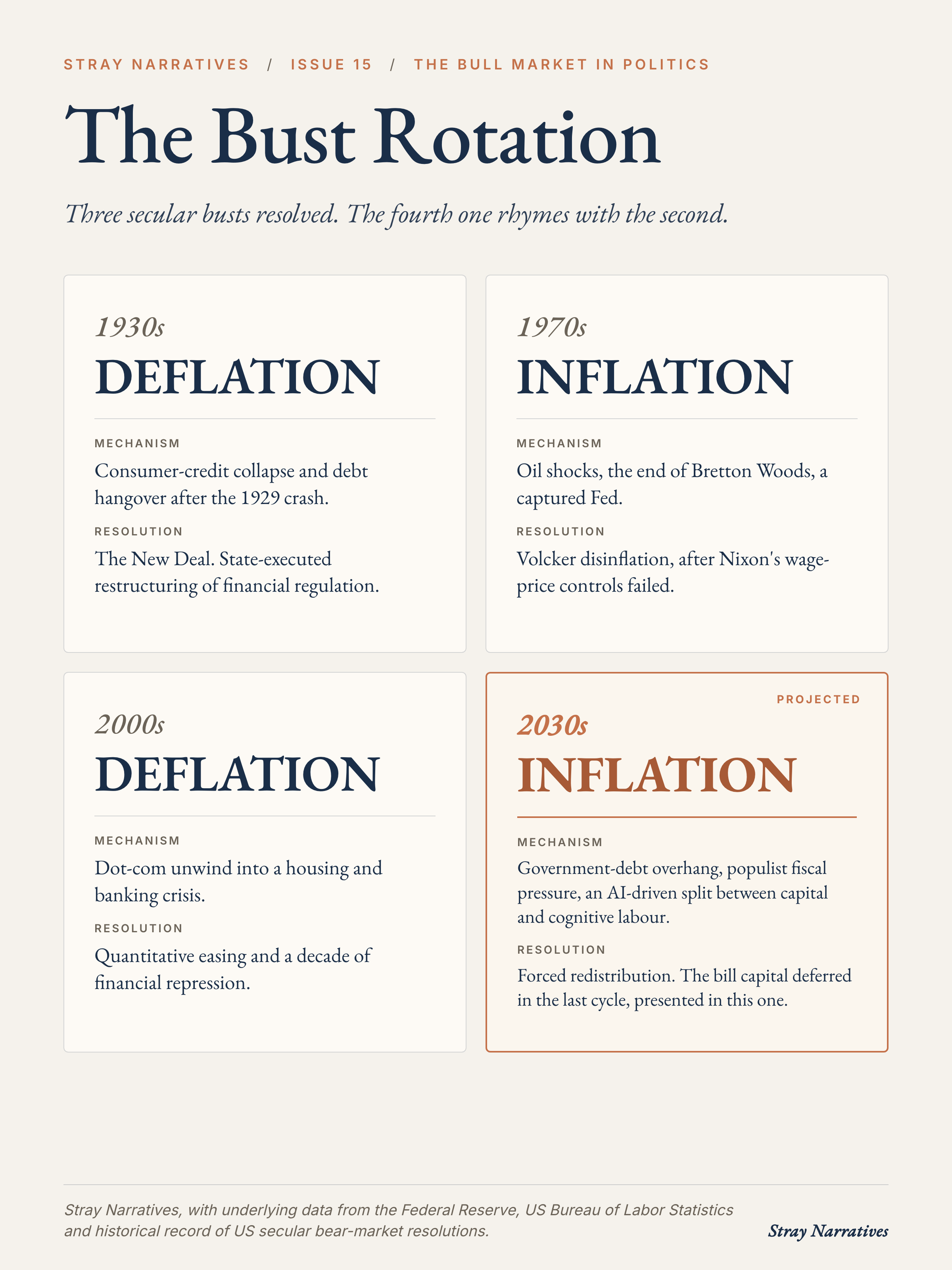

The Inevitable Snapback: History’s Rhythm

No serious analytical framework predicts that accelerating disparity at record levels resolves itself gracefully. The tension always breaks, and it breaks via state intervention.

Look at the resolution of the three prior US secular bear markets:

The 1930s (Deflationary): Resolved through the New Deal. A massive, state-executed restructuring of financial regulation, forced by the undeniable political pressure of mass unemployment.

The 1970s (Inflationary): Resolved through Volcker’s extreme disinflation, after the failure of Nixon’s wage-price controls [10].

The 2000s (Deflationary): Resolved through Quantitative Easing and financial repression [11]. This was a massive wealth transfer to capital owners to solve a banking crisis. It saved the system, but the bill for that disparity is now coming due.

A forced redistribution is coming. The only question for an investor is how to position capital before the politicians finish drafting the legislation.

The Investable Playbook: What This Means for Capital

The political question is not if the state will intervene to redistribute wealth, but where it will aim when it does.

Overweight the Diffuse Scarcities (Real Assets & The Human Element): Capital owners of what AI cannot make — relational-sector luxury brands and physical-input chokepoints — hold pricing power that is durable to inflation. More importantly, they possess political camouflage. A politician is highly unlikely to nationalise an ultra-luxury handbag boutique, and they cannot easily expropriate a fragmented network of prime agricultural land. The populist case against them is weak.

*The Macro Caveat:* Do not mistake political camouflage for invincibility. During an inflationary bust, the state will not outright steal the copper mine, but it will absolutely levy windfall taxes on the excess margin or impose price caps. You own these assets to survive the currency debasement, but you must actively manage the margin risk.

Overweight Verification Infrastructure: If AI drops the cost of cognitive output to near-zero, the economic value migrates entirely to the entity that stamps it as true. Think of the global testing, inspection, and certification giants — Swiss-based SGS, French-based Bureau Veritas, or British-based Intertek. An AI can optimise a global supply chain flawlessly, but it cannot legally certify that a shipment of medical supplies meets EU safety standards. The liability, and therefore the economic moat, remains human.

Underweight the Coordination Layer (The Expropriation Target): This refers to the digital middlemen. These are the platforms that don’t actually produce the goods or provide the service, but extract rent by controlling the matchmaking — think Amazon’s marketplace, Uber, App Stores, and the digital advertising duopolies. They are massive, highly visible, centralised, and deeply unpopular. When an angry political system needs a scapegoat to appease a fracturing society, Big Tech has a giant bullseye painted on its back. Margin-crushing regulation or antitrust dismantling of these platforms is a populist dream.

Hedge with Store-of-Value (With Cyclical Caution): When the political resolution inevitably demands wealth redistribution, the fiat currency bears the cost. Gold and structural currency diversification compound significantly when governments inflate their way out of a social crisis. However, this is not a one-way street; precious metals typically suffer brutal liquidity drawdowns during initial market shocks before ripping higher in the policy response.

What This Is Not

To ensure we are trading on market realities and not political emotion, we must define what this framework does not claim:

It is not a prediction of exact timing. These are secular trends. In terms of sequencing, there are actually growing arguments — which I will cover in a coming issue — that we will likely see a cyclical, deflationary recession first. That recession will act as the catalyst, pushing the political system to panic and finally triggering the inflationary policy bust.

It is not a partisan political warning. State intervention historically comes from both sides of the aisle. Nixon (a Republican) imposed wage-price controls; FDR (a Democrat) built the New Deal. The math forces the state’s hand regardless of who occupies the office.

It is not a doomsday argument. The historical pattern is resolution, not total collapse. If you are familiar with Neil Howe and William Strauss’s The Fourth Turning [10], you recognise this rhythm. Late-cycle secular bear markets force an institutional reset, producing new social contracts and redirecting capital flows. Properly positioned capital does not just survive these transitions — historically, it multiplies.

The Bottom Line

We are living in a late-cycle society where the marginal worker’s economic leverage is falling vastly faster than the political system can comfortably absorb. Bimodal compression and Elite Overproduction are the disease; populist redistribution is the historical cure.

The most dangerous assumption an investor can make today is that the benign regulatory environment of the 2010s will survive the brutal economics of the late 2020s. Asset prices reprice the exact moment a political mechanism becomes visible — not when the bill is signed into law.

The people who get this right will hold the assets the resolution rewards: the diffuse, inflation-resistant owners of the human element, physical limits, and verification moats. The people who get it wrong will hold the massive, highly visible coordination-layer platforms, watching their margins compress against regulatory caps while the wealth they thought they had concentrated quietly migrates away.

References

[1] Chief Justice of India Surya Kant’s remarks in open court, 15 May 2026, and the rise of the satirical Cockroach Janta Party (founded 16 May 2026 by Abhijeet Dipke; roughly 19–22 million Instagram followers within a week, surpassing the ruling BJP’s official account): BBC News, CNN, The Guardian and Al Jazeera, 19 May – 8 June 2026. Graduate unemployment: nearly 40% of Indian graduates under 25 are jobless, per Azim Premji University research cited by CNN, 22 May 2026.

[2] Robertson Morrow, “The Bull Market in Politics” (Clarium Capital, circulated mid-to-late 2000s). Morrow was CIO of Clarium Capital. Primary attestation in George Packer, “No Death, No Taxes: The Libertarian Futurism of a Silicon Valley Billionaire,” The New Yorker, 28 November 2011, which discusses the paper and the thesis within a profile of Peter Thiel. Morrow’s later by-line at The American Conservative (2002–2005) provides corroborating biographical detail.

[3] Stray Narratives, Issue 12: “Who Gets Paid After AI,” May 2026. The four-mechanism framework and the bimodal compression that runs through each.

[4] Stray Narratives, Issue 06: “The Noise Economy,” April 2026. The 13% / 77% workforce split.

[5] Peter Turchin, End Times: Elites, Counter-Elites, and the Path of Political Disintegration, Penguin Press, 2023. The elite-overproduction framework is developed across the book; earlier statements appear in Ages of Discord (2016).

[6] American lawyer counts ~400,000 (mid-1970s) to 1.2 million (2011), per the American Bar Association, cited in Peter Turchin, Ages of Discord: A Structural-Demographic Analysis of American History (Beresta Books, 2016) and End Times (Penguin Press, 2023). MBA six-fold expansion over the same window per the same Turchin sources. Secondary summary in Noah Smith, “Blame Rich, Overeducated Elites as Our Society Frays,” Bloomberg Opinion, 20 November 2013.

[7] Viktor Shvets, The Twilight Before the Storm: From the Fractured 1930s to Today’s Crisis Culture (Boyle & Dalton, August 2024). Shvets is a global strategist at Macquarie Capital; the book is cited here as a public work. The Fujiwhara Effect itself is a 1921 meteorological term (named after Sakuhei Fujiwhara) describing the interaction of two or more cyclones; Shvets adopted it as the organising metaphor of his macro thesis, deployed across both The Twilight Before the Storm and his earlier The Great Rupture (2020). His three-cyclone reading (neoliberalism + financialisation + Information Age) is laid out at viktorshvets.com/the-fujiwara-effect and discussed with Alan Kohler in The New Daily, “The Fujiwara Effect — three cyclones of modern world,” 26 August 2024.

[8] Silicon Valley figures advocating Universal Basic Income, including Sam Altman’s Y Combinator Research UBI experiment and public commentary, 2016 onward.

[9] Alap Shah, “The Global Intelligence Crisis, Part Three: The Path Forward” (alapshah1.substack.com, March 2026) — the “American Prosperity Compact”: a corporate displacement tax funding income security and an American AI Dividend Fund modelled on the Alaska Permanent Fund.

[10] Paul Volcker’s Federal Reserve tightening cycle, 1979–1982, taming inflation following the failure of Nixon’s 1971 wage-price controls. Federal Reserve archive and historical record.

[11] Federal Reserve Quantitative Easing programmes commencing November 2008; the ensuing decade of financial repression as the macro-policy response to the Global Financial Crisis. Federal Reserve communications and successor literature.

[12] William Strauss and Neil Howe, The Fourth Turning: An American Prophecy, Broadway Books, 1997. The generational-cycle framework.